HSBC 2012 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

127

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

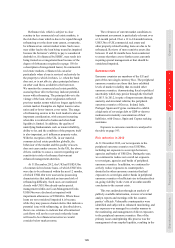

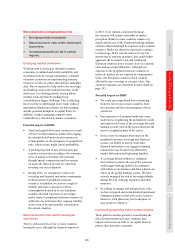

component of our risk management framework. It

is central to the annual planning process, in which

global businesses, geographical regions and

functions are required to articulate their risk

appetite statements. These are aligned with Group

strategy, and provide a risk profile of each global

business, region or function in the context of the

risk categories discussed above.

Quantitative and qualitative metrics are assigned

to nine key categories: earnings, capital, liquidity

and funding, securitisations, cost of risk, intra-group

lending, strategic investments, risk categories and

risk diversification and concentration. Measurement

against the metrics:

• guides underlying business activity, ensuring

it is aligned to risk appetite statements;

• informs risk-adjusted remuneration;

• enables the key underlying assumptions to be

monitored and, where necessary, adjusted

through subsequent business planning cycles;

and

• promptly identifies business decisions needed

to mitigate risk.

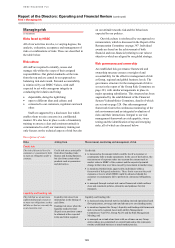

Some of the core metrics that are measured,

monitored and presented to the Board monthly are

tabulated below:

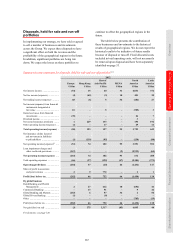

Risk appetite metrics

Target Actual

Core tier 1 ratio ........... 9.5% to 10.5% 12.3%

Return on equity ......... 12% to 15% 8.4%

Return on RWAs ........ 1.8% to 2.6% 1.8%

Dividend payout ratio . 40% to 60% 55.4%

Cost efficiency ratio ... 48% to 52% 62.8%

Advances to customer

accounts ratio........... Below 90%

74.4%

Cost of risk (LICs) ...... Below 20% of

operating income

9.9%

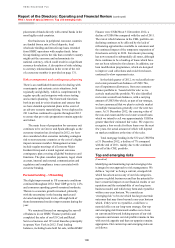

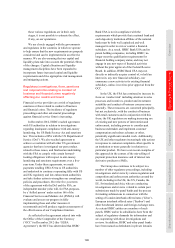

Stress testing

Our stress testing and scenario analysis programme

is central to the monitoring of top and emerging risks.

We conduct a range of Group stress-testing scenarios

including, but not limited to, severe global economic

downturn, country, sector and counterparty failures

and a variety of projected major operational risk

events. The outcomes of the stress testing are used

to assess the potential demand for regulatory capital

under the various scenarios. We also participate,

where appropriate, in scenario analyses requested by

regulatory bodies.

In the course of 2012, we examined several

scenarios reflecting potential developments in the

eurozone and more widely. Those reported to senior

management during 2012 included an assessment of

the annual operating plan 2012 under two

macroeconomic stress scenarios, as described below.

The results of the two scenarios demonstrated that

HSBC would remain satisfactorily capitalised under

the mild and severe scenarios after taking account of

assumed management actions.

In addition to the suite of risk scenarios

considered for the Group, each major HSBC

subsidiary conducts regular macroeconomic and

event-driven scenario analyses specific to their region.

Stress testing is used across risk categories such

as market risk, liquidity and funding risk and credit

risk to evaluate the potential impact of stress scenarios

on portfolio values, structural long-term funding

positions, income or capital.

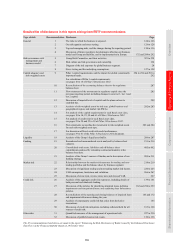

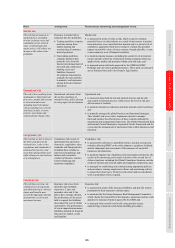

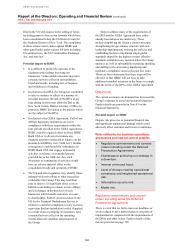

Stress scenario assumptions

Scenario Mild scenario assumptions Severe scenario assumptions

Assumptions

• the situation in Greece worsens and there is

an orderly default in Greece;

• Greek banks also default and, with support from the

EU and the International Monetary Fund, are bailed

out;

• increasing bond yields in Portugal, Ireland, Spain

and Italy trigger further fiscal austerity measures,

and governments strive to disassociate their

countries from Greece;

• through financial and trade linkages, an orderly

default in Greece results in the spread of contagion

to the rest of the world;

• the UK, US and emerging markets are adversely

affected, albeit to varying degrees; and

• slower global demand curbs growth and increases

the risk premium on interest rates as well as

commodity prices.

• a disorderly default in Greece, where the eurozone

governments are unable to ring-fence peripheral

countries and their banks;

• default of Portugal and Ireland with increases in

bond yields for high debt countries;

• the ensuing credit crunch together with declining

business and consumer confidence more than offset

any relief gained from the depreciation of the euro;

• investors become increasingly uncomfortable with

the US and the UK’s fiscal positions, with the severe

scenario resulting in a global slowdown; and

• emerging economies are less affected by the

financial shock.