HSBC 2012 Annual Report Download - page 169

Download and view the complete annual report

Please find page 169 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

167

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

generally determined through a combination of

professional and internal valuations and physical

inspection. The frequency of revaluation is

undertaken on a similar basis to commercial real

estate loans and advances; however, for financing

activities in corporate and commercial lending that

are not predominantly commercial real estate-

oriented, collateral value is not as strongly correlated

to principal repayment performance. Collateral

values will generally be refreshed when an obligor’s

general credit performance deteriorates and it is

necessary to assess the likely performance of

secondary sources of repayment should reliance

upon them prove necessary. For this reason, the table

above reports values only for customers with CRR 8

to 10, recognising that these loans and advances

generally have valuations which are comparatively

recent. For the table above, cash is valued at its

nominal value and marketable securities at their

fair value.

The difference between the collateral value and

the value of partially collateralised lending disclosed

in the tables above cannot be directly compared with

any impairment allowances recognised in respect of

impaired loans, as the loans may be performing in

accordance with their contractual terms. When

loans are not performing in accordance with their

contractual terms, the recovery of cash flows may be

affected by other cash resources of the customer, or

other credit risk enhancements not quantified for the

tables above. The Group’s policy for determining

impairment allowances, including the effect of

collateral on these impairment allowances, is

described on page 258.

