HSBC 2012 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

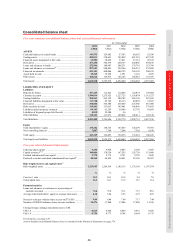

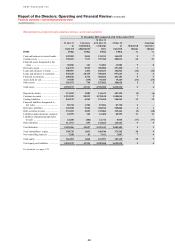

Financial summary > Consolidated balance sheet

46

Movement in 2012

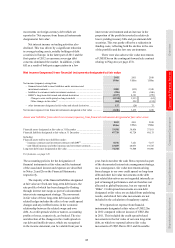

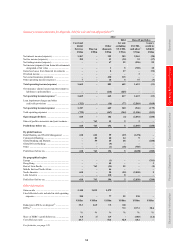

Total reported assets were US$2.7 trillion, 5%

higher than at 31 December 2011. Excluding the

effect of currency movements, total assets increased

by 4%, as shown on page 48.

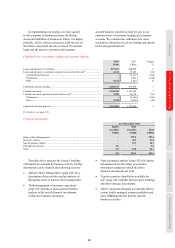

Our business model (see page 14) and our

approach to managing the Group balance sheet

contributed to our strong liquidity position.

Customer deposits increased by over US$65bn in

2012, which enabled us to continue to support our

customers’ borrowing requirements. Loans and

advances to customers grew by more than US$39bn

during the year, notably in residential mortgages and

term and trade-related lending to corporate and

commercial customers. Higher customer activity

also led to a rise in trading assets.

We have made significant progress in

simplifying and re-shaping our balance sheet to

improve our capital deployment. We completed a

significant number of business disposals during the

year, most notably the Card and Retail Services

business and non-strategic branches in the US. This

led to a significant reduction in ‘Assets held for sale’

with further transactions due to complete in 2013.

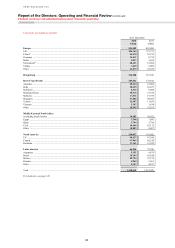

Assets

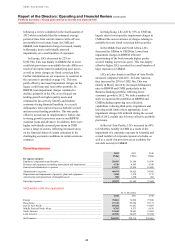

Cash and balances at central banks rose by 7% as

we placed a greater portion of our surplus liquidity

in Hong Kong, Europe and Rest of Asia-Pacific with

central banks, reflecting both our risk profile and

growth in customer deposits. This was partly offset

by a reduction in North America as liquidity was

redeployed into highly-rated financial investments.

Trading assets increased by 21%. At the end of

2011, client activity fell as eurozone debt concerns

dominated the global economy and, as a result, we

reduced our holdings of debt and equity securities

and did not replace maturities in our reverse repo

book. In 2012, client activity increased from these

subdued levels which resulted in a rise in reverse

repo and securities borrowing balances, together

with higher holdings of equity securities.

Notwithstanding the rise in year-end balances, we

actively managed the trading inventory in GB&M

and the average balance for the year declined by 9%.

Financial assets designated at fair value rose by

8%. Holdings of equity securities in our insurance

businesses in Hong Kong and Europe increased,

reflecting favourable market movements. Portfolio

growth was also partly attributable to net premiums

received in the year.

Derivative assets remained broadly in line with

December 2011 levels. Downward movements in

yield curves in major currencies led to a rise in the

fair value of interest rate contracts, largely in Europe

and, to a lesser extent, the US. This was partly offset

by a decline in the fair value of credit derivative

contracts in Europe and the US, as spreads tightened,

and foreign exchange contracts in Europe reflecting

lower volumes of open trades. In addition, netting

increased from an increase in trading through

clearing houses and a rise in the fair value of interest

rate contracts.

Loans and advances to banks declined by 16%,

driven by a reduction in reverse repo balances in

Europe, in part reflecting the redeployment of

liquidity to central banks, together with maturities

and repayments in Hong Kong and Rest of Asia-

Pacific.

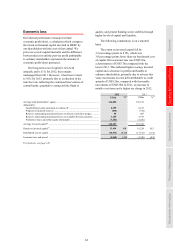

Loans and advances to customers increased by

4%. Residential mortgage balances continued to

grow strongly, following the success of marketing

campaigns and competitive pricing in the UK, the

continued strength in the property market in Hong

Kong and expansion of the distribution network

in Rest of Asia-Pacific. Our focus on corporate and

commercial customers that trade internationally led

to a rise in term and trade-related lending in Hong

Kong and Rest of Asia-Pacific. Lending to CMB

customers also increased in Europe, notably in the

UK despite muted demand for credit, and in North

America, reflecting our focus on target segments in

the US. In the Middle East and North Africa, the rise

in term lending balances followed the completion of

the merger of our operations in Oman with OIB and

the acquisition of the onshore retail and commercial

banking business of Lloyds Banking Group in the

UAE. Corporate overdraft balances which did not

meet netting criteria also increased in the UK, with a

corresponding rise in related customer accounts. The

above movements were partly offset by a reduction

in residential mortgage balances in North America as

a result of repayments and write-offs on the run-off

portfolio. Lending to GB&M customers in Europe

also declined as we reduced our exposure to certain

sectors and disposed of selected positions, and

clients chose to re-finance through the capital

markets. Reverse repo balances also declined,

mainly in Europe.

During 2012 we reclassified to ‘Assets held for

sale’ loans and advances to customers relating to the

planned disposals of non-strategic RBWM banking

operations in Rest of Asia-Pacific and businesses in

Latin America and Middle East and North Africa. In

addition, loans and advances to customers, net of

customer allowances, relating to the planned

disposal of non-real estate personal loan balances