HSBC 2012 Annual Report Download - page 154

Download and view the complete annual report

Please find page 154 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Risk > Credit risk > Personal lending / Wholesale lending

152

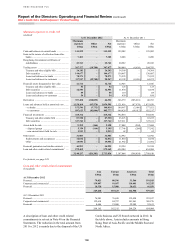

Valuation of foreclosed properties in the US

We obtain real estate by foreclosing on the collateral pledged

as security for residential mortgages. Prior to foreclosure,

carrying amounts of the loans in excess of fair value less costs

to sell are written down to the discounted cash flows expected

to be recovered, including from the sale of the property.

Broker price opinions are obtained and updated every 180 days

and real estate price trends are reviewed quarterly to reflect

any improvement or additional deterioration. Our methodology

is regularly validated by comparing the discounted cash flows

expected to be recovered based on current market conditions

(including estimated cash flows from the sale of the property)

to the updated broker price opinion, adjusted for the estimated

historical difference between interior and exterior appraisals.

The fair values of foreclosed properties are initially determined

based on broker price opinions. Within 90 days of foreclosure,

a more detailed property valuation is performed reflecting

information obtained from a physical interior inspection of

the property and additional allowances or write-downs are

recorded as appropriate. Updates to the valuation are

performed no less than once every 45 days until the property

is sold, with declines or increases recognised through changes

to allowances.

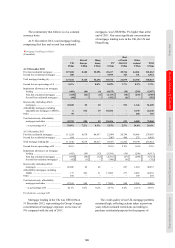

Credit cards

In the first half of 2012 we completed the sale

of our US Card and Retail Services business,

transferring general and private label credit card

lending balances to the purchaser. The residual

balances in the US at 31 December 2012 were

related to HSBC Bank USA’s credit card

programme.

Personal non-credit card lending

Personal non-credit card lending balances and two

months and over delinquent balances in the US fell,

largely due to the reclassification of non-real estate

personal loan balances to ‘Assets held for sale’ and

portfolio run-off, as this business is closed to new

advances.

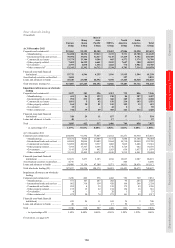

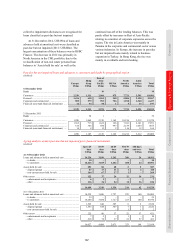

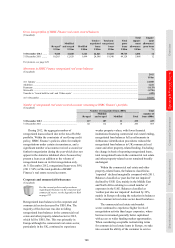

Trends in two months and over contractual delinquency in the US

(Unaudited)

At 31 December

2012 2011 2010

US$m US$m US$m

In personal lending in the US

First lien residential mortgages .................................................................................. 8,926 9,065 8,632

Consumer and Mortgage Lending .......................................................................... 7,629 7,922 7,618

Other mortgage lending .......................................................................................... 1,297 1,143 1,014

Second lien residential mortgages .............................................................................. 477 674 847

Consumer and Mortgage Lending .......................................................................... 350 501 668

Other mortgage lending .......................................................................................... 127 173 179

Credit card .................................................................................................................. 27 714 957

Private label ................................................................................................................ – 316 404

Personal non-credit card ............................................................................................. 335 513 811

Total ............................................................................................................................ 9,765 11,282 11,651

% % %

As a percentage of the relevant loans and receivables balances

First lien residential mortgages .................................................................................. 18.1 17.1 15.0

Second lien residential mortgages .............................................................................. 8.0 8.5 9.1

Credit card .................................................................................................................. 3.3 3.8 4.7

Private label ................................................................................................................ – 2.5 3.0

Personal non-credit card ............................................................................................. 7.4 8.3 9.5

Total ............................................................................................................................ 16.1 11.4 10.7

Wholesale lending

(Unaudited)

Wholesale lending covers the range of credit

facilities granted to sovereign borrowers, banks,

non-bank financial institutions, corporate entities

and commercial borrowers. Our wholesale portfolios

are well diversified across geographical and industry

sectors, with certain exposures subject to specific

portfolio controls.