Kodak 2000 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2000 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

19

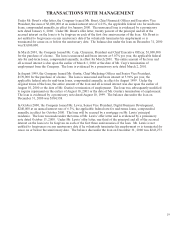

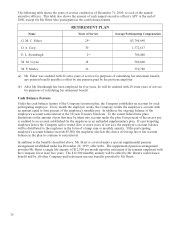

TRANSACTIONS WITH MANAGEMENT

Under Mr. Brust’s offer letter, the Company loaned Mr. Brust, Chief Financial Officer and Executive Vice

President, the sum of $3,000,000 at an annual interest rate of 6.21%, the applicable federal rate for mid-term

loans, compounded annually, in effect for January 2000. The unsecured loan is evidenced by a promissory

note dated January 6, 2000. Under Mr. Brust’s offer letter, twenty percent of the principal and all of the

accrued interest on the loan is to be forgiven on each of the first five anniversaries of the loan. Mr. Brust is

not entitled to forgiveness on any anniversary date if he voluntarily terminates his employment or is

terminated for cause on or before the anniversary date. The balance due under the loan on December 31, 2000

was $3,000,000.

In March 2001, the Company loaned Mr. Carp, Chairman, President and Chief Executive Officer, $1,000,000

for the purchase of a home. The loan is unsecured and bears interest at 5.07% per year, the applicable federal

rate for mid-term loans, compounded annually, in effect for March 2001. The entire amount of the loan and

all accrued interest is due upon the earlier of March 1, 2006 or the date of Mr. Carp’s termination of

employment from the Company. The loan is evidenced by a promissory note dated March 2, 2001.

In August 1999, the Company loaned Mr. Gustin, Chief Marketing Officer and Senior Vice President,

$170,000 for the purchase of a home. The loan is unsecured and bears interest at 5.96% per year, the

applicable federal rate for mid-term loans, compounded annually, in effect for August 1999. Under the

original terms of the loan, the entire amount of the loan and all accrued interest was due upon the earlier of

August 10, 2000 or the date of Mr. Gustin’s termination of employment. The loan was subsequently modified

to require repayment on the earlier of August 10, 2001 or the date of Mr. Gustin’s termination of employment.

The loan is evidenced by a promissory note dated August 10, 1999. The balance due under the loan on

December 31, 2000 was $184,338.

In October 2000, the Company loaned Mr. Lewis, Senior Vice President, Digital Business Development,

$240,000 at an annual interest rate of 6.3%, the applicable federal rate for mid-terms loans, compounded

annually, in effect for October 2000. The loan will be secured by a mortgage on Mr. Lewis’ principal

residence. The loan was made under the terms of Mr. Lewis’ offer letter and is evidenced by a promissory

note dated October 13, 2000. Under Mr. Lewis’ offer letter, one third of the principal and all of the accrued

interest on the loan is to be forgiven on each of the first three anniversaries of the loan. Mr. Lewis is not

entitled to forgiveness on any anniversary date if he voluntarily terminates his employment or is terminated for

cause on or before the anniversary date. The balance due under the loan on December 31, 2000 was $243,273.