HSBC 2012 Annual Report Download - page 173

Download and view the complete annual report

Please find page 173 of the 2012 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

|

|

171

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

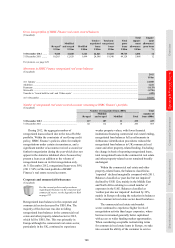

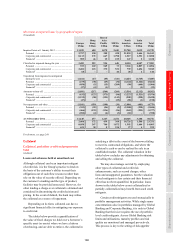

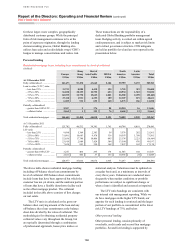

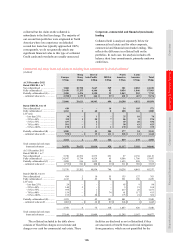

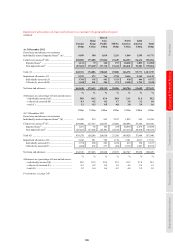

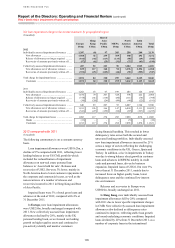

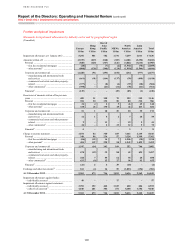

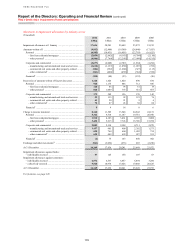

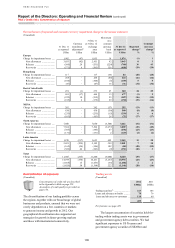

trade sector were written off or upgraded following

repayments, and delinquency rates reduced.

Releases and recoveries in Hong Kong were

US$65m, 27% lower than at the end of 2011 when

an allowance relating to a loan in GB&M that was

no longer considered impaired was released.

New loan impairment allowances in Rest of

Asia-Pacific increased by 8% to US$607m.

This reflected higher new collectively assessed

loan impairment allowances, mainly from the

growth in Singapore of RBWM’s credit card

portfolio. New individually assessed loan

impairment allowances also increased, as a result of

the impairment of a corporate exposure in Australia

and individual charges on a small number of

corporate exposures in India. Impaired loans in the

region increased by 4% to US$1.1bn in 2012 due to

the downgrade of a number of customers in Australia

and Taiwan, partly offset by the restructuring of a

significant loan in Singapore following the

renegotiation of terms, which is therefore regarded

as no longer impaired.

Releases and recoveries in the region decreased

by 7%, mainly in India as the cards portfolio

continued to run off, and in Thailand following

the sale of the RBWM business. These were

partly offset by an impairment allowance release

in Singapore compared with a charge in 2011.

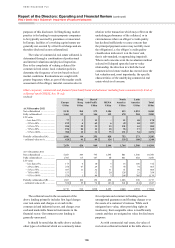

In the Middle East and North Africa, new

loan impairment allowances decreased by 2% to

US$463m in 2012. New collectively assessed loan

impairment allowances declined, primarily in the

UAE, due to the improvement in credit quality

reflecting the repositioning of the book towards

higher quality lending in previous years. New

individually assessed loan impairment allowances

rose due to significant loan impairment charges

recorded for a small number of large exposures

in GB&M. Impaired loans remained broadly

unchanged compared with 31 December 2011.

Releases and recoveries in the region increased

by 14% to US$208m in 2012, mainly relating to

a small number of exposures in UAE.

In North America, new loan impairment

allowances fell sharply, reducing by 50% to

US$3.7bn. New collectively assessed loan

impairment allowances declined, largely in the CML

portfolio due to the reclassification of impairment

allowances on non-real estate personal loan balances

to ‘Assets held for sale’ as well as the continued run-

off in the residential portfolios. This was partly

offset by a portfolio risk factor adjustment of

US$225m which was made to increase the collective

loan impairment allowances for our US mortgage

lending portfolios. The adjustment was made

following a review completed in the fourth quarter

of 2012 which concluded that the estimated average

period of time from current status to write-off was

ten months for real estate loans (previously a period

of seven months was used). During 2013, this

revised estimate will be incorporated into the

statistical impairment allowance models. It

was also partly offset by new loan impairment

allowances by HSBC Bank Bermuda on a small

number of exposures. Releases and recoveries in

North America declined by 11% to US$214m. This

reflected lower levels of impairments being booked

due to improving market conditions within the

corporate and commercial sector.

Impaired loans decreased by 11% in 2012 to

US$20.3bn, due to the continued run-off of the CML

portfolio which included the reclassification

of certain non-real estate personal loan balances to

held for sale.

In Latin America, new loan impairment

allowances increased by 23% to US$2.5bn.

The increase in new collectively assessed loan

impairment allowances was mainly in Brazil, driven

by higher delinquency rates in RBWM and CMB,

particularly in the Business Banking portfolio,

reflecting lower economic growth in 2012. Impaired

loans were 9% higher than at the end of 2011, driven

by past growth in the CMB portfolio in Brazil.

Releases and recoveries in Latin America

decreased by 2% from the end of 2011 to US$401m,

mainly in Brazil.

For an analysis of loan impairment charges and

other credit risk provisions by global business, see

page 76.