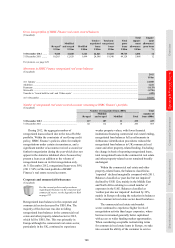

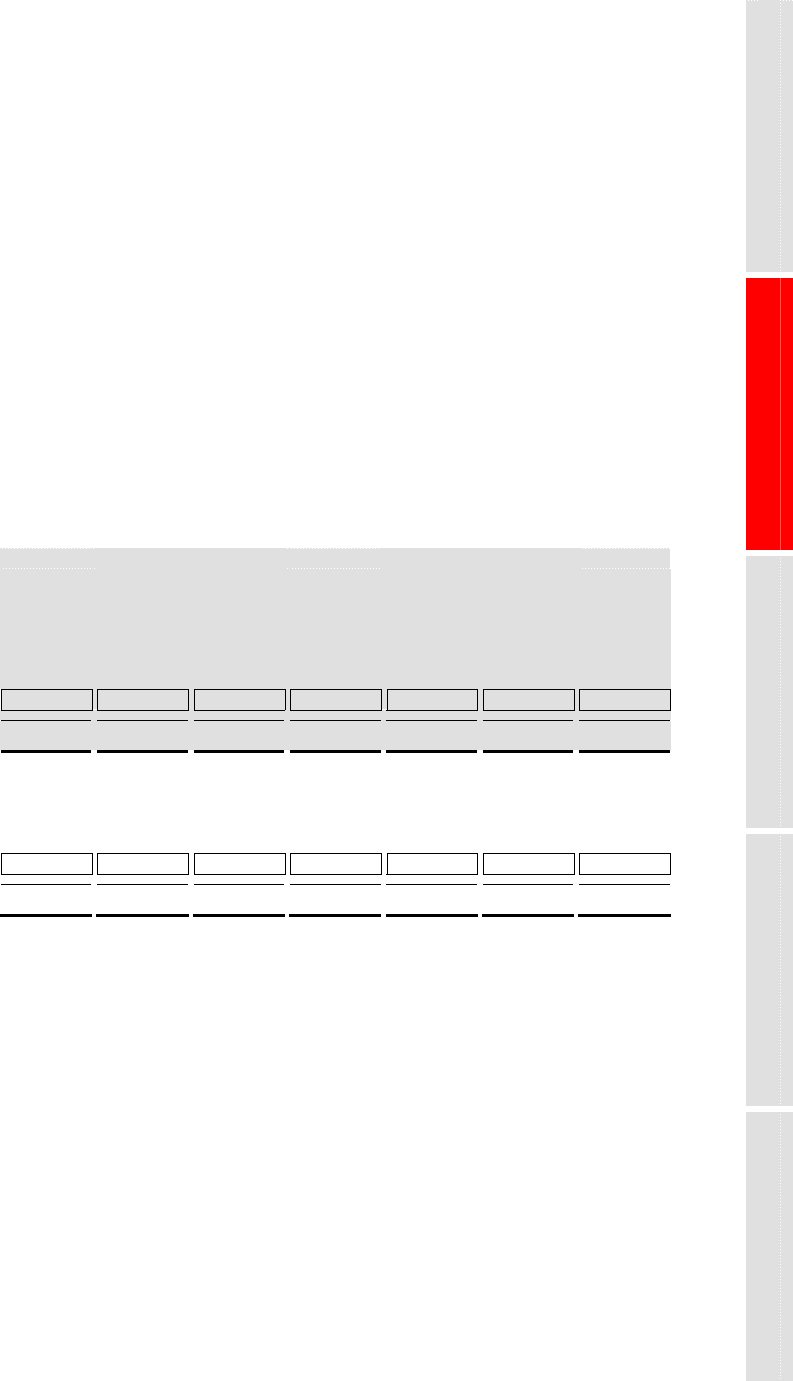

Loans and advances to banks

The following table shows loans and advances to

banks, including off-balance sheet loan

commitments by level of collateral.

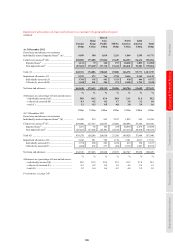

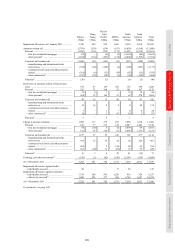

Loans and advances to banks including loan commitments by level of collateral

(Audited)

Europe

Hong

Kong

Rest of

Asia-Pacific MENA

North

America

Latin

America

Total

US$m US$m US$m US$m US$m US$m US$m

At 31 December 2012

Not collateralised ........................ 36,043 24,622 40,694 7,290 9,050 12,838 130,537

Fully collateralised ..................... 25,496 2,294 5,667 – 811 3,691 37,959

Partially collateralised (A)........... 62 1,459 1,207 – – – 2,728

– collateral value on A ............ 61 1,452 1,135 – – – 2,648

61,601 28,375 47,568 7,290 9,861 16,529 171,224

At 31 December 2011

Not collateralised ........................ 25,896 34,892 42,586 9,337 14,132 19,516 146,359

Fully collateralised ..................... 31,515 1,365 6,927 32 978 1,238 42,055

Partially collateralised (B)........... 146 50 445 – 784 114 1,539

– collateral value on B ............ 104 50 207 – 702 88 1,151

57,557 36,307 49,958 9,369 15,894 20,868 189,953

The collateral used in the assessment of the

above lending relates primarily to cash and

marketable securities. Loans and advances to banks

are typically unsecured. Certain products such as

reverse repos and stock borrowing are effectively

collateralised and have been included in the

above as fully or partly collateralised. The fully

collateralised loans and advances to banks for

Europe in the table above consist primarily of

reverse repo agreements and stock borrowing.

Derivatives

The International Swaps and Derivatives Association

(‘ISDA’) Master Agreement is our preferred

agreement for documenting derivatives activity. It

provides the contractual framework within which

dealing activity across a full range of over-the-

counter (‘OTC’) products is conducted, and

contractually binds both parties to apply close-out

netting across all outstanding transactions covered

by an agreement if either party defaults or another

pre-agreed termination event occurs. It is common,

and our preferred practice, for the parties to execute

a Credit Support Annex (‘CSA’) in conjunction

with the ISDA Master Agreement. Under a CSA,

collateral is passed between the parties to mitigate

the counterparty risk inherent in outstanding

positions. The majority of our CSAs are with

financial institutional clients.

We manage our counterparty exposure arising

due to market risk on OTC derivative contracts

through the use of collateral agreements with

counterparties and netting agreements. We do not

currently undertake active management of our