Kraft 2002 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2002 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

|

|

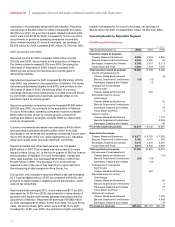

This VAR computation is a risk analysis tool designed to

statistically estimate the maximum probable daily loss from

adverse movements in interest rates, foreign currency rates

and commodity prices under normal market conditions. The

computation does not purport to represent actual losses in fair

value or earnings to be incurred by the Company, nor does it

consider the effect of favorable changes in market rates. The

Company cannot predict actual future movements in such market

rates and does not present these VAR results to be indicative of

future movements in such market rates or to be representative of

any actual impact that future changes in market rates may have

on its future results of operations or financial position.

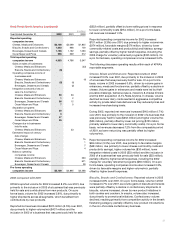

New Accounting Standards

As previously discussed, on January 1, 2002, the Company

adopted SFAS No. 141, “Business Combinations,” SFAS No. 142,

“Goodwill and Other Intangible Assets,” Emerging Issues Task

Force (“EITF”) Issue No. 00-14, “Accounting for Certain Sales

Incentives” and EITF Issue No. 00-25, “Vendor Income Statement

Characterization of Consideration Paid to a Reseller of the

Vendor’s Products.”

Effective January 1, 2002, the Company adopted SFAS No. 144,

“Accounting for the Impairment or Disposal of Long-Lived

Assets,” which replaces SFAS No. 121, “Accounting for the

Impairment of Long-Lived Assets and Long-Lived Assets to Be

Disposed Of.” SFAS No. 144 provides updated guidance

concerning the recognition and measurement of an impairment

loss for certain types of long-lived assets, expands the scope

of a discontinued operation to include a component of an

entity and eliminates the exemption to consolidation when

control over a subsidiary is likely to be temporary. The adoption

of this new standard did not have a material impact on the

Company’s consolidated financial position, results of

operations or cash flows.

In July 2002, the Financial Accounting Standards Board (“FASB”)

issued SFAS No. 146, “Accounting for Costs Associated with Exit

or Disposal Activities.” SFAS No. 146 requires companies to

recognize costs associated with exit or disposal activities when

they are incurred rather than at the date of a commitment to an

exit or disposal plan. Costs covered by SFAS No. 146 include

lease termination costs and certain employee severance costs

that are associated with a restructuring, discontinued operation,

plant closing or other exit or disposal activity. This statement is

effective for exit or disposal activities that are initiated after

December 31, 2002. Accordingly, the Company will apply the

provisions of SFAS No. 146 prospectively to exit or disposal

activities initiated after December 31, 2002.

In November 2002, the FASB issued Interpretation No. 45,

“Guarantor’s Accounting and Disclosure Requirements for

Guarantees, Including Indirect Guarantees of Indebtedness

of Others.” Interpretation No. 45 requires the disclosure of

certain guarantees existing at December 31, 2002. In addition,

Interpretation No. 45 requires the recognition of a liability for the

fair value of the obligation of qualifying guarantee activities that

are initiated or modified after December 31, 2002. Accordingly, the

Company will apply the recognition provisions of Interpretation

No. 45 prospectively to guarantee activities initiated after

December 31, 2002.

In November 2002, the EITF issued EITF Issue No. 00-21,

“Revenue Arrangements with Multiple Deliverables,” which

addresses certain aspects of the accounting by a vendor for

arrangements under which it will perform multiple revenue-

generating activities. Specifically, EITF Issue No. 00-21 addresses

how to determine whether an arrangement involving multiple

deliverables contains more than one unit of accounting. EITF

Issue No. 00-21 is effective for the Company for revenue

arrangements entered into beginning July 1, 2003. The Company

does not expect the adoption of EITF Issue No. 00-21 to have a

material impact on its 2003 consolidated financial statements.

In January 2003, the FASB issued Interpretation No. 46,

“Consolidation of Variable Interest Entities.” Interpretation No. 46

requires that the assets, liabilities and results of the activity of

variable interest entities be consolidated into the financial

statements of the company that has the controlling financial

interest. Interpretation No. 46 also provides the framework for

determining whether a variable interest entity should be

consolidated based on voting interests or significant financial

support provided to it. Interpretation No. 46 will be effective for

the Company on February 1, 2003 for variable interest entities

created after January 31, 2003, and on July 1, 2003 for variable

interest entities created prior to February 1, 2003. The Company

does not expect the adoption of Interpretation No. 46 to have a

material impact on its 2003 consolidated financial statements.

Contingencies

See Note 17 to the consolidated financial statements for a

discussion of contingencies.

41