Tyson Foods 2003 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2003 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

36 Tyson Foods, Inc.

notes to consolidated financial statements

TYSON FOODS, INC. 2003 ANNUAL REPORT

Goodwill and Other Intangible Assets: Goodwill and

indefinite life intangible assets are recorded at fair value

and not amortized, but are reviewed for impairment at

least annually or more frequently if impairment indicators

arise, as required by SFAS No. 142. Goodwill has been

allocated to and tested for impairment by reporting unit

based on fair value of identifiable assets. This goodwill is

not deductible for income tax purposes. For fiscal year

2001, goodwill arising prior to the IBP transaction was

amortized on a straight-line basis over periods ranging

from 15 to 40 years. Had the provisions of SFAS No. 142

been in effect during fiscal year 2001, a reduction in amorti-

zation expense and an increase to net income of $30 million

or $0.14 per diluted share, would have been recorded. At

September 27, 2003, and September 28, 2002, the accumu-

lated amortization of goodwill was $286 million.

Amount of goodwill by segment at September 27, 2003,

and September 28, 2002, was as follows:

in millions 2003 2002

Chicken $ 936 $ 917

Beef 1,306 1,306

Pork 350 350

Prepared Foods 60 60

Total $2,652 $ 2,633

At September 27, 2003, the gross carrying value of intan-

gible assets consisted of $100 million of trademarks,

$87 million of patents and $13 million of supply contracts

with accumulated amortization of $12 million and $6 mil-

lion for patents and supply contracts, respectively. At

September 28, 2002, the gross carrying value of intan-

gible assets consisted of $100 million of trademarks,

$87 million of patents and $13 million of supply contracts

with accumulated amortization of $6 million and $4 million

for patents and supply contracts, respectively. Amortization

expense on combined patents and supply contracts of

$8 million and $9 million was recognized during 2003 and

2002, respectively. Amortization expense on intangible

assets is estimated to be $8 million for 2004, 2005 and 2006,

and $6 million for 2007 and 2008. Patents and supply

contracts are amortized using the straight-line method

over their estimated period of benefit of 15 years and

five years, respectively.

Investments: The Company has investments in joint

ventures and other entities. The Company uses the cost

method of accounting where its voting interests are less

than 20 percent, and the equity method of accounting

where its voting interests are in excess of 20 percent but

not greater than 50 percent. The Company’s underlying

share of each entity’s equity is reported in the consoli-

dated balance sheet in the line item Other Assets.

Accrued Self Insurance: Insurance expense for casualty

claims and employee-related health care benefits are esti-

mated using historical experience and actuarial estimates.

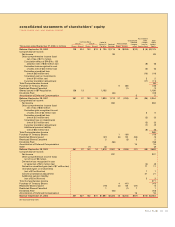

Capital Stock: Holders of Class B common stock (Class B

stock) may convert such stock into Class A common

stock (Class A stock) on a share-for-share basis. Holders

of Class B stock are entitled to 10 votes per share while

holders of Class A stock are entitled to one vote per

share on matters submitted to shareholders for approval.

Cash dividends cannot be paid to holders of Class B

stock unless they are simultaneously paid to holders of

Class A stock. The per share amount of the cash dividend

paid to holders of Class B stock cannot exceed 90% of the

cash dividend simultaneously paid to holders of Class A

stock. The Company pays quarterly cash dividends to Class

A and Class B shareholders. The Company paid Class A

dividends per share of $0.16 and Class B dividends per

share of $0.144 in fiscal years 2003, 2002 and 2001.

Stock Options: On December 29, 2002, the Company

adopted Financial Accounting Standards No. 148,

“Accounting for Stock-Based Compensation–Transition

and Disclosure” (SFAS No. 148). SFAS No. 148, which

amended FASB Statement No. 123, “Accounting for

Stock-Based Compensation,” does not require use of

the fair value method of accounting for stock-based

employee compensation. The Company applies

Accounting Principles Board Opinion No. 25 and related

interpretations in accounting for its employee stock

option plans. Accordingly, no compensation expense

was recognized for its stock option plans. Had compen-

sation cost for the employee stock option plans been