HSBC 2012 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

17

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

Strategic direction

Our strategic objective is to become the

world’s leading international bank.

Our strategic direction is aligned to two long-term

trends:

• International trade and capital flows – the

world economy is becoming ever more

connected. Growth in world trade and cross-

border capital flows continues to outstrip growth

in average gross domestic product. Financial

flows between countries and regions are highly

concentrated, and over the next decade we

expect 35 markets to generate 90% of world

trade growth with a similar degree of

concentration in cross-border capital flows.

• Economic development and wealth creation –

we expect economies currently deemed

‘emerging’ to have increased five-fold in size by

2050, benefiting from demographics and

urbanisation, by which time they will be larger

than the developed world. By then, we expect

19 of the 30 largest economies will be markets

that are currently described as emerging.

HSBC is one of the few truly international

banks and our advantages lie in the extent to which

our network corresponds with markets relevant

to international financial flows, our access and

exposure to high growth markets and businesses,

and our strong balance sheet, which helps to

generate a resilient stream of earnings.

Based on these long-term trends and our

competitive position, our strategy has two parts:

• Network of businesses connecting the world –

HSBC is well positioned to capture the growing

international financial flows. Our global reach

and range of services put us in a strong position

to serve corporate clients as they grow from

small enterprises into large and international

corporates. Our access to local retail funding

and our suite of international products allows

us to offer distinctive solutions for these clients

profitably. We will focus on ‘South-South’ trade,

connecting faster-growing economies with each

other.

• Wealth management and retail with local scale –

social mobility and wealth creation in the faster-

growing markets in which we are positioned

will generate demand for financial services

which we will meet through our Wealth

Management and GPB businesses. We will

only invest in retail businesses in markets

where we can achieve critical mass.

To implement this strategy we have set priorities

across three areas to simplify, restructure and grow

the Group, as described below.

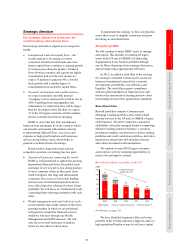

Simplifying HSBC

We will continue to make HSBC easier to manage

and control. This includes (i) running off legacy

assets in the US and in GB&M, (ii) addressing

fragmentation in our business portfolio through

our six filters disposing of non-strategic businesses,

and (iii) improving organisational efficiency.

In 2012, we added a sixth filter to the existing

five strategic evaluation criteria used to assess our

business (international connectivity, economic

development, profitability, cost efficiency and

liquidity). The sixth filter requires compliance

with our global standards on financial crime and

involves the assessment of existing and new client

relationships and activities against those standards.

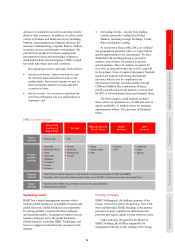

Run-off portfolios

Run-off portfolios comprise Consumer and

Mortgage Lending portfolios and certain related

treasury services in the US and, in GB&M, a legacy

credit business. The latter comprises a separately

identifiable, discretely managed business comprising

Solitaire Funding Limited (‘Solitaire’), securities

investment conduits, asset-backed securities, trading

portfolios and credit correlation portfolios, derivative

transactions entered into with monoline insurers

and certain structured credit transactions.

We continue to run off US legacy consumer

assets and are actively analysing opportunities to

reduce risk and improve returns.

