Entergy 2007 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2007 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

|

|

90

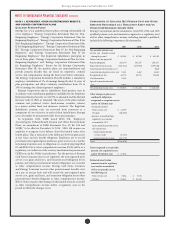

Entergy Corporation and Subsidiaries 2007

Notes to Consolidated Financial Statements continued

OT H E R PO S T R E T I R E M E N T BE N E F I T OB L I G AT I O N S , PL A N

AS S E T S , FU N D E D ST A T U S , A N D AM O U N T S RE C O G N I Z E D

IN T H E BA L A N C E SH E E T O F EN T E R G Y CO R P O R AT I O N A N D

I T S S U B S I D I A R I E S A S O F DE C E M B E R 31, 2007 A N D 2006

(IN T H O U S A N D S ):

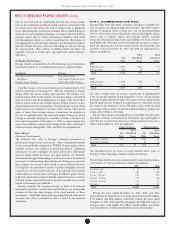

2007 2006

Change in APBO

Balance at beginning of year $1,074,559 $ 997,969

Service cost 44,137 41,480

Interest cost 63,231 57,263

Acquisition 11,336 –

Plan amendments (3,520) (10,708)

Special termination benets 603 –

Plan participant contributions 11,384 6,904

Actuarial gain (19,997) (17,838)

Benets paid (56,719) (62,314)

Medicare Part D subsidy received 4,617 1,610

Balance at end of year $1,129,631 $1,014,366

Change in Plan Assets

Fair value of assets at beginning of year $ 314,326 $ 234,516

Actual return on plan assets 20,314 27,912

Employer contributions 56,300 64,058

Plan participant contributions 11,384 6,904

Acquisition 5,114 –

Benets paid (56,719) (60,700)

Fair value of assets at end of year $ 350,719 $ 272,690

Funded status $ (778,912) $ (741,676)

Amounts recognized in the balance sheet (SFAS 158)

Current liabilities $ (28,859) $ (27,372)

Non-current liabilities (750,053) (714,304)

Total funded status $ (778,912) $ (741,676)

Amounts recognized as a regulatory asset

(before tax)

Transition obligation $ 12,435 $ 8,686

Prior service cost (30,833) (9,263)

Net loss 224,532 195,567

$ 206,134 $ 194,990

Amounts recognized as OCI (before tax)

Transition obligation $ 6,709 $ 4,321

Prior service cost (16,634) (52,799)

Net loss 112,692 158,166

$ 102,767 $ 109,688

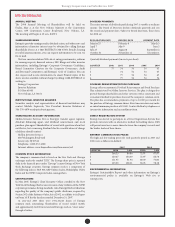

Qualified Pension and Other Postretirement

Plans’ Assets

Entergy’s qualied pension and postretirement plans’ weighted-

average asset allocations by asset category at December 31, 2007 and

2006 are as follows:

Qualied Pension Postretirement

2007 2006 2007 2006

Domestic Equity Securities 44% 43% 37% 37%

International Equity Securities 20% 21% 14% 14%

Fixed-Income Securities 34% 34% 49% 49%

Other 2% 2% –% –%

e Plan Administrator’s trust asset investment strategy is to invest

the assets in a manner whereby long-term earnings on the assets

(plus cash contributions) provide adequate funding for retiree benet

payments. e mix of assets is based on an optimization study that

identies asset allocation targets in order to achieve the maximum

return for an acceptable level of risk, while minimizing the expected

contributions and pension and postretirement expense.

In the optimization study, the Plan Administrator formulates

assumptions about characteristics, such as expected asset class

investment returns, volatility (risk), and correlation coecients among

the various asset classes. e future market assumptions used in the

optimization study are determined by examining historical market

characteristics of the various asset classes, and making adjustments to

reect future conditions expected to prevail over the study period.

e optimization analysis utilized in the Plan Administrator’s latest

study produced the following approved asset class target allocations.

Pension Postretirement

Domestic Equity Securities 45% 37%

International Equity Securities 20% 14%

Fixed-Income Securities 31% 49%

Other (Cash and Group Annuity Contracts) 4% –%

These allocation percentages combined with each asset class’

expected investment return produced an aggregate return expectation

for the ve years following the study of 7.6% for pension assets,

5.4% for taxable postretirement assets, and 7.2% for non-taxable

postretirement assets.

The expected long term rate of return of 8.50% for the qualied

Retirement Plans assets is based on the expected long-term return of

each asset class, weighted by the target allocation for each class as

dened in the table above. The source for each asset class’ expected

long-term rate of return is the geometric mean of the respective asset

class total return. The time period reected in the total returns is a long

dated period spanning several decades.

The expected long term rate of return of 8.50% for the non-taxable

VEBA trust assets is based on the expected long-term return of each

asset class, weighted by the target allocation for each class as dened

in the table above. The source for each asset class’ expected long-term

rate of return is the geometric mean of the respective asset class’ total

return. The time period reected in the total returns is a long dated

period spanning several decades.

For the taxable VEBA trust assets the allocation has a high

percentage of tax-exempt xed income securities. The tax-exempt

xed income long-term total return was estimated using total return

data from the 2007 Economic Report of the President. e time period

reected in the tax-exempt xed income total return is 1929 to 2006.

Aer reecting the tax-exempt xed income percentage and unrelated

business income tax, the long-term rate of return for taxable VEBA

trust assets is expected to be 6.0%.

Since precise allocation targets are inecient to manage security

investments, the following ranges were established to produce an

acceptable economically ecient plan to manage to targets:

Pension Postretirement

Domestic Equity Securities 45% to 55% 32% to 42%

International Equity Securities 15% to 25% 9% to 19%

Fixed-Income Securities 25% to 35% 44% to 54%

Other 0% to 10% 0% to 5%

AC C U M U L AT E D PE N S I O N BE N E F I T OB L I G AT I O N

e accumulated benet obligation for Entergy’s qualied pension

plans was $2.8 billion and $2.7 billion at December 31, 2007 and 2006,

respectively.