Thrifty Car Rental 2011 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2011 Thrifty Car Rental annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS

Overview

The Company operates two value rental car brands, Dollar and Thrifty. The majority of its customers

pick up their vehicles at airport locations. Both brands are value priced and the Company seeks to

be the industry’s low cost provider. Leisure customers typically rent vehicles for longer periods than

business customers, resulting in lower costs per transaction due to less frequent operational

interaction.

Both Dollar and Thrifty operate through a network of company-owned stores and franchisees. The

majority of the Company’s revenue is generated from renting vehicles to customers through

company-owned stores, with lesser amounts generated through parking income, vehicle leasing,

royalty fees and services provided to franchisees.

The Company’s profitability is primarily a function of the volume and pricing of rental transactions,

vehicle utilization rates and depreciation expense. Significant changes in the purchase or sales price

of vehicles or interest rates can also have a significant effect on the Company’s profitability,

depending on the ability of the Company to adjust its pricing for these changes. The Company’s

business requires significant expenditures for vehicles and, consequently, requires substantial

liquidity to finance such expenditures.

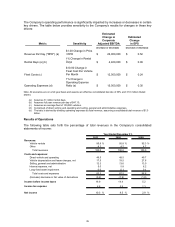

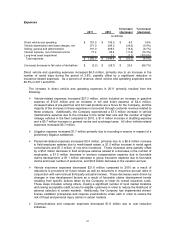

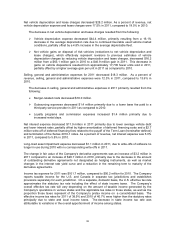

In 2011, the Company’s vehicle rental revenues increased when compared to 2010, primarily due to

a 3.8% increase in the number of rental days, partially offset by a 2.9% decrease in average revenue

per day.

During 2011, expenses declined 4.0% compared to 2010. The Company had lower net vehicle

depreciation and lease charges primarily due to lower depreciation rates per vehicle resulting from

continued favorable conditions in the used car market, mix optimization through a more diversified

fleet and improved remarketing efforts. Selling, general and administrative expenses decreased

primarily due to lower merger-related costs. Net interest expense decreased primarily due to lower

average vehicle debt and lower interest rates. Additionally, the Company experienced increases in

the fair value of derivatives in 2011 and 2010 of $3.2 million and $28.7 million, respectively.

The combination of these factors contributed to net income of $159.6 million for the year ended

December 31, 2011, compared to net income of $131.2 million for the year ended December 31,

2010. Excluding the change in fair value of derivatives and non-cash charges related to the

impairment of long-lived assets, net of tax, non-GAAP net income was $157.7 million for the year

ended December 31, 2011 compared to non-GAAP net income of $115.0 million for the year ended

December 31, 2010. Corporate Adjusted EBITDA for 2011 was $298.6 million compared to $235.7

million in 2010. Additionally, the Company incurred $4.6 million in merger-related expenses for the

year ended December 31, 2011, compared to $22.6 million for the year ended December 31, 2010.

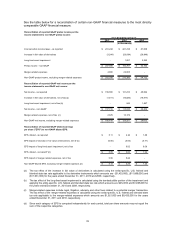

Reconciliations of non-GAAP financial measures to the comparable measures calculated in

accordance with generally accepted accounting principles in the United States (“GAAP”) are

presented below.

Use of Non-GAAP Measures for Measuring Results

Non-GAAP pretax income, non-GAAP net income and non-GAAP EPS exclude the impact of the

(increase) decrease in fair value of derivatives and the impact of long-lived asset impairments, net of

related tax impact (as applicable), from the reported GAAP measures and are further adjusted to

exclude merger-related expenses. Due to volatility resulting from the mark-to-market treatment of

the derivatives and the non-operating nature of the non-cash impairments and merger-related

expenses, the Company believes these non-GAAP measures provide an important assessment of

year-over-year operating results.

32