Shutterfly 2010 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2010 Shutterfly annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

|

|

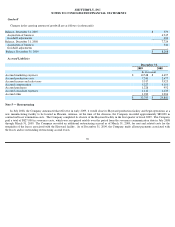

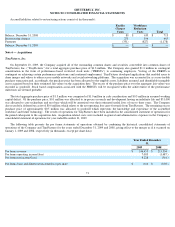

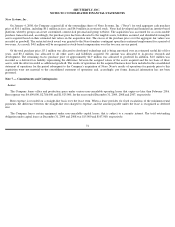

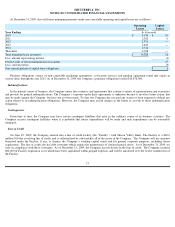

SHUTTERFLY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Effective January 1, 2009, the Company adopted an accounting standard which establishes accounting and reporting standards for the

noncontrolling interest in a subsidiary and for the deconsolidation of a subsidiary, as codified in ASC 810-10-

60 (formerly SFAS No. 160,

Accounting and Reporting on Non

-controlling Interest in Consolidated Financial Statements, an Amendment of ARB 51

). This accounting

standard states that accounting and reporting for minority interests are to be recharacterized as noncontrolling interests and classified as a

component of equity. The calculation of earnings per share continues to be based on income amounts attributable to the parent. The adoption of

these accounting updates did not have any impact on the Company’s consolidated financial statements.

Effective January 1, 2009, the Company adopted an accounting standard update regarding the determination of the useful life of intangible

assets. As codified in ASC 350-30-50 (formerly FSP No. 142-3, Determination of the Useful Life of Intangible Assets

), this update amends the

factors considered in developing renewal or extension assumptions used to determine the useful life of a recognized intangible asset under

intangibles accounting. It also requires a consistent approach between the useful life of a recognized intangible asset under prior business

combination accounting and the period of expected cash flows used to measure the fair value of an asset under the new business combinations

accounting (as currently codified under ASC 850). The update also requires enhanced disclosures when an intangible asset’

s expected future

cash flows are affected by an entity’

s intent and/or ability to renew or extend the arrangement. The adoption of these accounting updates did not

have any impact on the Company’s consolidated financial statements.

Effective January 1, 2009, the Company adopted a new accounting standard update regarding the accounting of defensive intangible

assets. This update, as codified in ASC 350-30 (formerly EITF No. 08-7, Accounting for Defensive Intangible Assets

), clarifies accounting for

defensive intangible assets subsequent to initial measurement. It applies to acquired intangible assets which an entity has no intention of actively

using, or intends to discontinue use of, the intangible asset but holds it to prevent others from obtaining access to it (i.e., a defensive intangible

asset). Under this update, a consensus was reached that an acquired defensive asset should be accounted for as a separate unit of accounting (i.e.,

an asset separate from other assets of the acquirer); and the useful life assigned to an acquired defensive asset should be based on the period

during which the asset would diminish in value. The adoption of these accounting updates did not have any impact on the Company’

s

consolidated financial statements.

Effective April 1, 2009, the Company adopted a new accounting standard for subsequent events, as codified in ASC 855-

10 (formerly

SFAS No. 165, Subsequent Events

). The update modifies the names of the two types of subsequent events either as recognized subsequent

events (previously referred to in practice as Type I subsequent events) or non-

recognized subsequent events (previously referred to in practice as

Type II subsequent events). In addition, the standard modifies the definition of subsequent events to refer to events or transactions that occur

after the balance sheet date, but before the financial statements are issued (for public entities) or available to be issued (for nonpublic entities). It

also requires the disclosure of the date through which subsequent events have been evaluated. The update did not result in significant changes in

the practice of subsequent event disclosures, and therefore the adoption did not have any impact on the Company’

s consolidated financial

statements.

Effective April 1, 2009, the Company adopted three accounting standard updates which were intended to provide additional application

guidance and enhanced disclosures regarding fair value measurements and impairments of securities. They also provide additional guidelines for

estimating fair value in accordance with fair value accounting. The first update, as codified in ASC 820-10-65 (formerly FSP No. 157-

4,

Determining Fair Value When the Volume and Level of Activity for the Asset or Liability Have Significantly Decreased and Identifying

Transactions That Are Not Orderly

), provides additional guidelines for estimating fair value in accordance with fair value accounting. The

second accounting update, as codified in ASC 320-10-65 (formerly FSP No. 115-2, Recognition and Presentation of Other-Than-

Temporary

Impairments)

, changes accounting requirements for other-than-temporary-

impairment (OTTI) for debt securities by replacing the current

requirement that a holder have the positive intent and ability to hold an impaired security to recovery in order to conclude an impairment was

temporary with a requirement that an entity conclude it does not intend to sell an impaired security and it will not be required to sell the security

before the recovery of its amortized cost basis. The third accounting update, as codified in ASC 825-10-

65 (formerly Accounting Principles

Board (“APB”) Opinion No. 28-1, Interim Disclosures about Fair Value of Financial Instruments)

, increases the frequency of fair value

disclosures. These updates were effective for fiscal years and interim periods ended after June 15, 2009. The adoption of these accounting

updates did not have any impact on the Company’s consolidated financial statements.

Effective July 1, 2009, the Company adopted The “FASB Accounting Standards Codification” and the Hierarchy of Generally Accepted

Accounting Principles (ASC 105), (formerly SFAS No. 168, The “FASB Accounting Standards Codification” and the Hierarchy of Generally

Accepted Accounting Principles

). This standard establishes only two levels of U.S. generally accepted accounting principles (“GAAP”),

authoritative and nonauthoritative. The Financial Accounting Standard Board (“FASB”) Accounting Standards Codification (the “Codification”)

became the source of authoritative, nongovernmental GAAP, except for rules and interpretive releases of the SEC, which are sources of

authoritative GAAP for SEC registrants. All other non-grandfathered, non-SEC accounting literature not included in the Codification became

nonauthoritative. The Company began using the new guidelines and numbering system prescribed by the Codification when referring to GAAP

in the third quarter of fiscal 2009. As the Codification was not intended to change or alter existing GAAP, it did not have any impact on the

Company’s consolidated financial statements.

65