HSBC 2012 Annual Report Download - page 165

Download and view the complete annual report

Please find page 165 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

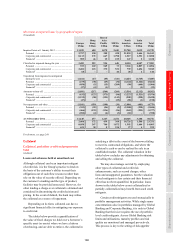

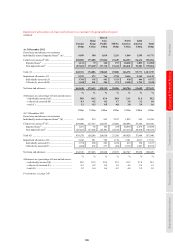

163

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

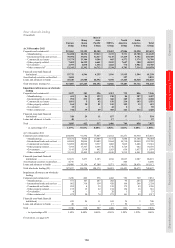

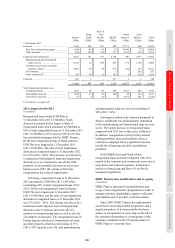

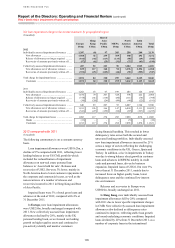

Movement in impaired loans by geographical region

(Unaudited)

Europe

Hong

Kong

Rest of

Asia-

Pacific MENA

North

America

Latin

America Total

US$m US$m US$m US$m US$m US$m US$m

Impaired loans at 1 January 2012 ............................. 11,819 608 1,070 2,445 22,758 3,039 41,739

Personal ................................................................ 2,797 190 388 428 21,094 1,646 26,543

Corporate and commercial ................................... 8,113 372 667 1,798 1,517 1,391 13,858

Financial2 .............................................................. 909 46 15 219 147 2 1,338

Classified as impaired during the year ..................... 3,482 292 924 648 8,130 4,507 17,983

Personal ................................................................ 933 169 549 73 7,363 2,807 11,894

Corporate and commercial ................................... 2,481 123 375 531 739 1,696 5,945

Financial2 .............................................................. 68 – – 44 28 4 144

Transferred from impaired to unimpaired

during the year ...................................................... (1,164) (47) (85) (321) (4,223) (1,765) (7,605)

Personal ................................................................ (279) (38) (69) (32) (4,124) (1,124) (5,666)

Corporate and commercial ................................... (858) (5) (15) (289) (99) (640) (1,906)

Financial2 .............................................................. (27) (4) (1) –– (1) (33)

Amounts written off ................................................. (1,891) (217) (564) (264) (3,514) (2,112) (8,562)

Personal ................................................................ (632) (127) (373) (96) (3,227) (1,521) (5,976)

Corporate and commercial ................................... (1,212) (90) (191) (143) (202) (590) (2,428)

Financial2 .............................................................. (47) – – (25) (85) (1) (158)

Net repayments and other.......................................... (1,101) (159) (198) (34) (2,806) (481) (4,779)

Personal ................................................................ (353) (22) (56) (5) (2,380) (228) (3,044)

Corporate and commercial ................................... (466) (133) (136) (26) (363) (253) (1,377)

Financial2 .............................................................. (282) (4) (6) (3) (63) – (358)

At 31 December 2012 .............................................. 11,145 477 1,147 2,474 20,345 3,188 38,776

Personal ................................................................ 2,466 172 439 368 18,726 1,580 23,751

Corporate and commercial ................................... 8,058 267 700 1,872 1,592 1,604 14,093

Financial2 .............................................................. 621 38 8 234 27 4 932

For footnote, see page 249.

Collateral

Collateral and other credit enhancements

held

(Audited)

Loans and advances held at amortised cost

Although collateral can be an important mitigant

of credit risk, it is the Group’s practice to lend on

the basis of the customer’s ability to meet their

obligations out of cash flow resources rather than

rely on the value of security offered. Depending on

the customer’s standing and the type of product,

facilities may be provided unsecured. However, for

other lending a charge over collateral is obtained and

considered in determining the credit decision and

pricing. In the event of default, the bank may utilise

the collateral as a source of repayment.

Depending on its form, collateral can have a

significant financial effect in mitigating our exposure

to credit risk.

The tables below provide a quantification of

the value of fixed charges we hold over a borrower’s

specific asset (or assets) where we have a history

of enforcing, and are able to enforce, the collateral in

satisfying a debt in the event of the borrower failing

to meet its contractual obligations, and where the

collateral is cash or can be realised by sale in an

established market. The collateral valuation in the

tables below excludes any adjustments for obtaining

and selling the collateral.

We may also manage our risk by employing

other types of collateral and credit risk

enhancements, such as second charges, other

liens and unsupported guarantees, but the valuation

of such mitigants is less certain and their financial

effect has not been quantified. In particular, loans

shown in the tables below as not collateralised or

partially collateralised may benefit from such credit

mitigants.

Certain credit mitigants are used strategically in

portfolio management activities. While single name

concentrations arise in portfolios managed by Global

Banking and Corporate Banking, it is only in Global

Banking that their size requires the use of portfolio

level credit mitigants. Across Global Banking risk

limits and utilisations, maturity profiles and risk

quality are monitored and managed pro-actively.

This process is key to the setting of risk appetite