HSBC 2012 Annual Report Download - page 281

Download and view the complete annual report

Please find page 281 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

279

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

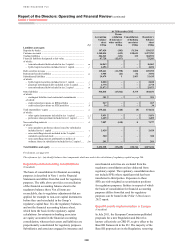

scheme’s trustees (where relevant). The defined benefit plans invest these contributions in a range of investments

designed to meet their long-term liabilities.

The level of these contributions has a direct impact on HSBC’s cash flow and would normally be set to ensure that

there are sufficient funds to meet the cost of the accruing benefits for the future service of active members. However,

higher contributions will be required when plan assets are considered insufficient to cover the existing pension

liabilities. Contribution rates are typically revised annually or triennially, depending on the plan. The agreed

contributions to the principal plan are revised triennially.

A deficit in a defined benefit plan may arise from a number of factors, including

• investments delivering a return below that required to provide the projected plan benefits. This could arise, for example, when there is a

fall in the market value of equities, or when increases in long-term interest rates cause a fall in the value of fixed income securities held;

• the prevailing economic environment leading to corporate failures, thus triggering write-downs in asset values (both equity and debt);

• a change in either interest rates or inflation which causes an increase in the value of the scheme liabilities; and

• scheme members living longer than expected (known as longevity risk).

A plan’s investment strategy is determined after taking into consideration the market risk inherent in the investments

and its consequential impact on potential future contributions. The long-term investment objectives of both HSBC

and, where relevant and appropriate, the trustees are:

• to limit the risk of the assets failing to meet the liabilities of the plans over the long-term; and

• to maximise returns consistent with an acceptable level of risk so as to control the long-term costs of the defined

benefit plans.

In pursuit of these long-term objectives, a benchmark is established for the allocation of the defined benefit plan

assets between asset classes. In addition, each permitted asset class has its own benchmarks, such as stock market or

property valuation indices and, where relevant, desired levels of out-performance. The benchmarks are reviewed

at least triennially within 18 months of the date at which an actuarial valuation is made, or more frequently if

required by local legislation or circumstances. The process generally involves an extensive asset and liability review.

Ultimate responsibility for investment strategy rests with either the trustees or, in certain circumstances, a

Management Committee. The degree of independence of the trustees from HSBC varies in different jurisdictions.

Pension plans in the UK

The largest plan globally exists in the UK, where the HSBC Bank (UK) Pension Scheme (‘the Scheme’) covers

employees of HSBC Bank plc and certain other employees of HSBC. This comprises a funded final salary defined

benefit plan (‘the principal plan’), which is closed to new entrants, and a defined contribution plan which was

established in July 1996 for new employees.

The principal plan, which accounts for approximately 70% of the obligations of our defined benefit pension plans,

is overseen by a corporate trustee who has a fiduciary responsibility for the operation of the pension scheme. The

Trustee is responsible for monitoring and managing the investment strategy and administration of scheme benefits.

The principal plan holds a diversified portfolio of investments to meet future cash flow liabilities arising from

accrued benefits as they fall due to be paid. The trustee of the principal plan is required to produce a written

Statement of Investment Principles which governs decision-making about how investments are made and the need

for adequate diversification is taken into account in the choice of asset allocation and manager structure in the

Defined Benefit Section.

Longevity risk in the principal plan is assessed as part of the measurement of the pension liability and managed

through the funding process of the scheme.

Pension plans in Hong Kong

In Hong Kong, the HSBC Group Hong Kong Local Staff Retirement Benefit Scheme covers employees of The

Hongkong and Shanghai Banking Corporation and certain other employees of HSBC. The scheme comprises a

funded defined benefit scheme and a defined contribution scheme. The defined benefit section of the scheme is a

final salary lump sum scheme and therefore its exposure to longevity risk is limited; it was closed to new members

from 1999.