WeightWatchers 2011 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2011 WeightWatchers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

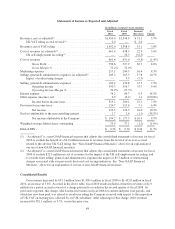

for each franchise right acquired is the country corresponding to the acquired franchise territory. The carrying

values of these franchise rights acquired in the United States, Canada, United Kingdom, Australia/New Zealand

and other countries at December 31, 2011 were $656.6 million, $70.7 million, $16.6 million, $15.2 million and

$4.9 million, respectively, totaling $764.0 million.

We estimate future cash flows for each unit of accounting by utilizing the historical cash flows attributable

to the rights in that country and then applying a growth rate using a blend of the historical operating income

growth rates for such country and expected future operating income growth rates for such country. We utilize

operating income as the basis for measuring our potential growth because we believe it is the best indicator of the

performance of our business. For fiscal 2011, the blended growth rates used in our discounted cash flow analysis

ranged from approximately 3% to approximately 20%. For fiscal 2010, the blended growth rates used in our

discounted cash flow analysis ranged from approximately 5% to approximately 26%. We then discount the

estimated future cash flows utilizing a discount rate. The discount rate is calculated using the average cost of

capital, which includes the cost of equity and the cost of debt. The cost of equity is determined by combining a

risk-free rate of return and a market risk premium. The risk-free rate of return is generally determined based on

the average rate of long-term Treasury securities. The market risk premium is generally determined by reviewing

external market data. When appropriate, we further adjust the resulting combined rate to account for certain

entity-specific factors such as maturity of the market in order to determine the utilized discount rate. The cost of

debt is our average borrowing rate for the period. The discount rates used in our fiscal 2011 year-end impairment

test and our fiscal 2010 year-end impairment test averaged approximately 11.3% and 10.5%, respectively.

At the end of fiscal 2011, we estimated that approximately 90% of the carrying value of our franchise rights

acquired had a fair value of at least three times their respective carrying amounts. In the United States, the region

which held approximately 86% of the franchise rights acquired, the aggregate fair value of our franchise rights

acquired was approximately three times the aggregate carrying value. Given that there is a significant difference

between the fair value and carrying value of our franchise rights acquired, we believe there are currently no

reasonably likely changes in assumptions that would cause an impairment.

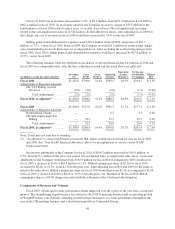

Derivative Instruments and Hedging

We enter into interest rate swaps to hedge a substantial portion of our variable rate debt. We record all

derivative financial instruments on the consolidated balance sheet at fair value as either assets or liabilities. Fair

value adjustments for qualifying derivative instruments are recorded as a component of other comprehensive

income and will be included in earnings in the periods in which earnings are affected by the hedged item.

Income Taxes

Deferred income taxes result primarily from temporary differences between financial and tax reporting. If it

is more likely than not that some portion of a deferred tax asset will not be realized, a valuation allowance is

recognized. We consider historic levels of income, estimates of future taxable income and feasible tax planning

strategies in assessing the need for a tax valuation allowance.

Capitalized Software Development

We capitalize certain software costs incurred in connection with developing or obtaining software for

internal use. These costs are amortized over a period of three to five years, the estimated useful life of the

software. We periodically evaluate for impairment capitalized software development costs by considering,

among other factors, whether the software is still expected to provide substantive service potential, and whether a

significant change is being made or will be made to the software.

40