Pizza Hut 2006 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2006 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

60 YUM! BRANDS, INC.

DIRECT MARKETING COSTS We charge direct marketing costs

to expense ratably in relation to revenues over the year in which

incurred and, in the case of advertising production costs, in the

year the advertisement is first shown. Deferred direct marketing

costs, which are classified as prepaid expenses, consist of media

and related advertising production costs which will generally be

used for the first time in the next fiscal year and have historically

not been significant. To the extent we participate in advertis-

ing cooperatives, we expense our contributions as incurred.

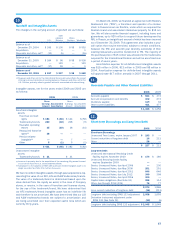

Our advertising expenses were $492 million, $497 million and

$458 million in 2006, 2005 and 2004, respectively. We report

substantially all of our direct marketing costs in occupancy and

other operating expenses.

RESEARCH AND DEVELOPMENT EXPENSES Research and

development expenses, which we expense as incurred, are

reported in G&A expenses. Research and development expenses

were $33 million, $33 million and $26 million in 2006, 2005 and

2004, respectively.

IMPAIRMENT OR DISPOSAL OF LONG-LIVED ASSETS In accor-

dance with SFAS No. 144, “Accounting for the Impairment or

Disposal of Long-Lived Assets” (“SFAS 144”), we review our long-

lived assets related to each restaurant to be held and used in

the business, including any allocated intangible assets subject to

amortization, semi-annually for impairment, or whenever events or

changes in circumstances indicate that the carrying amount of a

restaurant may not be recoverable. We evaluate restaurants using

a “two-year history of operating losses” as our primary indicator

of potential impairment. Based on the best information available,

we write down an impaired restaurant to its estimated fair market

value, which becomes its new cost basis. We generally measure

estimated fair market value by discounting estimated future cash

flows. In addition, when we decide to close a restaurant it is

reviewed for impairment and depreciable lives are adjusted based

on the expected disposal date. The impairment evaluation is

based on the estimated cash flows from continuing use through

the expected disposal date plus the expected terminal value.

We account for exit or disposal activities, including store

closures, in accordance with SFAS No. 146, “Accounting for Costs

Associated with Exit or Disposal Activities” (“SFAS 146”). Store

closure costs include costs of disposing of the assets as well

as other facility-related expenses from previously closed stores.

These store closure costs are generally expensed as incurred.

Additionally, at the date we cease using a property under an oper-

ating lease, we record a liability for the net present value of any

remaining lease obligations, net of estimated sublease income,

if any. Any subsequent adjustments to that liability as a result of

lease termination or changes in estimates of sublease income

are recorded in store closure costs. To the extent we sell assets,

primarily land, associated with a closed store, any gain or loss

upon that sale is also recorded in store closure costs (income).

Refranchising (gain) loss includes the gains or losses from

the sales of our restaurants to new and existing franchisees and

the related initial franchise fees, reduced by transaction costs. In

executing our refranchising initiatives, we most often offer groups

of restaurants. We classify restaurants as held for sale and sus-

pend depreciation and amortization when (a) we make a decision

to refranchise; (b) the stores can be immediately removed from

operations; (c) we have begun an active program to locate a buyer;

(d) significant changes to the plan of sale are not likely; and (e)

the sale is probable within one year. We recognize estimated

losses on refranchisings when the restaurants are classified as

held for sale. We also recognize as refranchising loss impair-

ment associated with stores we have offered to refranchise for a

price less than their carrying value, but do not believe have met

the criteria to be classified as held for sale. We recognize gains

on restaurant refranchisings when the sale transaction closes,

the franchisee has a minimum amount of the purchase price in

at-risk equity, and we are satisfied that the franchisee can meet

its financial obligations. If the criteria for gain recognition are not

met, we defer the gain to the extent we have a remaining financial

exposure in connection with the sales transaction. Deferred gains

are recognized when the gain recognition criteria are met or as our

financial exposure is reduced. When we make a decision to retain

a store, or group of stores, previously held for sale, we revalue

the store at the lower of its (a) net book value at our original sale

decision date less normal depreciation and amortization that

would have been recorded during the period held for sale or (b)

its current fair market value. This value becomes the store’s new

cost basis. We record any difference between the store’s carrying

amount and its new cost basis to refranchising gain (loss).

Considerable management judgment is necessary to esti-

mate future cash flows, including cash flows from continuing

use, terminal value, sublease income and refranchising pro-

ceeds. Accordingly, actual results could vary significantly from

our estimates.

IMPAIRMENT OF INVESTMENTS IN UNCONSOLIDATED AFFILIATES

We record impairment charges related to an investment in an

unconsolidated affiliate whenever events or circumstances

indicate that a decrease in the fair value of an investment has

occurred which is other than temporary. In addition, we evaluate

our investments in unconsolidated affiliates for impairment when

they have experienced two consecutive years of operating losses.

We recorded no impairment associated with our investments in

unconsolidated affiliates during the years ended December 30,

2006, December 31, 2005 and December 25, 2004.

Considerable management judgment is necessary to esti-

mate future cash flows. Accordingly, actual results could vary

significantly from our estimates.

GUARANTEES We account for certain guarantees in accor-

dance with FASB Interpretation No. 45, “Guarantor’s Accounting

and Disclosure Requirements for Guarantees, Including Indirect

Guarantees of Indebtedness to Others, an interpretation of FASB

Statements No. 5, 57 and 107 and a rescission of FASB Interpre-

tation No. 34” (“FIN 45”). FIN 45 elaborates on the disclosures

to be made by a guarantor in its interim and annual financial

statements about its obligations under guarantees issued. FIN

45 also clarifies that a guarantor is required to recognize, at

inception of a guarantee, a liability for the fair value of certain

obligations undertaken.

We have also issued guarantees as a result of assigning

our interest in obligations under operating leases as a condi-

tion to the refranchising of certain Company restaurants. Such

guarantees are subject to the requirements of SFAS No. 145,

“Rescission of FASB Statements No. 4, 44, and 64, Amendment

of FASB Statement No. 13, and Technical Corrections” (“SFAS

145”). We recognize a liability for the fair value of such lease

guarantees under SFAS 145 upon refranchising and upon any

subsequent renewals of such leases when we remain contin-

gently liable. The related expense in both instances is included

in refranchising gain (loss).