HSBC 2012 Annual Report Download - page 249

Download and view the complete annual report

Please find page 249 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

247

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

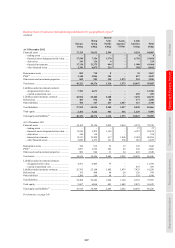

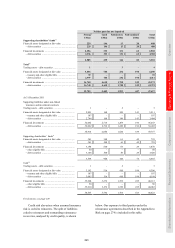

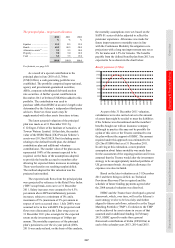

The principal plan – target asset allocation

2012 2011 2006

% % %

Equities ........................... 15.5 15.5 15.0

Bonds .............................. 60.5 60.5 50.0

Alternative assets75 ......... 9.5 9.5 10.0

Property ........................... 9.0 9.0 10.0

Cash ................................ 5.5 5.5 15.0

100.0 100.0 100.0

For footnote, see page 249.

As a result of a special contribution to the

principal plan in June 2010 of £1,760m

(US$2,638m), a cash generating portfolio was

established. The portfolio comprised supra-national,

agency and government-guaranteed securities,

ABSs, corporate subordinated debt and auction

rate securities. A further special contribution in

December 2011 of £184m (US$286m) added to this

portfolio. The contribution was used to

purchase ABSs from HSBC at an arm’s length value

determined by the Scheme’s independent third-party

advisers. However, these assets may be

supplemented with other assets from time to time.

The latest actuarial valuation of the principal

plan was made as at 31 December 2011 by

C G Singer, Fellow of the Institute of Actuaries, of

Towers Watson Limited. At that date, the market

value of the HSBC Bank (UK) Pension Scheme’s

assets was £18.3bn (US$28.3bn) (including assets

relating to the defined benefit plan, the defined

contribution plan and additional voluntary

contributions). The market value of the plan assets

represented 100% of the amount expected to be

required, on the basis of the assumptions adopted,

to provide the benefits accrued to members after

allowing for expected future increases in earnings.

There was therefore no resulting surplus/deficit.

The method adopted for this valuation was the

projected unit method.

