Kraft 2002 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2002 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

|

|

50

kraft foods inc. notes to consolidated financial statements

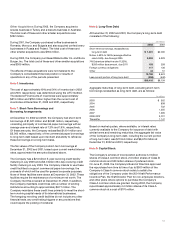

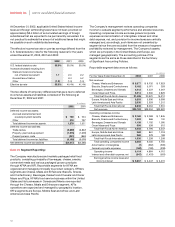

Income taxes: The Company accounts for income taxes in

accordance with SFAS No. 109, “Accounting for Income Taxes.”

The accounts of the Company are included in the consolidated

federal income tax return of Altria Group, Inc. Income taxes are

generally computed on a separate company basis. To the extent

that foreign tax credits, capital losses and other credits generated

by the Company, which cannot be utilized on a separate company

basis, are utilized in Altria Group, Inc.’s consolidated federal

income tax return, the benefit is recognized in the calculation of

the Company’s provision for income taxes. The Company utilized

tax benefits that it would otherwise not have been able to use of

$193 million, $185 million and $139 million for the years ended

December 31, 2002, 2001 and 2000, respectively. The Company

makes payments to, or is reimbursed by, Altria Group, Inc., for the

tax effects resulting from its inclusion in Altria Group, Inc.’s

consolidated federal income tax return.

Inventories: Inventories are stated at the lower of cost or market.

The last-in, first-out (“LIFO”) method is used to cost substantially

all domestic inventories. The cost of other inventories is

principally determined by the average cost method.

Marketing costs: The Company promotes its products with

significant marketing activities, including advertising, consumer

incentives and trade promotions. Advertising costs are expensed

as incurred. Consumer incentive and trade promotion activities

are recorded as a reduction of revenues based on amounts

estimated as being due to customers and consumers at the

end of a period, based principally on historical utilization and

redemption rates.

Revenue recognition: The Company recognizes revenues,

net of sales incentives and including shipping and handling

charges billed to customers, upon shipment of goods when title

and risk of loss pass to customers. Shipping and handling costs

are classified as part of cost of sales.

Effective January 1, 2002, the Company adopted the Emerging

Issues Task Force (“EITF”) Issue No. 00-14, “Accounting for

Certain Sales Incentives” and EITF Issue No. 00-25, “Vendor

Income Statement Characterization of Consideration Paid to a

Reseller of the Vendor’s Products.” Prior period consolidated

statements of earnings have been reclassified to reflect the

adoption. The adoption of these EITF Issues resulted in a

reduction of revenues of approximately $4.6 billion and

$3.6 billion in 2001 and 2000, respectively. In addition, the

adoption reduced marketing, administration and research costs

by $4.7 billion and $3.7 billion in 2001 and 2000, respectively,

while cost of sales increased by an insignificant amount. The

adoption of these EITF Issues had no impact on operating

income, net earnings or basic and diluted EPS.

Software costs: The Company capitalizes certain computer

software and software development costs incurred in connection

with developing or obtaining computer software for internal use.

Capitalized software costs are amortized on a straight-line basis

over the estimated useful lives of the software, which do not

exceed five years.

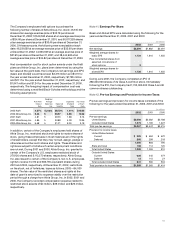

Stock-based compensation: The Company accounts for

employee stock compensation plans in accordance with the

intrinsic value-based method permitted by SFAS No. 123,

“Accounting for Stock-Based Compensation,” which did not

result in compensation cost for stock options.

At December 31, 2002, the Company had stock-based employee

compensation plans, which are described more fully in

Note 10. Stock Plans. The Company applies the recognition and

measurement principles of Accounting Principles Board Opinion

No. 25, “Accounting for Stock Issued to Employees,” and related

Interpretations in accounting for those plans. No compensation

expense for employee stock options is reflected in net earnings

as all options granted under those plans had an exercise price

equal to the market value of the common stock on the date of the

grant. Net earnings, as reported, includes compensation expense

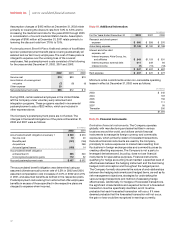

related to restricted stock. The following table illustrates the effect

on net earnings and EPS if the Company had applied the fair

value recognition provisions of SFAS No. 123 to stock-based

employee compensation for the years ended December 31, 2002,

2001 and 2000:

(in millions, except per share data)

2002 2001 2000

Net earnings, as reported $3,394 $1,882 $2,001

Deduct:

Total stock-based employee

compensation expense determined

under fair value method for all

stock option awards, net of related

tax effects 78 97 54

Pro forma net earnings $3,316 $1,785 $1,947

Earnings per share:

Basic—as reported $1.96 $ 1.17 $ 1.38

Basic—pro forma $1.91 $ 1.11 $ 1.34

Diluted—as reported $1.96 $ 1.17 $ 1.38

Diluted—pro forma $1.91 $ 1.11 $ 1.34

New accounting pronouncements: In July 2002, the FASB

issued SFAS No. 146, “Accounting for Costs Associated with Exit

or Disposal Activities.” SFAS No. 146 requires companies to

recognize costs associated with exit or disposal activities when

they are incurred rather than at the date of a commitment to an

exit or disposal plan. Costs covered by SFAS No. 146 include

lease termination costs and certain employee severance costs

that are associated with a restructuring, discontinued operation,

plant closing or other exit or disposal activity. This statement is

effective for exit or disposal activities that are initiated after

December 31, 2002. Accordingly, the Company will apply the

provisions of SFAS No. 146 prospectively to exit or disposal

activities initiated after December 31, 2002.

In November 2002, the EITF issued EITF Issue No. 00-21,

“Revenue Arrangements with Multiple Deliverables,” which

addresses certain aspects of the accounting by a vendor for

arrangements under which it will perform multiple revenue-

generating activities. Specifically, EITF Issue No. 00-21 addresses

how to determine whether an arrangement involving multiple