HSBC 2012 Annual Report Download - page 262

Download and view the complete annual report

Please find page 262 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Risk > Appendix – Risk policies and practices > Credit risk / Liquidity and funding

260

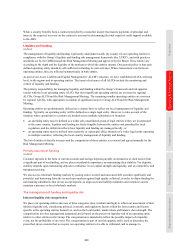

Our exposure to non-residential mortgage-related ABSs and direct lending includes securities with collateral relating

to:

• commercial property mortgages;

• leveraged finance loans;

• student loans; and

• other assets, such as securities with other receivable-related collateral.

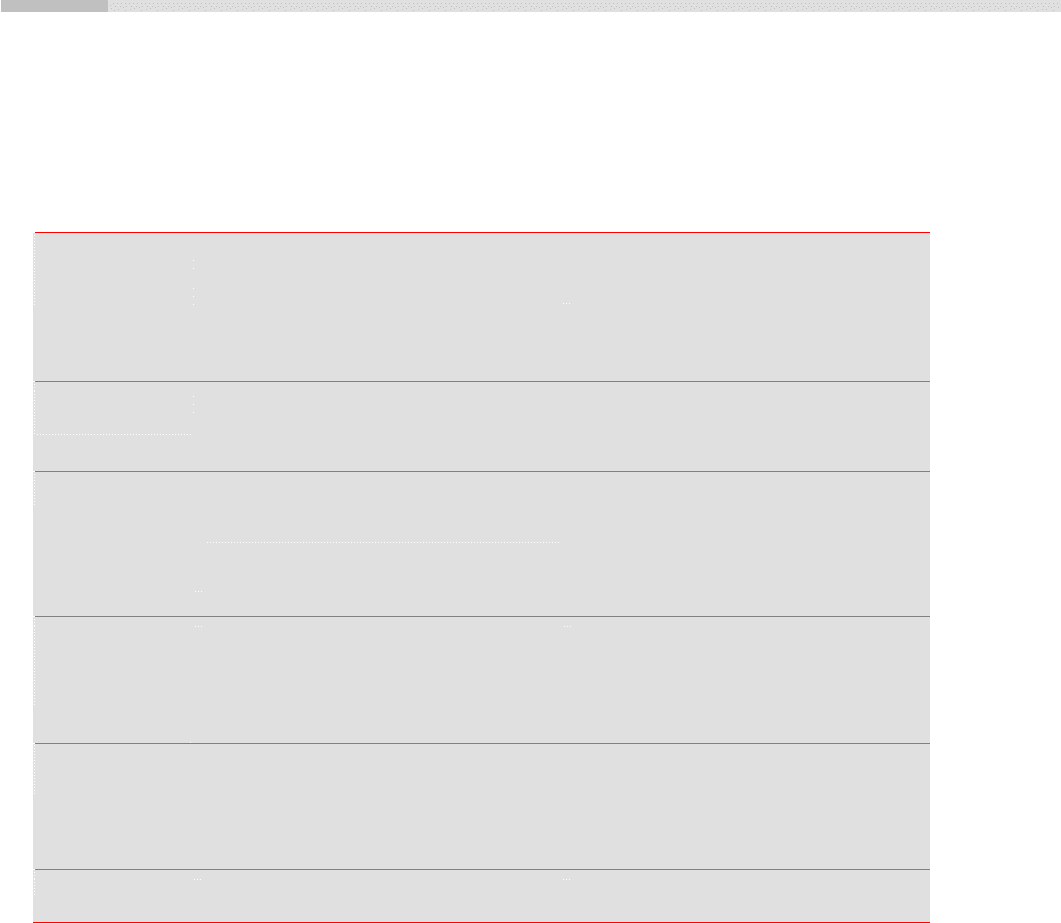

Categories of

ABSs and CDOs Definition Classification

Sub-prime Loans to customers who have limited credit histories,

modest incomes or high debt-to-income ratios or have

experienced credit problems caused by occasional

delinquencies, prior charge-offs, bankruptcy or other

credit-related actions.

For US mortgages, a FICO score of 620 or less has

primarily been used to determine whether a loan is sub-

prime. For non-US mortgages, management judgement

is used.

US Home Equity Lines

of Credit (‘HELoC’s)

A form of revolving credit facility provided to

customers, which is supported in the majority of

circumstances by a second lien or lower ranking charge

over residential property.

Holdings of HELoCs are classified as sub-prime.

US Alt-A Lower risk loans than sub-prime, but they share higher

risk characteristics than lending under fully conforming

standard criteria.

US credit scores and the completeness of

documentation held (such as proof of income), are

considered when determining whether an Alt-A

classification is appropriate. Non sub-prime mortgages

in the US are classified as Alt-A if they are not eligible

for sale to the major US Government mortgage

agencies or sponsored entities.

US Government agency

and sponsored

enterprises mortgage-

related assets

Securities that are guaranteed by US Government

agencies such as the Government National Mortgage

Association (‘Ginnie Mae’), or by US Government

sponsored entities including the Federal National

Mortgage Association (‘Fannie Mae’) and the Federal

Home Loan Mortgage Corporation (‘Freddie Mac’).

Holdings of US Government agency and US

Government sponsored enterprises’ mortgage-related

assets are classified as prime exposures.

UK non-conforming

mortgages

UK mortgages that do not meet normal lending criteria.

Examples include mortgages where the expected level

of documentation is not provided (such as income with

self-certification), or where poor credit history

increases risk and results in pricing at a higher than

normal lending rate.

UK non-conforming mortgages are treated as sub-

prime exposures.

Other mortgages Residential mortgages, including prime mortgages, that

do not meet any of the classifications described above.

Prime residential mortgage-related assets are included

in this category.

Impairment methodologies

(Audited)

To identify objective evidence of impairment for available-for-sale ABSs, an industry standard valuation model is

normally applied which uses data with reference to the underlying asset pools and models their projected future cash

flows. The estimated future cash flows of the securities are assessed at the specific financial asset level to determine

whether any of them are unlikely to be recovered as a result of loss events occurring on or before the reporting date.

The principal assumptions and inputs to the models are typically the delinquency status of the underlying loans, the

probability of delinquent loans progressing to default, the prepayment profiles of the underlying assets and the loss

severity in the event of default. However, the models utilise other variables relevant to specific classes of collateral to

forecast future defaults and recovery rates. Management uses externally available data and applies judgement when

determining the appropriate assumptions in respect of these factors. We use a modelling approach which incorporates

historically observed progression rates to default to determine if the decline in aggregate projected cash flows from

the underlying collateral will lead to a shortfall in contractual cash flows. In such cases, the security is considered to

be impaired.

In respect of CDOs, expected future cash flows for the underlying collateral are assessed to determine whether there

is likely to be a shortfall in the contractual cash flows of the CDO.