LensCrafters 2008 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2008 LensCrafters annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

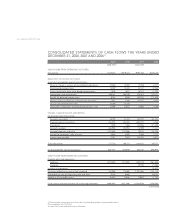

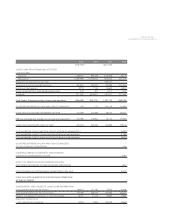

> 66 |ANNUAL REPORT 2008

standards that address fair value measurements. In February 2008, the FASB issued FASB Staff Position No.

157-1 (“FSP No. 157-1”),

Application of FASB Statement No. 157 to FASB Statement No. 13 and Other

Accounting Pronouncements that Address Fair Value Measurements for Purposes of Lease Classification or

Measurement under Statement 13

, and FSP No. 157-2,

Effective Date of FASB Statement 157

. FSP 157-1

amends SFAS No. 157 to exclude leases and lease transactions under FASB Statement No. 13. While FSP

157-2 amends the effective date of SFAS No. 157 for all non-financial assets and non-financial liabilities,

except those recognized or disclosed on a recurring basis (at least annually) until the beginning of the first

quarter of 2009. In October 2008, FASB issued FSP No. 157-3,

Determining the Fair Value of a Financial Asset

When the Market for that Asset is Not Active

, which clarifies how to calculate the fair value of financial asset

under certain conditions and gives an example of such. SFAS No 159 allows the Company to elect and record

at fair value many financial assets and liabilities and certain other items with the change being recorded in

earnings. This can be done on an instrument by instrument basis in most circumstances, is irrevocable after

elected for that instrument and must be applied to the entire instrument. The adoption of both of these

standards did not have a material effect on the consolidated financial statements. See Note 16.

Information expressed in US Dollars. The Company’s consolidated financial statements are stated in

Euro, the currency of the country in which the parent company is incorporated and operates. The

translation of Euro amounts into US Dollar amounts is included solely for the convenience of international

readers and has been made at the rate of Euro 1 to US Dollar 1.3919. Such rate was determined by using

the noon buying rate of the Euro to US Dollar as certified for customs purposes by the Federal Reserve

Bank of New York as of December 31, 2008. Such translations should not be construed as representations

that Euro amounts could be converted into US Dollars at that or any other rate.

Recent accounting pronouncements.

In December 2008, the FASB issued FASB Staff Position (“FSP”) 132(R)-1,

Employee Disclosures about

Postretirement Benefit Plan Assets

which requires enhanced disclosures on plan assets including fair value

measurements and categories of assets, investment policies and strategies and disclosures on

concentration of risks. The effective date for the enhanced disclosures about plan assets required by this

FSP shall be provided for fiscal years ending after December 15, 2009. The disclosure requirements are not

required for earlier periods that are presented for comparative purposes. The adoption is not expected to

have a material effect on the financial statements.

In November 2008, the Emerging Issues Task Force (“EITF”) reached a consensus on issue No. 08-7,

Accounting for Defensive Intangible Assets

. This consensus requires that the defensive asset be recorded

at its fair value on the opening balance sheet and amortized over a reasonable life that approximates its

diminishing value. It also states that an indefinite useful life for these defensive assets would be rare. The

consensus is effective for intangible assets acquired on or after the first annual reporting period beginning

after December 15, 2008, which coincides with the adoption of SFAS No. 141(R). The Company expects

EITF No. 08-7 will have an impact on its consolidated financial statements when effective, which will

depend on the nature, terms and size of the acquisitions consummated after the effective date.

In May 2008, the FASB issued Statement No. 162,

The Hierarchy of Generally Accepted Accounting

Principles

, which identifies the sources of accounting principles and the framework for selecting the

principles used in the preparation of financial statements that are presented in conformity with generally

accepted accounting principles (“GAAP”) in the United States. The statement became effective

November 15, 2008 and allowed for transition provisions if necessary. The adoption did not have a material

effect on the financial statements.

In March 2008, the FASB issued Statement No. 161,

Disclosures about Derivative Instruments and Hedging

Activities - an amendment of FASB Statement No. 133,

which amends the disclosure requirements to

provide more “enhanced” disclosures about (i) how and why derivatives are used by the Company, (ii) how