HSBC 2012 Annual Report Download - page 387

Download and view the complete annual report

Please find page 387 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

377 -

378

378 -

379

379 -

380

380 -

381

381 -

382

382 -

383

383 -

384

384 -

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

390 -

391

391 -

392

392 -

393

393 -

394

394 -

395

395 -

396

396 -

397

397 -

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

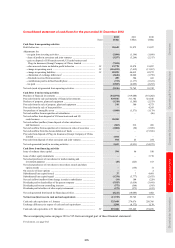

385

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

immediately in the income statement.

Changes in a parent’s ownership interest in a subsidiary that do not result in a loss of control are treated as

transactions between equity holders and are reported in equity.

Entities that are controlled by HSBC are consolidated until the date that control ceases.

In the context of Special Purpose Entities (‘SPE’s), the following circumstances may indicate a relationship in

which, in substance, HSBC controls and consequently consolidates an SPE:

• the activities of the SPE are being conducted on behalf of HSBC according to its specific business needs so

that HSBC obtains benefits from the SPE’s operation;

• HSBC has the decision-making powers to obtain the majority of the benefits of the activities of the SPE or,

by setting up an ‘autopilot’ mechanism, HSBC has delegated these decision-making powers;

• HSBC has rights to obtain the majority of the benefits of the SPE and therefore may be exposed to risks

incidental to the activities of the SPE; or

• HSBC retains the majority of the residual or ownership risks related to the SPE or its assets in order to

obtain benefits from its activities.

HSBC performs a re-assessment of consolidation whenever there is a change in the substance of the relationship

between HSBC and an SPE.

All intra-HSBC transactions are eliminated on consolidation.

The consolidated financial statements of HSBC also include the attributable share of the results and reserves

of joint ventures and associates. These are based on financial statements made up to 31 December, with the

exception of BoCom, Ping An and Industrial Bank which are included on the basis of financial statements

made up for the twelve months to 30 September. These are equity accounted three months in arrears in order

to meet the requirements of the Group’s reporting timetable. HSBC takes into account the effect of significant

transactions or events that occur between the period from 1 October to 31 December that would have a material

effect on its results. As discussed further in Note 26, HSBC announced disposal of its entire shareholding in Ping

An. As a result of the disposal of the first tranche of shares on 7 December 2012, HSBC no longer had

significant influence over Ping An at 31 December 2012 and ceased to account for it as an associate.

(f) Future accounting developments

At 31 December 2012, a number of standards and amendments to standards had been issued by the IASB which

are not effective for these consolidated financial statements. In addition to the projects to complete financial

instrument accounting, the IASB is continuing to work on projects on insurance, revenue recognition and lease

accounting which, together with the standards described below, could represent significant changes to

accounting requirements in the future.

Amendments issued by the IASB

Standards applicable in 2013

In May 2011, the IASB issued IFRS 10 ‘Consolidated Financial Statements,’ IFRS 11 ‘Joint Arrangements’ and

IFRS 12 ‘Disclosure of Interests in Other Entities.’ In June 2012, the IASB issued amendments to IFRS 10, IFRS

11 and IFRS 12 ‘Transition Guidance’. The standards and amendments are effective for annual periods

beginning on or after 1 January 2013 with early adoption permitted. IFRSs 10 and 11 are required to be applied

retrospectively.

Under IFRS 10, there is one approach for determining consolidation for all entities, based on the concept

of power, variability of returns and their linkage. This replaced the approach which applies to these financial

statements which emphasises legal control or exposure to risks and rewards, depending on the nature of the

entity. IFRS 11 places more focus on the investors’ rights and obligations than on the structure of the

arrangement, and introduces the concept of a joint operation. IFRS 12 is a comprehensive standard on disclosure

requirements for all forms of interests in other entities, including for unconsolidated structured entities.

We do not expect the overall effect of IFRS 10 and IFRS 11 on the financial statements to be material.