Starwood 2006 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2006 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

|

|

For the year ended December 31, 2006, the loss on disposition represents a $2 million tax assessment

associated with the disposition of the Company’s former gaming business in 1999.

For the year ended December 31, 2005, the loss from operations represents a $2 million sales and use tax

assessment related to periods prior to the Company’s disposal of its gaming business in 1999, offset by a $1 million

income tax benefit related to this business.

For the year ended December 31, 2004, the net gain on disposition primarily consists of the reversal of

$10 million of reserves set up in conjunction with the sale of the Company’s former gaming business in 1999. The

related contingencies were resolved in January 2005 and, therefore, the reserves are no longer required. The gain on

disposition also includes a tax benefit of $16 million associated with the disposition of the Company’s former

gaming business as a result of the favorable resolution of certain tax matters.

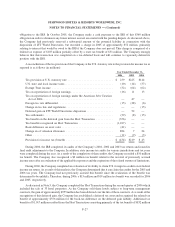

Note 17. Employee Benefit Plans

Adoption of SFAS No. 158. On December 31, 2006, the Company adopted the recognition and disclosure

provisions of SFAS No. 158. SFAS No. 158 required the Company to recognize the funded status (i.e., the difference

between the fair value of plan assets and the projected benefit obligations) of its pension plans in the December 31,

2006 consolidated balance sheet, with a corresponding adjustment to accumulated other comprehensive income, net

of tax. The adjustment to accumulated other comprehensive income at adoption represents the net unrecognized

actuarial losses, which were previously netted against the plan’s funded status in the Company’s consolidated

balance sheet pursuant to the provisions of SFAS No. 87. These amounts will be subsequently recognized as net

periodic pension cost pursuant to the Company’s historical accounting policy for amortizing such amounts. Further,

actuarial gains and losses that arise in subsequent periods and are not recognized as net periodic pension cost in the

same periods will be recognized as a component of other comprehensive income. Those amounts will be

subsequently recognized as a component of net periodic pension cost on the same basis as the amounts recognized

in accumulated other comprehensive income at adoption of SFAS No. 158.

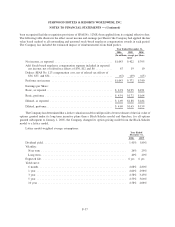

The incremental effects of adopting the provisions of SFAS No. 158 on the Company’s consolidated balance

sheet at December 31, 2006 are presented in the following table (in millions). The adoption of SFAS No. 158 had no

effect on the Company’s consolidated statement of income for the year ended December 31, 2006, or for any prior

period presented, and it will not effect the Company’s operating results in future periods. Had the Company not been

required to adopt SFAS No. 158 at December 31, 2006, it would have recognized an additional minimum liability

pursuant to the provisions of SFAS No. 87. The effect of recognizing the additional minimum liability is included in

table below in the column labeled “Prior to Application of SFAS No. 158.”

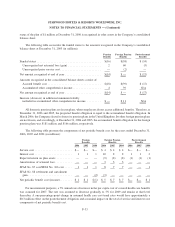

Prior to

Adopting

SFAS

No. 158

Effect of

Adopting

SFAS

No. 158

As

Reported

Prior to

Adopting

SFAS

No. 158

Effect of

Adopting

SFAS

No. 158

As

Reported

Prior to

Adopting

SFAS

No. 158

Effect of

Adopting

SFAS

No. 158

As

Reported

Pension Benefits Foreign Pension Benefits Postretirement Benefits

Other assets ............ $— $— $— $— $ 1 $ 1 $— $— $—

Accrued expenses ....... $— $ 1 $ 1 $— $— $— $— $— $—

Deferred income taxes .... $— $— $— $— $ 2 $ 2 $— $ 1 $ 1

Other liabilities ......... $18 $(2) $16 $24 $12 $36 $17 $(5) $12

Accumulated other

comprehensive income . . $ (4) $ 1 $ (3) $(38) $(12) $(50) $— $ 5 $ 5

Included in accumulated other comprehensive income at December 31, 2006 is unrecognized actuarial losses

of $48 million ($36 million, net of tax) that have not yet been recognized in net periodic pension cost. The actuarial

loss included in accumulated other comprehensive income and expected to be recognized in net periodic pension

cost during the year ended December 31, 2007 is $2 million ($2 million, net of tax).

F-31

STARWOOD HOTELS & RESORTS WORLDWIDE, INC.

NOTES TO FINANCIAL STATEMENTS — (Continued)