The expected cash flows from the principal plan

were projected by reference to the Retail Price Index

(‘RPI’) swap break-even curve at 31 December

2011. Salary increases were assumed to be 0.5%

per annum above RPI and inflationary pension

increases, subject to a minimum of 0% and a

maximum of 5% (maximum of 3% per annum in

respect of service accrued since 1 July 2009), were

assumed to be in line with RPI. The projected cash

flows were discounted at the Libor swap curve at

31 December 2011 plus a margin for the expected

return on the investment strategy of 160bps per

annum. The mortality experience of the principal

plan’s pensioners over the six-year period (2006-

2011) was analysed and, on the basis of this analysis,

the mortality assumptions were set, based on the

SAPS S1 series of tables adjusted to reflect the

pensioner experience. Allowance was made for

future improvements to mortality rates in line

with the Continuous Mortality Investigation core

projections with a long run improvement rate set at

2% for males and 1.5% for females. The benefits

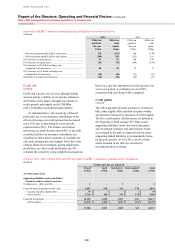

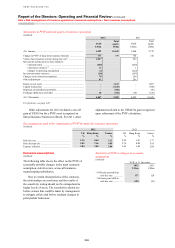

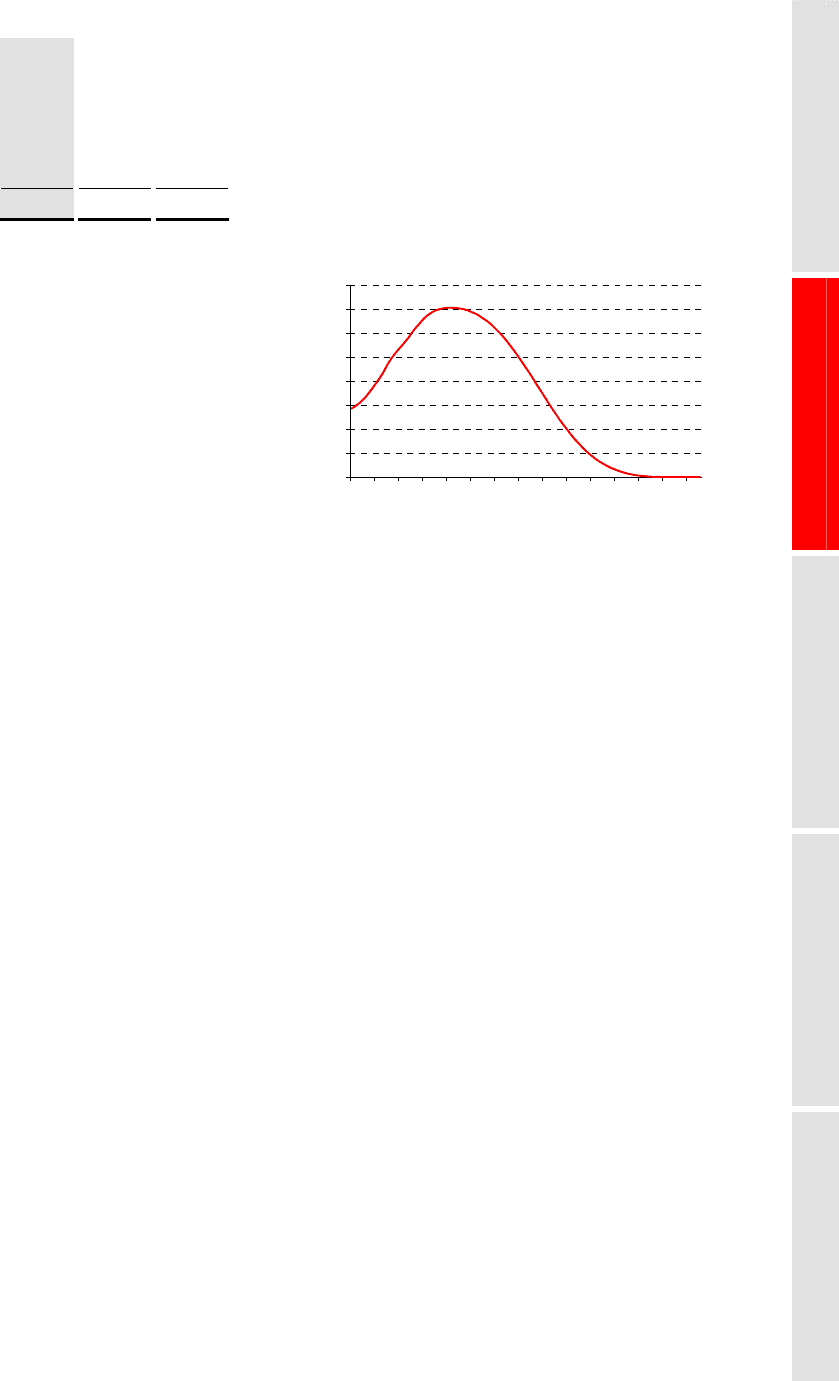

payable from the defined benefit plan from 2013 are

expected to be as shown in the chart below.

Benefit payments (US$m)

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2013

2019

2025

2031

2037

2043

2049

2055

2061

2067

2073

2079

2085

2091

2097

As part of the 31 December 2011 valuation,

calculations were also carried out as to the amount

of assets that might be needed to meet the liabilities

if the Scheme was discontinued and the members’

benefits bought out with an insurance company

(although in practice this may not be possible for

a plan of this size) or the Trustee continued to run

the plan without the support of HSBC. The amount

required under this approach was estimated to be

£26.2bn (US$40.6bn) as at 31 December 2011.

In arriving at this estimation, a more prudent

assumption about future mortality was made than

for the assessment of the ongoing position and it was

assumed that the Trustee would alter the investment

strategy to be an appropriately matched portfolio of

UK government bonds. An explicit allowance for

expenses was also included.

Based on the latest valuation as at 31 December

2011 and there being no deficit, no Technical

Provisions Recovery Plan is required and the

schedule of future funding payments agreed after

the 2008 actuarial valuation was dissolved.

HSBC and the Trustee have developed a general

framework, which, over time, will see the Scheme’s

asset strategy evolve to be less risky and further

aligned to future cash-flows, referred to as the Target

Matching Portfolio (‘TMP’). Evolution to the TMP

can be achieved by asset returns in excess of that

assumed and/or additional funding. In February

2013, HSBC agreed to make three general

framework contributions of £64m (US$103m) in

each of the calendar years 2013, 2014 and 2015.