TripAdvisor 2015 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2015 TripAdvisor annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

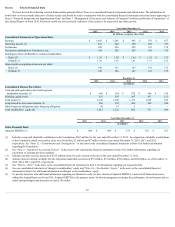

|

|

creditmarkets,therecanbenoassurancethatsufficientfinancingwillbeavailableondesirableorevenanytermstofundinvestments,acquisitions,stock

repurchases,dividends,debtrefinancingorextraordinaryactionsorthatcounterpartiesinanysuchfinancingswouldhonortheircontractualcommitments.

We have indebtedness which could adversely affect our business and financial condition.

Wecurrentlyhaveoutstandingapproximately$200millioninlong-termdebt.Risksrelatingtoourindebtednessinclude:

·Increasingourvulnerabilitytogeneraladverseeconomicandindustryconditions;

·Requiringustodedicateaportionofourcashflowfromoperationstoprincipalandinterestpaymentsonourindebtedness,therebyreducingthe

availabilityofcashflowtofundworkingcapital,capitalexpenditures,acquisitionsandinvestmentsandothergeneralcorporatepurposes;

·Makingitmoredifficultforustooptimallycapitalizeandmanagethecashflowforourbusinesses;

·Limitingourflexibilityinplanningfor,orreactingto,changesinourbusinessesandthemarketsinwhichweoperate;

·Possiblyplacingusatacompetitivedisadvantagecomparedtoourcompetitorsthathavelessdebt;

·Limitingourabilitytoborrowadditionalfundsortoborrowfundsatratesoronothertermsthatwefindacceptable;and

·Exposingustotheriskofincreasedinterestratesbecauseouroutstandingdebtisexpectedtobesubjecttovariableratesofinterest.

Inaddition,itispossiblethatwemayneedtoincuradditionalindebtednessinthefutureintheordinarycourseofbusiness.Thetermsofourrevolving

creditfacilitywillallowustoincuradditionaldebtsubjecttocertainlimitations;however,thereisnoassurancethatadditionalfinancingwillbeavailabletouson

termsfavorabletous,ifatall.Inaddition,ifnewdebtisaddedtocurrentdebtlevels,therisksdescribedabovecouldintensify.

The agreements that govern our revolving credit facility contain various covenants that limit our discretion in the operation of our business and also require us

to meet financial maintenance tests and other covenants. The failure to comply with such tests and covenants could have a material adverse effect on us.

Wearepartytoacreditagreementprovidingfortherevolvingcreditfacility.Theagreementsthatgoverntherevolvingcreditfacilitycontainvarious

covenants,includingthosethatlimitourabilityto,amongotherthings:

·Incurindebtedness;

·Paydividendson,redeemorrepurchaseourcapitalstock;

·Enterintocertainassetsaletransactions,includingpartialorfullspin-offtransactions;

·Enterintosecuredfinancingarrangements;

·Enterintosaleandleasebacktransactions;and

·Enterintounrelatedbusinesses.

Thesecovenantsmaylimitourabilitytooptimallyoperateourbusiness.Inaddition,ourrevolvingcreditfacilityrequiresthatwemeetcertainfinancial

tests,includingaleverageratiotest.Anyfailuretocomplywiththerestrictionsofourcreditfacilitymayresultinaneventofdefaultundertheagreements

governingsuchfacilities.Suchdefaultmayallowthecreditorstoacceleratethedebtincurredthereunder.Inaddition,lendersmaybeabletoterminateany

commitmentstheyhadmadetosupplyuswithfurtherfunds(includingperiodicrolloversofexistingborrowings).

Our effective tax rate is impacted by a number of factors that could have a material impact on our financial results and could increase the volatility of those

results.

Duetotheglobalnatureofourbusiness,wearesubjecttoincometaxesintheUnitedStatesandotherforeignjurisdictions.Intheeventweincurnetincome

incertainjurisdictionsbutincurlossesinotherjurisdictions,wegenerallycannotoffsettheincomefromonejurisdictionwiththelossfromanother,whichcould

increaseoureffectivetaxrate.Furthermore,significantjudgmentisrequiredtocalculateourworldwideprovisionforincometaxes.Intheordinarycourseofour

businesstherearemanytransactionsandcalculationswheretheultimatetaxdeterminationisuncertain.Byvirtueofourpreviouslyfiledseparatecompanyand

consolidatedincometaxreturnswithExpediaweareroutinelyunderauditbyfederal,stateandforeigntaxingauthorities.Althoughwebelieveourtaxestimates

arereasonable,thefinaldeterminationofauditscouldbemateriallydifferentfromourhistoricalincometaxprovisions

21