Kraft 2002 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2002 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

|

|

kraft foods inc. management’s discussion and analysis of financial condition and results of operations

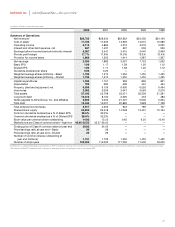

During 2002, reported net revenues increased $111 million (2.2%)

over 2001, due to higher volume/mix ($59 million) and higher net

pricing ($52 million). On a pro forma basis, net revenues also

increased 2.2%.

Reported operating companies income for 2002 increased

$127 million (13.1%) over 2001, due primarily to favorable margins

($96 million, due primarily to higher net pricing and lower

commodity costs for nuts), Nabisco synergy savings and higher

volume/mix. On a pro forma basis, operating companies income

increased 12.4%.

Beverages, Desserts and Cereals: Reported and pro forma

volume in 2002 increased 8.4% over 2001, due primarily to growth

in ready-to-drink beverages. In coffee, volume increased, driven

by merchandising programs and packaging innovation. In the

desserts business, volume increases were led by dry packaged

desserts and frozen toppings, which benefited from holiday

programs, and in ready-to-eat desserts, aided by new products.

During 2002, reported net revenues increased $175 million (4.1%)

over 2001, due primarily to higher volume/mix ($245 million),

partially offset by lower net pricing ($58 million). On a pro forma

basis, net revenues increased 4.4%.

Reported operating companies income for 2002 decreased

$56 million (4.7%) from 2001, primarily reflecting the 2002

charge for voluntary retirement programs ($47 million), higher

integration related costs in 2002 ($44 million), higher marketing,

administration and research costs ($36 million, including higher

benefit costs) and lower margins ($18 million), partially offset by

higher volume/mix ($98 million) and productivity savings. On a

pro forma basis, operating companies income increased 3.1%,

resulting from volume growth and productivity savings, partially

offset by higher marketing, administration and research costs.

Oscar Mayer and Pizza: Reported and pro forma volume in 2002

increased 2.3% over 2001, due to volume gains in processed

meats and pizza. The increase in processed meats was driven by

gains in hot dogs, bacon and soy-based meat alternatives, aided

by new product introductions. The pizza business also benefited

from new products.

During 2002, reported and pro forma net revenues increased

$84 million (2.9%) over 2001, due to higher volume/mix

($97 million), partially offset by lower net pricing ($13 million).

Reported operating companies income for 2002 increased

$17 million (3.2%) over 2001, primarily reflecting favorable

costs ($50 million, due primarily to lower meat and cheese

commodity costs and productivity savings) and higher

volume/mix ($30 million), partially offset by the 2002 charge for

voluntary retirement programs ($25 million), higher marketing,

administration and research costs ($24 million, including higher

benefit costs) and higher manufacturing costs. On a pro forma

basis, operating companies income increased 8.1%.

2001 compared with 2000

KFNA’s reported volume for 2001 increased 31.7% over 2000,

due primarily to the acquisition of Nabisco. On a pro forma basis,

volume for 2001 increased 1.7%, or 2.9% excluding the 53rd week

of shipments in 2000. The 2.9% increase was due primarily to

higher shipments across all segments and reflects contributions

from new products.

Reported net revenues increased $5.7 billion (37.0%) over 2000,

due primarily to the acquisition of Nabisco ($5.7 billion) and the

shift in CDC revenues ($59 million), partially offset by unfavorable

currency movements ($62 million). On a pro forma basis, net

revenues increased 0.4%, due primarily to higher net revenues

from the Biscuits, Snacks and Confectionery segment and the

Oscar Mayer and Pizza segment, partially offset by the impact of

the 53rd week in 2000.

Reported operating companies income for 2001 increased

$1,249 million (35.2%) over 2000, due primarily to the acquisition

of Nabisco ($1.2 billion), lower marketing, administration and

research costs ($274 million) and the shift in CDC income

($27 million), partially offset by lower margins ($136 million, driven

primarily by higher dairy commodity-related costs) and the loss

on the sale of a North American food factory and integration

costs ($82 million). On a pro forma basis, operating companies

income increased 9.6%.

The following discusses operating results within each of KFNA’s

reportable segments.

Cheese, Meals and Enhancers: Reported volume in 2001

increased 8.3% over 2000, due primarily to the acquisition of

Nabisco. On a pro forma basis, volume in 2001 decreased 1.1%,

due primarily to the 53rd week of shipments in 2000. Excluding

the 53rd week of shipments in 2000, volume increased 0.2%, as

volume gains in meals, enhancers and Canada were partially

offset by declines in cheese and food service. Meals recorded

volume gains, reflecting higher shipments of macaroni & cheese

dinners. Enhancers also recorded volume gains, reflecting higher

shipments of spoonable and pourable dressings. In Canada,

volume grew on higher shipments of branded products. In

cheese, shipments decreased, due primarily to the Company’s

decision to exit the lower-margin, non-branded cheese business.

Volume also declined in process cheese loaves and cream

cheese, as retailers continued to reduce trade inventory levels,

partially offset by higher volume in grated and natural cheese. In

U.S. food service, shipments declined due to weakness in the

economy and the Company’s exit from lower-margin businesses.

During 2001, reported net revenues increased $809 million

(10.2%) over 2000, due primarily to the acquisition of Nabisco

($791 million), higher net pricing ($122 million, primarily related

to higher dairy commodity costs) and the shift in CDC revenues

($29 million), partially offset by lower volume/mix ($65 million) and

unfavorable currency movements ($62 million). On a pro forma

basis, net revenues increased slightly from the comparable period

of 2000, as higher pricing in cheese and food service were

partially offset by unfavorable currency and lower volume/mix.

34