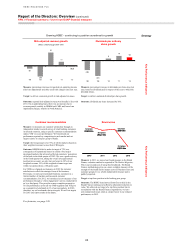

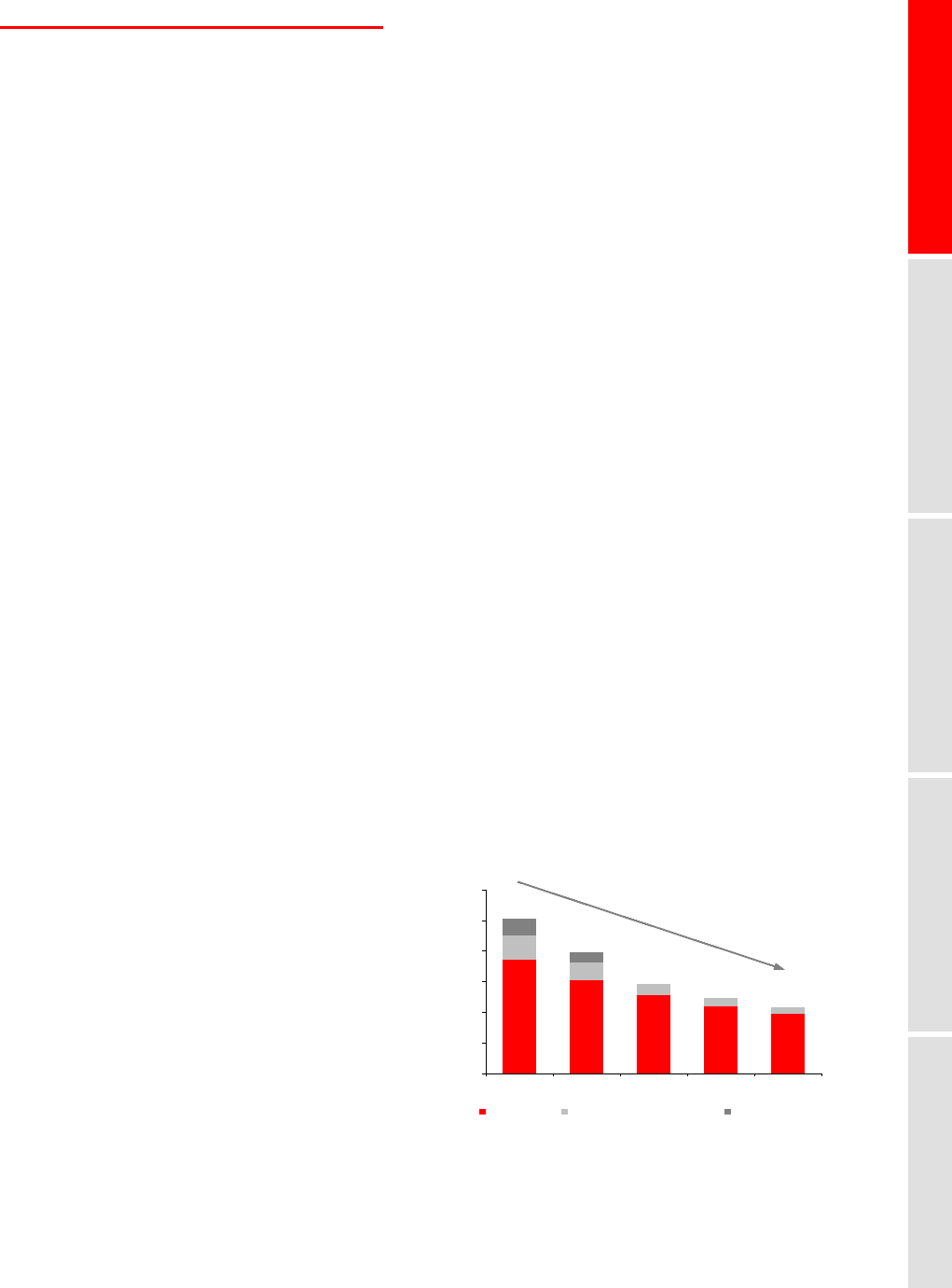

Run-off of portfolio receivables in the US

74 61 51 44 39

16

11

7

54

11

7

0

20

40

60

80

100

120

2008 2009 2010 2011 2012

Real estate Non-real estate (unsecured) Vehicle finance

101

79

58

49

Compound annual

growth rate 19%

43

US$bn

18

For footnote, see page 120.

We have identified segments of the real estate

portfolio in the US that represent a high risk and/or a

high operational burden or may be sold on a capital