Kraft 2002 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2002 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70

|

|

60

kraft foods inc. notes to consolidated financial statements

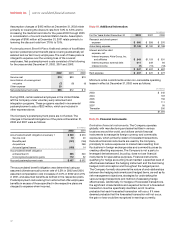

Assumption changes of $193 million at December 31, 2002 relate

primarily to lowering the discount rate from 7.0% to 6.5% and to

increasing the medical trend rate for the years 2003 through 2005

in consideration of current medical inflation trends. Assumption

changes of $180 million at December 31, 2001 relate primarily to

lowering the discount rate from 7.75% to 7.0%.

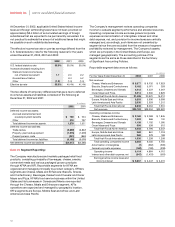

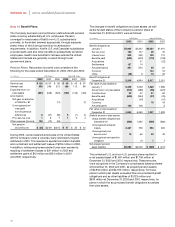

Postemployment Benefit Plans: Kraft and certain of its affiliates

sponsor postemployment benefit plans covering substantially all

salaried and certain hourly employees. The cost of these plans is

charged to expense over the working lives of the covered

employees. Net postemployment costs consisted of the following

for the years ended December 31, 2002, 2001 and 2000:

(in millions)

2002 2001 2000

Service cost $19 $20 $13

Amortization of unrecognized

net gains (7) (8) (4)

Other expense 23

Net postemployment costs $35 $12 $ 9

During 2002, certain salaried employees in the United States

left the Company under voluntary early retirement and

integration programs. These programs resulted in incremental

postemployment costs of $23 million, which are included in

other expense above.

The Company’s postemployment plans are not funded. The

changes in the benefit obligations of the plans at December 31,

2002 and 2001 were as follows:

(in millions)

2002 2001

Accumulated benefit obligation at January 1 $ 520 $ 373

Service cost 19 20

Benefits paid (141) (156)

Acquisitions 269

Actuarial (gains) losses (103) 14

Accumulated benefit obligation

at December 31 295 520

Unrecognized experience gains 112 52

Accrued postemployment costs $ 407 $ 572

The accumulated benefit obligation was determined using an

assumed ultimate annual turnover rate of 0.3% in 2002 and 2001,

assumed compensation cost increases of 4.0% in 2002 and 4.5%

in 2001, and assumed benefits as defined in the respective plans.

Postemployment costs arising from actions that offer employees

benefits in excess of those specified in the respective plans are

charged to expense when incurred.

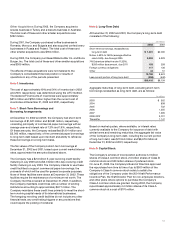

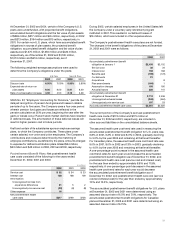

Note 15. Additional Information:

(in millions)

For the Years Ended December 31, 2002 2001 2000

Research and development

expense $ 360 $ 358 $ 270

Advertising expense $1,145 $1,190 $1,198

Interest and other debt

expense, net:

Interest expense, Altria Group, Inc.

and affiliates $ 243 $1,103 $ 531

Interest expense, external debt 611 349 84

Interest income (7) (15) (18)

$ 847 $1,437 $ 597

Rent expense $ 437 $ 372 $ 277

Minimum rental commitments under non-cancelable operating

leases in effect at December 31, 2002 were as follows:

(in millions)

2003 $ 245

2004 197

2005 156

2006 111

2007 95

Thereafter 200

$1,004

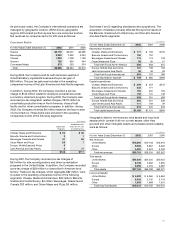

Note 16. Financial Instruments:

Derivative financial instruments: The Company operates

globally, with manufacturing and sales facilities in various

locations around the world, and utilizes certain financial

instruments to manage its foreign currency and commodity

exposures, which primarily relate to forecasted transactions.

Derivative financial instruments are used by the Company,

principally to reduce exposures to market risks resulting from

fluctuations in foreign exchange rates and commodity prices by

creating offsetting exposures. The Company is not a party to

leveraged derivatives and, by policy, does not use financial

instruments for speculative purposes. Financial instruments

qualifying for hedge accounting must maintain a specified level of

effectiveness between the hedging instrument and the item being

hedged, both at inception and throughout the hedged period.

The Company formally documents the nature of and relationships

between the hedging instruments and hedged items, as well as its

risk-management objectives, strategies for undertaking the

various hedge transactions and method of assessing hedge

effectiveness. Additionally, for hedges of forecasted transactions,

the significant characteristics and expected terms of a forecasted

transaction must be specifically identified, and it must be

probable that each forecasted transaction will occur. If it were

deemed probable that the forecasted transaction will not occur,

the gain or loss would be recognized in earnings currently.