Kraft 2002 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2002 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

|

|

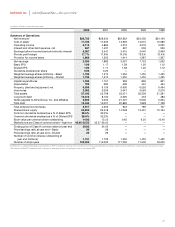

As discussed in Notes 3, 7 and 8 to the consolidated financial

statements, the Company’s total debt of $14.4 billion at December

31, 2002, which includes borrowings from Altria Group, Inc. and

affiliates, is due to be repaid as follows: in 2003, $4.3 billion; in

2004-2005, $1.6 billion; in 2006-2007, $2.6 billion; and thereafter,

$5.9 billion. Debt obligations due to be repaid in 2003 will be

satisfied with a combination of short-term borrowings, long-term

borrowings and operating cash flows. The Company’s debt-to-

equity ratio was 0.56 at December 31, 2002 and 0.68 at

December 31, 2001.

Credit Ratings: The Company’s credit ratings by Moody’s at

December 31, 2002 were “P-1” in the commercial paper market

and “A2” for long-term debt obligations. The Company’s credit

ratings by Standard & Poor’s at December 31, 2002 were “A-1”

in the commercial paper market and “A-” for long-term debt

obligations. The Company’s credit ratings by Fitch Rating

Services at December 31, 2002 were “F-1” in the commercial

paper market and “A” for long-term debt obligations. Changes

in the Company’s credit ratings, although none are currently

anticipated, could result in corresponding changes in the

Company’s borrowing costs. However, none of the Company’s

debt agreements require accelerated repayment in the event of

a decrease in credit ratings.

Credit Lines: The Company and its subsidiaries maintain

credit lines with a number of lending institutions, amounting to

$5.6 billion at December 31, 2002. Approximately $5.4 billion of

these lines were undrawn at December 31, 2002. Certain of these

credit lines were used to support commercial paper borrowings

of $1.4 billion at December 31, 2002, the proceeds of which were

used for general corporate purposes. Approximately $600 million

of these credit lines are available to meet the short-term working

capital needs of the Company’s international businesses. At

December 31, 2002, the Company’s credit lines also include a

$2.0 billion, five-year revolving credit facility expiring in July 2006

and a $3.0 billion 364-day revolving credit facility expiring in

July 2003. These credit facilities require the maintenance of a

minimum net worth, as defined in the credit facility, of $18.2

billion, which the Company met at December 31, 2002. The

Company does not currently anticipate any difficulty in continuing

to meet this covenant requirement. The foregoing revolving

credit facilities do not include any other financial tests, any

credit rating triggers or any provisions that could require the

posting of collateral. The five-year revolving credit facility

enables the Company to reclassify short-term debt on a long-

term basis. At December 31, 2002, $1.4 billion of commercial

paper borrowings that the Company intends to refinance were

reclassified as long-term debt. The Company expects to continue

to refinance long-term and short-term debt from time to time.

The nature and amount of the Company’s long-term and short-

term debt and the proportionate amount of each can be

expected to vary as a result of future business requirements,

market conditions and other factors.

Guarantees and Commitments: As discussed in Note 17 to the

consolidated financial statements, the Company had third-party

guarantees, which are primarily derived from acquisition and

divestiture activities, of $36 million at December 31, 2002.

Substantially all of these guarantees expire through 2012, with

$12 million expiring in 2003. The Company is required to perform

under these guarantees in the event that a third-party fails to

make contractual payments or achieve performance measures.

The Company has recorded a liability of $21 million at December

31, 2002 relating to these guarantees. In addition, at December 31,

2002, the Company was contingently liable for $58 million of

guarantees related to its own performance. These include surety

bonds related to dairy commodity purchases and guarantees

related to letters of credit. Guarantees do not have, and are not

expected to have, a significant impact on the Company’s liquidity.

The Company’s consolidated rent expense for 2002 was

$437 million. Accordingly, the Company does not consider its

lease commitments to be a significant determinant of the

Company’s liquidity.

The Company believes that its cash from operations, existing

credit facilities and access to global capital markets will provide

sufficient liquidity to meet its working capital needs, planned

capital expenditures and payment of its anticipated quarterly

dividends.

Equity and Dividends

Dividends paid in 2002 and 2001 were $936 million and

$225 million, respectively, reflecting the payment of four quarterly

dividends during 2002, compared with one during 2001, as well

as a higher dividend rate in 2002. During the third quarter of 2002,

the Company’s Board of Directors approved a 15.4% increase in

the quarterly dividend rate to $0.15 per share on its Class A and

Class B common stock. As a result, the present annualized

dividend rate is $0.60 per common share. The declaration of

dividends is subject to the discretion of the Company’s Board

of Directors and will depend on various factors, including the

Company’s net earnings, financial condition, cash requirements,

future prospects and other factors deemed relevant by the

Company’s Board of Directors.

On June 21, 2002, the Company’s Board of Directors approved

the repurchase from time to time of up to $500 million of the

Company’s Class A common stock solely to satisfy the

obligations of the Company to provide shares under its 2001

Performance Incentive Plan, 2001 Director Plan for non-employee

directors, and other plans where options to purchase the

Company’s Class A common stock are granted to employees

of the Company. During 2002, the Company repurchased

approximately 4.4 million shares of its Class A common stock at

a cost of $170 million.

Concurrently with the IPO, certain employees of Altria Group, Inc.

and its subsidiaries (other than the Company) received a one-time

grant of options to purchase shares of the Company’s Class A

common stock held by Altria Group, Inc. at the IPO price of

$31.00 per share. In order to completely satisfy this obligation and

maintain its current percentage ownership of the Company, Altria

Group, Inc. purchased 1.6 million shares of the Company’s Class

A common stock in open market transactions during 2002.

39