Starwood 2006 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2006 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

|

|

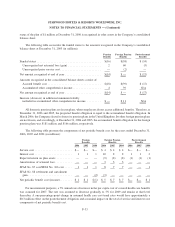

In November 2005, the Company securitized approximately $221 million of VOI notes receivable (the “2005

Securitization”), resulting in gross cash proceeds of approximately $197 million. The related gain of $24 million is

included in gain on sale of VOI notes receivable in the Company’s statements of income. In connection with the

2005 Securitization, the Company used a portion of the proceeds to repurchase all the remaining VOI notes

receivable sold under the 2004 Purchase Facility described below for approximately $64 million.

Key assumptions used in measuring the fair value of the Retained Interests at the time of the 2005

Securitization and at December 31, 2005, relating to the 2005 Securitization, were as follows: discount rate of

10%; annual prepayments, which yields an average expected life of the prepayable VOI notes receivable of

99 months; and expected gross VOI notes receivable balance defaulting as a percentage of the total initial pool of

11.0%. These key assumptions are based on the Company’s experience.

During 2004, the Company sold, in several sales, $113 million of VOI notes receivable pursuant to an

arrangement (the “2004 Purchase Facility”) with third party purchasers. The Company’s net cash proceeds received

from these sales were approximately $103 million. Total gains from these sales of $13 million are included in gain

on sale of VOI notes receivable in the Company’s statements of income in 2004. As discussed above, in connection

with the 2005 Securitization, the Company repurchased all the remaining VOI notes receivable sold under the 2004

Purchase Facility.

Key assumptions used in measuring the fair value of the Retained Interests at the time of sale and at

December 31, 2004 under the 2004 Purchase Facility were as follows: discount rate of 12%; annual prepayments,

which yields an average expected life of the prepayable VOI notes receivable of 99 months; and expected gross VOI

notes receivable balance defaulting as a percentage of the total initial pool of 15.1%. These key assumptions are

based on the Company’s experience.

At December 31, 2006, the aggregate outstanding principal balance of VOI notes receivable that have been

securitized or sold was $361 million. The principal amounts of those VOI notes receivables that were more than

90 days delinquent at December 31, 2006 was approximately $3 million.

Gross credit losses for all VOI notes receivable were $17 million, $17 million, and $22 million during 2006,

2005, and 2004, respectively.

The Company received aggregate cash proceeds of $36 million, $35 million and $32 million from the Retained

Interests during 2006, 2005, and 2004, respectively, and aggregate servicing fees of $4 million, $3 million and

$3 million related to these VOI notes receivable in 2006, 2005, and 2004, respectively.

At the time of each VOI notes receivable sale and at the end of each financial reporting period, the Company

estimates the fair value of its Retained Interests using a discounted cash flow model. All assumptions used in the

models are reviewed and updated, if necessary, based on current trends and historical experience.

At December 31, 2006, the Company completed a sensitivity analysis on the net present value of the Retained

Interests to measure the change in value associated with independent changes in individual key variables. The

methodology applied unfavorable changes for the key variables of expected prepayment rates, discount rates and

expected gross credit losses. The aggregate net present value and carrying value of Retained Interests at

December 31, 2006 was approximately $51 million. The decreases in value of the Retained Interests that would

result from various independent changes in key variables are shown in the chart that follows (dollar amounts are in

millions). These factors may not move independently of each other.

F-23

STARWOOD HOTELS & RESORTS WORLDWIDE, INC.

NOTES TO FINANCIAL STATEMENTS — (Continued)