HSBC 2012 Annual Report Download - page 241

Download and view the complete annual report

Please find page 241 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

239

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

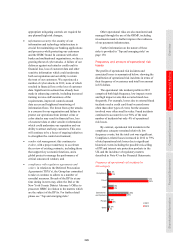

Approximately 65.6% of financial assets were

invested in debt securities at 31 December 2012

(2011: 65.2%) with 24.5% (2011: 22.9%) invested

in equity securities.

In life linked insurance, premium income less

charges levied is invested in a portfolio of assets. We

manage the financial risks of this product on behalf

of the policyholders by holding appropriate assets in

segregated funds or portfolios to which the liabilities

are linked. These assets represented 25.2% (2011:

23.2%) of the total financial assets of our insurance

manufacturing subsidiaries at the end of 2012.

The remaining financial risks are managed

either solely on behalf of the shareholder, or jointly

on behalf of the shareholder and policyholders where

DPF exist.

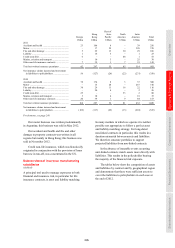

Market risk

(Audited)

Market risk arises when mismatches occur between

product liabilities and the investment assets which

back them. For example, mismatches between asset

and liability yields and maturities give rise to interest

rate risk.

Long-term insurance or investment products

may incorporate benefits that are guaranteed. Where

mismatches exist as a result of current yields falling

below guaranteed levels for a prolonged period, the

risk that shareholder capital is required to meet

liabilities to policyholders increases. The table below

shows, in respect of each category of guarantee, the

total liabilities to policyholders established for

guaranteed products manufactured by our insurance

subsidiaries. The table also shows the range of

investment returns on the assets supporting these

products and the implied investment returns that

would enable the business to meet the guarantees.

Immediate annuities, where current investment

returns are below guarantees, relate to a closed

portfolio in the US which is held for sale at

31 December 2012. Annual return guarantees

between 4.5-6%, where current investment returns

are below guarantees, is a closed portfolio in Hong

Kong. The only other portfolio of contracts

identified where current investment returns are

below guarantees relate to a closed portfolio in

France. This portfolio has reserves of US$495m for

which current portfolio yields are 3.25% but

investment returns implied by the guarantees are

4.5%.

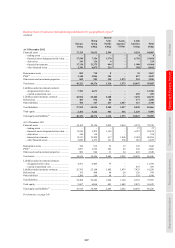

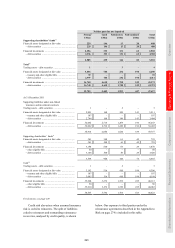

Liabilities to policyholders69

(Audited)

2012 2011

Amount of

reserve

Investment

returns

implied by

guarantee64

Current

yields

Amount of

reserve

Investment

returns

implied by

guarantee64

Current

yields

US$m % % US$m % %

Annuities in payment .......................................... 1,379 0.0 – 11.7 4.6 – 20.8 1,414 0.0 – 9.6 4.2 – 25.2

Deferred annuities .............................................. 179 0.0 – 6.0 3.3 – 20.4 175 0.0 – 6.0 3.2 – 22.7

Immediate annuities70 ......................................... 485 6.0 – 12.0 5.4 – 5.5 538 6.0 – 12.0 5.3 – 5.4

Annual return ...................................................... 23,878 0.0 – 2.5 1.4 – 4.7 20,465 0.0 – 2.5 0.0 – 6.9

Annual return ...................................................... 4,315 2.5 – 4.5 3.3 – 6.7 3,849 2.5 – 4.5 3.3 – 10.0

Annual return ...................................................... 155 4.5 – 6.0 4.1 – 4.2 163 4.5 – 6.0 6.4 – 6.5

Capital ................................................................. 18,779 – 0.0 – 7.2 17,400 – 2.3 – 7.8

For footnotes, see page 249.

The following table illustrates the effects of

selected interest rate, equity price, foreign exchange

rate and credit spread scenarios on our profit for the

year and total equity of our insurance manufacturing

subsidiaries.

Where appropriate, we include the impact of the

stress on the PVIF in the results of the sensitivity

tests. The relationship between the profit and total

equity and the risk factors is non-linear and,

therefore, the results disclosed should not be

extrapolated to measure sensitivities to different

levels of stress. The sensitivities are stated before

allowance for management actions which may

mitigate the effect of changes in market rates, and

for any factors such as policyholder behaviour that

may change in response to changes in market risk.