Rosetta Stone 2014 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2014 Rosetta Stone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

|

|

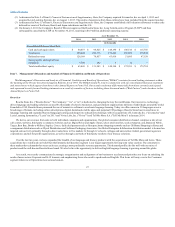

Table of Contents

• prudent and feasible tax planning strategies that would be implemented, if necessary, to protect against the loss of the deferred tax assets; and

• the effect of reversing taxable temporary differences.

The evaluation of the recoverability of the deferred tax assets requires that we weigh all positive and negative evidence to reach a conclusion that it is

more likely than not that all or some portion of the deferred tax assets will not be realized. The weight given to the evidence is commensurate with the extent

to which it can be objectively verified. The more negative evidence that exists, the more positive evidence is necessary and the more difficult it is to support

a conclusion that a valuation allowance is not needed. Our valuation allowance analysis considers a number of factors, including our cumulative losses in

recent years, our expectation of future taxable income and the time frame over which our net operating losses expire.

As of December 31, 2014, a full valuation allowance exists for the U.S., Korea, Japan, China, Hong Kong, Mexico, Spain and Brazil where we have

determined the deferred tax assets will not more likely than not be realized. Further, in France a partial valuation allowance has been recorded on deferred tax

assets we believe are not more likely than not to be realized.

The establishment of a valuation allowance has no effect on the ability to use the deferred tax assets in the future to reduce cash tax payments. We will

continue to assess the likelihood that the deferred tax assets will be realizable at each reporting period, and the valuation allowance will be adjusted

accordingly, which could materially affect our financial position and results of operations.

In presenting our financial statements in conformity with accounting principles generally accepted in the U.S., we are required to make estimates and

assumptions that affect the reported amounts of assets, liabilities, revenues, costs and expenses and related disclosures.

Some of the estimates and assumptions we are required to make relate to matters that are inherently uncertain as they pertain to future events. We base

these estimates and assumptions on historical experience or on various other factors that we believe to be reasonable and appropriate under the

circumstances. On an ongoing basis, we reconsider and evaluate our estimates and assumptions. Our future estimates may change if the underlying

assumptions change. Actual results may differ significantly from these estimates.

We believe that the critical accounting policies listed below involve our more significant judgments, assumptions and estimates and, therefore, could

have the greatest potential impact on our consolidated financial statements. In addition, we believe that a discussion of these policies is necessary for readers

to understand and evaluate our consolidated financial statements contained in this annual report on Form 10-K.

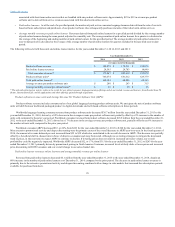

Our primary sources of revenue are web-based software subscriptions, online services, perpetual product software, and bundles of perpetual product

software and short-term online services. We also generate revenue from the sale of audio practice products, mobile applications, and professional services.

Revenue is recognized when all of the following criteria are met: there is persuasive evidence of an arrangement; the product has been delivered or services

have been rendered; the fee is fixed or determinable; and collectability is reasonably assured. Revenues are recorded net of discounts.

We identify the units of accounting contained within our sales arrangements and in doing so, we evaluate a variety of factors including whether the

undelivered element(s) have value to the customer on a stand-alone basis or if the undelivered element(s) could be sold by another vendor on a stand-alone

basis.

For multiple element arrangements that contain perpetual software products and related services, we allocate the total arrangement consideration to the

deliverables based on vendor-specific objective evidence of fair value ("VSOE"). We generate a substantial portion of consumer revenue from the CD and

digital download formats of the Rosetta Stone language-learning packaged software product which is a multiple-element arrangement that contains two

deliverables: perpetual software, which is delivered at the time of sale, and a short-term online service, which is considered a software-related element. The

online service includes short-term access to conversational coaching services. Because we only sell the perpetual language-learning software on a stand-

alone basis in our homeschool version, we do not have a sufficient concentration of stand-alone sales to establish VSOE for this element. Accordingly, we

allocate the arrangement consideration using the residual method based on the existence of VSOE of the undelivered element, the short-term online service.

We determine VSOE of the short-term online service by reference to the range of stand-alone renewal sales of the three-month online service. We review these

stand-alone

32