Entergy 2007 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2007 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

51

Entergy Corporation and Subsidiaries 2007

The Pension Protection Act also extended the provisions of the Pension

Funding Equity Act that would have expired in 2006 had the Pension

Protection Act not been enacted, which increased the allowed discount

rate used to calculate the pension funding liability.

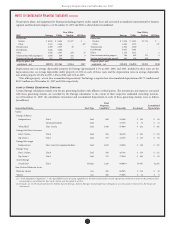

Total postretirement health care and life insurance benet costs for

Entergy in 2007 were $89.6 million, including $26 million in savings

due to the estimated eect of future Medicare Part D subsidies.

Entergy expects 2008 postretirement health care and life insurance

benet costs to be $93.4 million. is includes a projected

$24.7 million in savings due to the estimated eect of future Medicare

Part D subsidies. Entergy expects to contribute $69.6 million in 2008

to its other postretirement plans.

OT H E R CO N T I N G E N C I E S

As a company with multi-state domestic utility operations and a history

of international investments, Entergy is subject to a number of federal,

state, and international laws and regulations and other factors and

conditions in the areas in which it operates, which potentially subject

it to environmental, litigation, and other risks. Entergy periodically

evaluates its exposure for such risks and records a reserve for those

matters which are considered probable and estimable in accordance

with generally accepted accounting principles.

Environmental

Entergy must comply with environmental laws and regulations

applicable to the handling and disposal of hazardous waste. Under these

various laws and regulations, Entergy could incur substantial costs

to restore properties consistent with the various standards. Entergy

conducts studies to determine the extent of any required remediation

and has recorded reserves based upon its evaluation of the likelihood

of loss and expected dollar amount for each issue. Additional sites

could be identied which require environmental remediation for

which Entergy could be liable. e amounts of environmental reserves

recorded can be signicantly aected by the following external events

or conditions:

n Changes to existing state or federal regulation by governmental

authorities having jurisdiction over air quality, water quality,

control of toxic substances and hazardous and solid wastes, and

other environmental matters.

n e identication of additional sites or the ling of other

complaints in which Entergy may be asserted to be a potentially

responsible party.

n e resolution or progression of existing matters through the

court system or resolution by the United States Environmental

Protection Agency (EPA).

Litigation

Entergy has been named as defendant in a number of lawsuits involving

employment, ratepayer, and injuries and damages issues, among other

matters. Entergy periodically reviews the cases in which it has been

named as defendant and assesses the likelihood of loss in each case as

probable, reasonably estimable, or remote and records reserves for cases

which have a probable likelihood of loss and can be estimated. Notes

2 and 8 to the nancial statements include more detail on ratepayer

and other lawsuits and management’s assessment of the adequacy of

reserves recorded for these matters. Given the environment in which

Entergy operates, and the unpredictable nature of many of the cases

in which Entergy is named as a defendant, however, the ultimate

outcome of the litigation Entergy is exposed to has the potential to

materially aect the results of operations of Entergy, or its operating

company subsidiaries.

Sales Warranty and Tax Reserves

Entergy’s operations, including acquisitions and divestitures,

require Entergy to evaluate risks such as the potential tax eects of a

transaction, or warranties made in connection with such a transaction.

Entergy believes that it has adequately assessed and provided for these

types of risks, where applicable. Any reserves recorded for these types

of issues, however, could be signicantly aected by events such as

claims made by third parties under warranties, additional transactions

contemplated by Entergy, or completion of reviews of the tax treatment

of certain transactions or issues by taxing authorities. Entergy does not

expect a material adverse eect on earnings from these matters.

NE W AC C O U N T I N G PR O N O U N C E M E N T S

In September 2006 the FASB issued Statement of Financial Accounting

Standards No. 157, “Fair Value Measurements” (SFAS 157), which

denes fair value, establishes a framework for measuring fair value

in GAAP, and expands disclosures about fair value measurements.

SFAS 157 generally does not require any new fair value measurements.

However, in some cases, the application of SFAS 157 in the future may

change Entergy’s practice for measuring and disclosing fair values

under other accounting pronouncements that require or permit fair

value measurements. SFAS 157 is eective for Entergy in the rst

quarter 2008 and will be applied prospectively. Entergy does not expect

the application of SFAS 157 to materially aect its nancial position,

results of operations, or cash ows.

In February 2007 the FASB issued Statement of Financial Accounting

Standards No. 159, “e Fair Value Option for Financial Assets

and Financial Liabilities” (SFAS 159). SFAS 159 provides an option

for companies to select certain nancial assets and liabilities to be

accounted for at fair value with changes in the fair value of those assets

or liabilities being reported through earnings. e intent of the standard

is to mitigate volatility in reported earnings caused by the application

of the more complicated fair value hedging accounting rules. Under

SFAS 159, companies can select existing assets or liabilities for this fair

value option concurrent with the eective date of January 1, 2008 for

companies with scal years ending December 31 or can select future

assets or liabilities as they are acquired or entered into. Entergy does not

expect that the adoption of this standard will have a material eect on its

nancial position, results of operations, or cash ows.

e FASB issued Statement of Financial Accounting Standards No.

141(R), “Business Combinations” (SFAS 141(R)) during the fourth

quarter 2007. e signicant provisions of SFAS 141R are that: (i) assets,

liabilities and non-controlling (minority) interests will be measured

at fair market value; (ii) costs associated with the acquisition such as

transaction-related costs or restructuring costs will be separately

recorded from the acquisition and expensed as incurred; (iii) any

excess of fair market value of the assets, liabilities and minority interests

acquired over the fair market value of the purchase price will be

recognized as a bargain purchase and a gain recorded at the acquisition

date; and (iv) contractual contingencies resulting in potential future

assets or liabilities will be recorded at fair market value at the date of

acquisition. SFAS 141(R) applies prospectively to business combinations

for which the acquisition date is on or aer the beginning of the rst

annual reporting period beginning on or aer December 15, 2008. An

entity may not apply SFAS 141(R) before that date.

e FASB issued Statement of Financial Accounting Standards No.

160, “Noncontrolling Interests in Consolidated Financial Statements”

(SFAS 160) during the fourth quarter 2007. SFAS 160 enhances

disclosures surrounding minority interests in the balance sheet,

income statement and statement of comprehensive income. SFAS 160

will also require a parent to record a gain or loss when a subsidiary in

which it retains a minority interest is deconsolidated from the parent

company. SFAS 160 applies prospectively to business combinations

for which the acquisition date is on or aer the beginning of the rst

annual reporting period beginning on or aer December 15, 2008. An

entity may not apply SFAS 160 before that date.

In April 2007 the FASB issued Sta Position No. 39-1, “Amendment

of FASB Interpretation No. 39” (FSP FIN 39-1). FSP FIN 39-1 allows an

entity to oset the fair value of a receivable or payable against the fair

value of a derivative that is executed with the same counterparty under

a master netting arrangement. is guidance becomes eective for scal

years beginning aer November 15, 2007. Entergy does not expect these

provisions to have a material eect on it its nancial position.

Management’s Financial Discussion and Analysis concluded