HSBC 2012 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

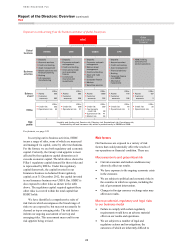

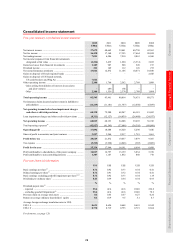

Financial summary > Consolidated income statement

30

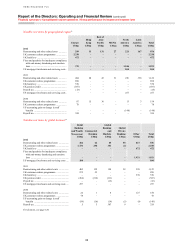

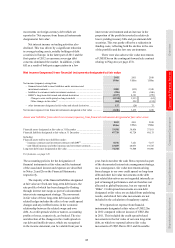

Reported profit before tax of US$20.6bn in 2012

was US$1.2bn, or 6%, lower than in 2011. This was

primarily due to adverse fair value movements on

own debt attributable to credit spreads of US$5.2bn,

compared with favourable movements of US$3.9bn

in 2011. The variance was partially offset by

US$7.5bn of gains (net of losses) on disposals,

in particular in respect of the US Card and Retail

Services business and our associate, Ping An. Our

remaining shareholding in Ping An has been

reclassified as a financial investment (see Note 26 on

the Financial Statements), the sale of which was

completed on 6 February 2013.

We expect disposal of the Card and Retail

Services business in North America and of our

associate shares in Ping An in Rest of Asia-Pacific to

have a significant impact on our profits in each of

these regions for the foreseeable future. In addition,

future profits in Rest of Asia-Pacific are expected to

be affected by the dilution of our shareholding in

Industrial Bank Co. Limited (‘Industrial Bank’),

following its issue of additional share capital to third

parties on 7 January 2013. Our shareholding in

Industrial Bank has now been classified as a financial

investment.

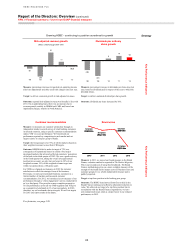

On an underlying basis, profit before tax rose by

18%, primarily due to higher net operating income

before loan impairment charges and other credit risk

provisions (‘revenue’) and lower loan impairment

charges and other credit risk provisions, which were

partially offset by an increase in operating expenses.

The latter was primarily driven by fines and penalties

paid as part of the settlement of investigations into

past inadequate compliance with anti-money

laundering and sanctions laws of US$1.9bn, and a

higher provision for UK customer redress

programmes of US$1.4bn.

The following commentary is on an underlying

basis, except where otherwise stated. The difference

between reported and underlying results is explained

and reconciled on page 26.

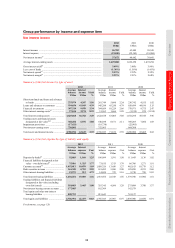

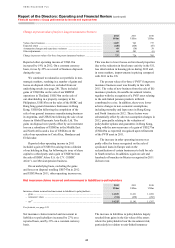

Revenue of US$63.5bn was US$4.2bn, or 7%,

higher than in 2011, primarily due to lower adverse

movements on non-qualifying hedges which

accounted for US$1.1bn of the increase, and

revenue growth in GB&M and CMB.

Revenue growth in GB&M mainly reflected

higher Rates and Credit income, notably in Europe,

as spreads tightened and investor sentiment improved

following stimuli by central banks globally.

In CMB, revenue growth primarily reflected

increased net interest income as a result of average

balance sheet growth. Customer loans and advances

grew in all regions, with over half this growth

coming from our faster-growing regions of Hong

Kong, Rest of Asia-Pacific and Latin America,

driven by trade-related lending. In Europe, lending

balances increased, notably in the UK, despite muted

demand for credit. Customer deposits also rose as we

continued to attract deposits through our Payments

and Cash Management products.

Revenue growth in RBWM reflected increased

insurance income, mainly in Hong Kong and Latin

America, which benefited from higher investment

returns and increased sales of life insurance products.

In addition, net interest income grew, mainly in

Hong Kong and Latin America, reflecting higher

average lending and deposit balances. These factors

were partially offset by the continued run-off of our

Consumer and Mortgage Lending (‘CML’) portfolio

in the US.

Loan impairment charges and other credit risk

provisions were US$2.3bn lower than in 2011.

This primarily reflected a decrease in North America,

mainly due to the continued decline in lending

balances and lower delinquency rates in the CML

portfolio. In addition, in Europe there were lower

credit risk provisions on available-for-sale asset-

backed securities (‘ABS’s) driven by an

improvement in underlying asset prices, and lower

loan impairment charges in RBWM, most notably in

the UK, as delinquency rates improved across both

unsecured and secured lending portfolios. These

factors were partially offset by increased loan

impairment charges and other credit risk provisions

in Latin America, particularly in Brazil, which were

primarily due to higher delinquency rates in RBWM

and in Business Banking in CMB. In Rest of Asia-

Pacific, there were also higher individually assessed

loan impairments on a small number of customers in

CMB.

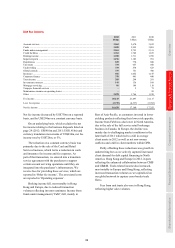

Operating expenses were higher than in 2011,

primarily from fines and penalties paid as part of

the settlement of investigations into past inadequate

compliance with anti-money laundering and

sanctions laws of US$1.9bn, as well as an increase

in provisions relating to UK customer redress

programmes of US$1.4bn. In addition, in 2011

operating expenses included a credit of US$570m

relating to defined benefit pension obligations in the

UK, which did not recur.

The charges for UK customer redress

programmes include estimates in respect of possible

mis-selling in previous years of payment protection

insurance (‘PPI’) policies of US$1.7bn and interest

rate protection products of US$598m. The additional

provision relating to PPI reflects our recent claims