Tyson Foods 2003 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2003 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

26 Tyson Foods, Inc.

management’s discussion and analysis

TYSON FOODS, INC. 2003 ANNUAL REPORT

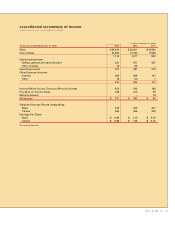

Beef segment sales were $10.5 billion, including beef

case-ready sales of $795 million and international beef

sales of $1.4 billion. Beef segment operating income

totaled $220 million. The Beef segment resulted from the

acquisition of IBP in the fourth quarter of fiscal 2001.

Pork segment sales including IBP’s pork processing

revenues were $2.5 billion compared to $619 million in

2001, including fiscal 2002 pork case-ready sales of

$145 million and international pork sales of $248 million.

Pork segment operating income decreased $2 million

from 2001. Sales and operating income were positively

affected by the inclusion of the IBP pork processing

results in fiscal 2002. However, both were impacted

by the negative results of the live swine operation.

Operating income was also affected by the restructuring

charge related to the Company’s live swine operation

of approximately $26 million in the fourth quarter of

fiscal 2002.

Prepared Foods segment sales increased $2.3 billion

compared to 2001. The Prepared Foods segment operat-

ing income increased $143 million. The increase in both

sales and operating income is primarily due to the

inclusion of IBP results. Operating income was also

influenced by lower and more stable raw material prices

and improvement in product mix. These increases were

partially offset by the Thomas E. Wilson write-down of

$27 million related to the discontinuation of the brand.

Other segment operating income increased $64 million

primarily due to the partial settlement of approximately

$30 million received in the third quarter of fiscal 2002

related to vitamin antitrust litigation combined with prior

year IBP merger related expenses of $19 million.

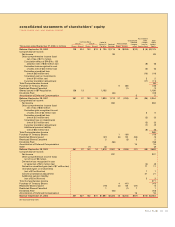

ACQUISITIONS

In August 2001, the Company acquired 50.1% of IBP by

paying approximately $1.7 billion in cash. In September

2001, the Company issued approximately 129 million

shares of Class A stock, with a fair value of approximately

$1.2 billion, to acquire the remaining IBP shares, and

assumed approximately $1.7 billion of IBP debt. The total

acquisition cost of approximately $4.6 billion was

accounted for as a purchase in accordance with SFAS

No. 141, “Business Combinations.” Accordingly, the

tangible and identifiable intangible assets and liabilities

have been adjusted to fair values with the remainder of

the purchase price recorded as goodwill. The allocation

of the purchase price has been completed.

In May 2002, the Company acquired the assets of Millard

Processing Services, a bacon processing operation, for

approximately $73 million in cash. The acquisition has

been accounted for as a purchase, and goodwill of

approximately $14 million has been recorded.

DISPOSITION

In September 2002, the Company completed the sale of

its Specialty Brands, Inc. subsidiary. The subsidiary had

been acquired with the IBP acquisition and its results of

operations were included in the Company’s Prepared

Foods segment. The Company received cash proceeds of

approximately $131 million, which were used to reduce

indebtedness, and recognized a pretax gain of $22 million.

Specialty Brands, Inc.’s sales and operating income for the

year ended September 28, 2002, were $244 million and

$2 million, respectively.

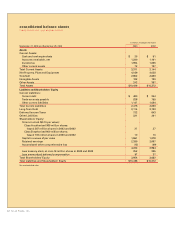

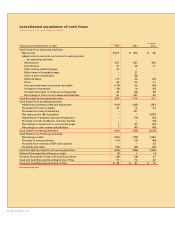

LIQUIDITY AND CAPITAL RESOURCES

Cash provided by operations continues to be the

Company’s primary source of funds to finance operating

requirements and capital expenditures. In 2003, net cash

of $820 million was provided by operating activities,

down $354 million from 2002. The decrease from fiscal

2002 is primarily due to a net change in working capital of

$423 million and a decrease in net income of $46 million,

partially offset by an increase in deferred taxes of $91 mil-

lion. The change in working capital is primarily due to

increased accounts receivable resulting from increased

sales and increased inventory values, as well as the

timing of cash receipts and payments related to other

working capital items. The Company’s foreseeable cash

needs for operations and capital expenditures are

expected to continue to be met through cash flows pro-

vided by operating activities. Additionally, at September 27,

2003, the Company had borrowing capacity of $1.5 billion

consisting of $705 million available under its $1 billion

unsecured revolving credit facilities and $750 million

under its accounts receivable securitization. At September

27, 2003, the Company had construction projects in