LensCrafters 2008 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2008 LensCrafters annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

expense. Related to the uncertain tax benefits noted above, the Company’s accrual for penalties and

interest during 2008 and 2007 was immaterial and, in total, as of December 31, 2008, the Company has

recognized a liability for penalties of approximately Euro 3.6 million and interest expense of approximately

Euro 7.5 million.

The Group is subject to taxation in Italy and foreign jurisdictions of which only the U.S. federal is significant.

Italian companies’ taxes are subject to review pursuant to Italian law. As of December 31, 2008, tax years

from 2003 through the most recent year were open for such review. At the date of December, 31 2008 no

Italian companies are subjected to a tax inspection. The previous tax inspections open in 2007 were closed

with no material liability for the Group.

The Group’s U.S. federal tax years for 2005, 2006 and 2007 are subject to examination by the tax authorities.

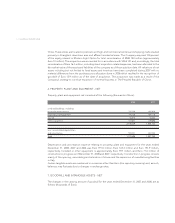

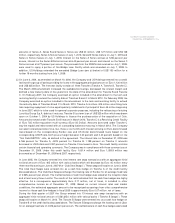

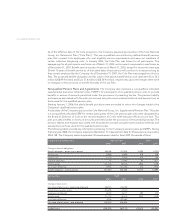

9. LONG-TERM DEBT

Long-term debt consists of the following (thousands of Euro):

NOTES TO CONSOLIDATED

FINANCIAL STATEMENTS |77 <

December 31,

2008 2007

Credit agreement with various Italian financial institutions (a) 400,000 185,000

Senior unsecured guaranteed notes (b) 213,196 97,880

Credit agreement with various financial institutions (c) 1,001,403 1,059,918

Other loans with banks and other third parties, interest

at various rates, payable in installments through 2014 (d) 4,314 4,894

Credit Agreement with various financial Institution

for Oakley acquisition (e) 1,185,482 1,369,582

Capital lease obligations, payable in installments through 2009 1,107 1,866

Total 2,805,502 2,719,140

Current maturities 286,213 792,617

Long-term debt 2,519,289 1,926,523

(a) In September 2003, the Company acquired its ownership interest of OPSM and more than 90 percent

of the performance rights and options of OPSM for an aggregate of AUD 442.7 million (Euro 253.7

million), including acquisition expenses. The purchase price was paid for with the proceeds of a credit

facility with Banca Intesa S.p.A. of Euro 200 million, in addition to other short-term lines available. The

credit facility included a Euro 150 million term loan, which required repayment of equal semi-annual

installments of principal of Euro 30 million starting on September 30, 2006 until the final maturity date.

Interest accrued on the term loan at Euribor (as defined in the agreement) plus 0.55 percent. The

revolving loan provided borrowing availability of up to Euro 50 million; amounts borrowed under the

revolving portion could be borrowed and repaid until final maturity. Interest accrued on the revolving

loan at Euribor (as defined in the agreement) plus 0.55 percent. The Company could select interest

periods of one, two or three months. The final maturity of the credit facility was September 30, 2008,

the credit facility was repaid in full. The credit facility contains certain financial and operating covenants.

The Company was in compliance with those covenants during 2008, prior to the final maturity date.

In June 2005, the Company entered into four interest rate swap transactions with various banks with an

aggregate initial notional amount of Euro 120 million which decreased by Euro 30 million every six months

starting on March 30, 2007. These swaps expired on September 30, 2008. The ineffectiveness of cash flow