Pizza Hut 2006 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2006 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

44 YUM! BRANDS, INC.

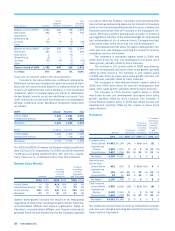

The funding rules for our pension plans outside of the

U.S. vary from country to country and depend on many factors

including discount rates, performance of plan assets, local

laws and tax regulations. Our most significant plans are in the

U.K., including a plan for which we assumed full liability upon

our purchase of the remaining fifty percent interest in our for-

mer Pizza Hut U.K. unconsolidated affiliate. During 2006, we

made a discretionary contribution of approximately $18 mil-

lion to our KFC U.K. pension plan in anticipation of certain

future funding requirements. Since our plan assets approxi-

mate our projected benefit obligation at year-end for this plan,

we do not anticipate any significant further, near term funding.

The projected benefit obligation of our Pizza Hut U.K. pension

plan exceeds plan assets by approximately $35 million. We

anticipate taking steps to reduce this deficit in the near term,

which could include a decision to partially or completely fund

the deficit in 2007. However, given the level of cash flows

from operations the Company anticipates generating in 2007,

any funding decision would not materially impact our ability to

maintain our planned levels of discretionary spending.

During 2006, Congress passed the Pension Protection

Act of 2006 (the “Act”) with the stated purpose of improving

the funding of America’s private pension plans. The Act intro-

duces new funding requirements for defined benefit pension

plans, introduces benefit limitations for certain under-funded

plans and raises tax deduction limits for contributions. The Act

applies to pension plan years beginning after December 31,

2007 and is applicable only to our U.S. Plan. We have pre-

liminarily reviewed the provisions of the Act to determine the

impact on the Company. Required funding under the Act will be

dependent upon many factors including our U.S. Plan’s future

funded status as well as discretionary contributions we may

choose to make. Based upon this preliminary review as well

as the current funded status of the U.S. Plan relative to our

level of annual operating cash flows, we do not believe that

required contributions under the Act would materially impact

our operating cash flows in any one given year.

Our postretirement plan is not required to be funded in

advance, but is pay as you go. We made postretirement bene-

fit payments of $4 million in 2006. See Note 15 for further

details about our pension and postretirement plans.

We have excluded from the contractual obligations table

payments we may make for: workers’ compensation, employ-

ment practices liability, general liability, automobile liability and

property losses (collectively “property and casualty losses”)

for which we are self-insured; employee healthcare and long-

term disability claims for which we are self-insured; and

income taxes and associated interest we may pay upon audit

by tax authorities of tax returns previously filed. The majority

of our recorded liability for self-insured employee health, long-

term disability and property and casualty losses represents

estimated reserves for incurred claims that have yet to be

filed or settled. We provide reserves for potential tax and

associated interest exposures when we consider it probable

that a taxing authority may take a sustainable position on a

matter contrary to our position.

Off-Balance Sheet Arrangements

We had provided approximately $16 million of partial guar-

antees of two franchisee loan pools related primarily to the

Company’s historical refranchising programs and, to a lesser

extent, franchisee development of new restaurants at Decem-

ber 30, 2006. In support of these guarantees, we posted

letters of credit of $4 million. We also provided a standby let-

ter of credit of $18 million, under which we could potentially

be required to fund a portion of one of the franchisee loan

pools. The total loans outstanding under these loan pools

were approximately $75 million at December 30, 2006.

Any funding under the guarantees or letters of credit

would be secured by the franchisee loans and any related

collateral. We believe that we have appropriately provided for

our estimated probable exposures under these contingent

liabilities. These provisions were primarily charged to net

refranchising loss (gain). New loans added to the loan pools

in 2006 were not significant.

Our unconsolidated affiliates have approximately $29 mil-

lion of short-term debt outstanding as of December 30, 2006,

none of which is guaranteed by YUM.

Accounting Pronouncements Adopted in the

Fourth Quarter of 2006

In the fourth quarter of 2006, we adopted Staff Account-

ing Bulletin No. 108, “Considering the Effects of Prior Year

Misstatements when Quantifying Misstatements in Current

Year Financial Statements” (“SAB 108”). SAB 108 provides

interpretive guidance on how the effects of the carryover or

reversal of prior year misstatements should be considered in

quantifying a current year misstatement for the purpose of

a materiality assessment. SAB 108 requires that registrants

quantify a current year misstatement using an approach that

considers both the impact of prior year misstatements that

remain on the balance sheet and those that were recorded in

the current year income statement. Historically, we quantified

prior year misstatements and assessed materiality based on

a current year income statement approach. The transition

provisions of SAB 108 permitted the Company to adjust for

the cumulative effect of uncorrected prior year misstatements

that were not material to any prior periods under our histori-

cal income statement approach but that were material under

the guidance in SAB 108 through retained earnings at the

beginning of 2006. See Note 2 for further discussion on the

impact of adopting SAB 108.

In the fourth quarter of 2006, we adopted the recogni-

tion and disclosure provisions of SFAS No. 158, “Employers’

Accounting for Defined Benefit Pension and Other Postretire-

ment Plans — an amendment of FASB Statements No. 87,

88, 106 and 132(R)” (“SFAS 158”). SFAS 158 required the

Company to recognize the funded status of its pension and

post-retirement plans in the December 30, 2006 Consolidated

Balance Sheet, with a corresponding adjustment to accumu-

lated other comprehensive income, net of tax. Gains or losses

and prior service costs or credits that arise in future years

will be recognized as a component of other comprehensive

income to the extent they have not been recognized as a com-

ponent of net periodic benefit cost. The impact of adopting

SFAS 158 has been included in the Company’s December 30,

2006 Consolidated Balance Sheet. See Notes 2 and 15 for

further discussion of the impact of adopting SFAS 158.

SFAS 158 also requires measurement of the funded sta-

tus of pension and postretirement plans as of the date of a