Clearwire 2007 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2007 Clearwire annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

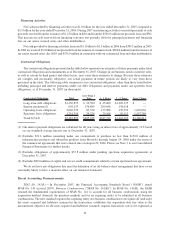

As such, we determined that the market approach was a more accurate method of estimating fair value and relied on

the income approach for corroboration only.

Accounting for Spectrum Licenses and Leases

We have two types of arrangements for spectrum licenses in the United States: direct licenses from the FCC

which we own and leases or subleases from third parties that own or lease one or more FCC licenses.

The owned FCC licenses in the United States and internationally are accounted for as intangible assets with

indefinite lives in accordance with the provisions of SFAS No. 142, Goodwill and Other Intangible Assets

(“SFAS No. 142”). In accordance with SFAS No. 142, intangible assets with indefinite useful lives are not

amortized but must be assessed for impairment annually or more frequently if an event indicates that the asset might

be impaired. We performed our annual impairment test of indefinite lived intangible assets as of October 1, 2007

and concluded that there was no impairment of these intangible assets. For leases involving significant up-front

payments, we account for such payments as prepaid spectrum license fees.

We account for the spectrum lease arrangements as executory contracts which are similar to operating leases.

For leases containing scheduled rent escalation clauses we record minimum rental payments on a straight-line basis

over the terms of the leases, including the renewal periods as appropriate.

Deferred Tax Asset Valuation Allowance

A valuation allowance is provided for deferred tax assets if it is more likely than not that these items will either

expire before we are able to realize their benefit, or that future deductibility is uncertain. In accordance with

SFAS No. 109, Accounting for Income Taxes, we record net deferred tax assets to the extent we believe these assets

will more likely than not be realized. In making such determination, we consider all available positive and negative

evidence, including our limited operating history, scheduled reversals of deferred tax liabilities, projected future

taxable income/loss, tax planning strategies and recent financial performance. We have recorded a valuation

allowance for net deferred tax assets, which was approximately $441.4 million and $170.8 million as of

December 31, 2007 and 2006, respectively.

Investments

SFAS No. 115, Accounting for Certain Investments in Debt and Equity Securities, and SAB No. 59,

Accounting for Non-current Marketable Equity Securities, provide guidance on determining when an investment

is other-than-temporarily impaired. We classify marketable debt and equity securities that are available for current

operations as short-term available-for-sale investments, and are stated at fair value. Unrealized gains and losses are

recorded as a separate component of accumulated other comprehensive income (loss). Losses are recognized when

a decline in fair value is determined to be other-than-temporary. Realized gains and losses are determined on the

basis of the specific identification method. We review our short-term and long-term investments on an ongoing basis

for indicators of other-than-temporary impairment, and this determination requires significant judgment.

We have an investment portfolio comprised of marketable debt and equity securities including commercial

paper, corporate bonds, municipal bonds, auction rate securities and other securities. The value of these securities is

subject to market volatility for the period we hold these investments and until their sale or maturity. We recognize

realized losses when declines in the fair value of our investments below their cost basis are judged to be other-than-

temporary. In determining whether a decline in fair value is other-than-temporary, we consider various factors

including market price (when available), investment ratings, the financial condition and near-term prospects of the

issuer, the length of time and the extent to which the fair value has been less than our cost basis, and our intent and

ability to hold the investment until maturity or for a period of time sufficient to allow for any anticipated recovery in

market value. We make significant judgments in considering these factors. If it is judged that a decline in fair value

is other-than-temporary, the investment is valued at the current estimated fair value and a realized loss equal to the

decline is reflected in the consolidated statement of operations.

In determining fair value, we use quoted prices in active markets where such prices are available, or we use

models to estimate fair value using various methods including the market, income and cost approaches. For

46