Cigna 2011 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2011 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

119CIGNA CORPORATION2011 Form10K

PART II

ITEM 8 Financial Statements and Supplementary Data

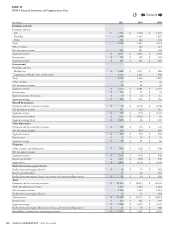

Premiums and fees, mail order pharmacy revenues and other revenues by product type were as follows for the years ended December31:

(In millions)

2011 2010 2009

Medical $ 14,568 $ 14,253 $ 12,089

Disability 1,280 1,162 1,063

Supplemental Health, Life, and Accident 3,103 2,839 2,748

Mail order pharmacy 1,447 1,420 1,282

Other 392 399 261

TOTAL $ 20,790 $ 20,073 $ 17,443

Concentration of risk. For theCompany’s International segment, South

Korea is the single largest geographic market. South Korea generated

31% of the segment’s revenues and 51% of the segment’s earnings

in 2011. South Korea generated 32% of the segment’s revenues and

49% of the segment’s earnings in 2010. Due to the concentration

of business in South Korea, the International segment is exposed to

potential losses resulting from economic and geopolitical developments

in that country, as well as foreign currency movements aecting the

South Korean currency, which could have a signicant impact on the

segment’s results and the Company’s consolidated nancial results.

NOTE 23 Contingencies and Other Matters

e Company, through its subsidiaries, is contingently liable for various

guarantees provided in the ordinary course of business.

A. Financial Guarantees Primarily Associated

with the Sold Retirement Benefits

Business

Separate account assets are contractholder funds maintained in accounts

with specic investment objectives. e Company records separate

account liabilities equal to separate account assets. In certain cases,

primarily associated with the sold retirement benets business (which

was sold in April2004), the Company guarantees a minimum level

of benets for retirement and insurance contracts, written in separate

accounts. e Company establishes an additional liability if management

believes that the Company will be required to make a payment under

these guarantees.

e Company guarantees that separate account assets will be sucient

to pay certain retiree or life benets. e sponsoring employers are

primarily responsible for ensuring that assets are sucient to pay

these benets and are required to maintain assets that exceed a certain

percentage of benet obligations. is percentage varies depending on

the asset class within a sponsoring employer’s portfolio (for example,

a bond fund would require a lower percentage than a riskier equity

fund) and thus will vary as the composition of the portfolio changes.

If employers do not maintain the required levels of separate account

assets, the Company or an aliate of the buyer has the right to redirect

the management of the related assets to provide for benet payments.

As of December31,2011, employers maintained assets that exceeded

the benet obligations. Benet obligations under these arrangements

were $1.7billion as of December31,2011. As of December31,2011,

approximately 75% of these guarantees are reinsured by an aliate of the

buyer of the retirement benets business. e remaining guarantees are

provided by the Company with minimal reinsurance from third parties.

ere were no additional liabilities required for these guarantees as of

December31,2011. Separate account assets supporting these guarantees

are classied in Levels 1 and 2 of the GAAP fair value hierarchy. See

Note10 for further information on the fair value hierarchy.

e Company does not expect that these nancial guarantees will have

a material eect on the Company’s consolidated results of operations,

liquidity or nancial condition.

B. Guaranteed Minimum Income Benefit

Contracts

e Company’s reinsurance operations, which were discontinued in

2000 and are now an inactive business in run-o mode, reinsured

minimum income benets under certain variable annuity contracts

issued by other insurance companies. A contractholder can elect the

guaranteed minimum income benet (“GMIB”) within 30days of any

eligible policy anniversary after a specied contractual waiting period.

e Company’s exposure arises when the guaranteed annuitization

benet exceeds the annuitization benet based on the policy’s current

account value. At the time of annuitization, the Company pays the

excess (if any) of the minimum benet guaranteed under the contract

over the benet based on the current account value in a lump sum to

the direct writing insurance company.

In periods of declining equity markets or declining interest rates, the

Company’s GMIB liabilities increase. Conversely, in periods of rising

equity markets and rising interest rates, the Company’s liabilities for

these benets decrease.

e Company estimates the fair value of the GMIB assets and liabilities

using assumptions for market returns and interest rates, volatility of

the underlying equity and bond mutual fund investments, mortality,

lapse, annuity election rates, non-performance risk, and risk and prot

charges. See Note10 for additional information on how fair values

for these liabilities and related receivables for retrocessional coverage

are determined.

The Company is required to disclose the maximum potential

undiscounted future payments for GMIB contracts. Under these

guarantees, the future payment amounts are dependent on equity

and bond fund market and interest rate levels prior to and at the

date of annuitization election, which must occur within 30days of a

policy anniversary, after the appropriate waiting period. erefore, the

future payments are not xed and determinable under the terms of

Contents

Q