Kodak 2000 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2000 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

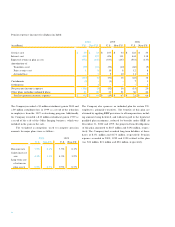

1 9 9 8 On March 12, 1998, the Company acquired 51% of

P i c t u re Vision Inc.’s stock for approximately $50 million. The

acquisition was accounted for as a purchase and, accord i n g l y,

the operating results of the business have been included in the

accompanying consolidated financial statements from the date

of acquisition.

In Febru a ry 1998, the Company contributed $308 million

to Kodak (China) Company Limited (KCCL), a newly form e d

company operating in China, in exchange for 80% of the out-

standing shares of the company. On March 25 and September 1,

1998, the new company acquired certain manufacturing assets

of Shantou Era Photo Material Industry Corporation, a Chinese

domestic photographic enterprise, for $159 million in cash and

$22 million in debt payable in 2003. On March 26, 1998, KCCL

a c q u i red certain manufacturing assets of Xiamen Fuda Photo-

graphic Materials Company, Ltd., another C hinese domestic

photographic enterprise, for $149 million.

In Febru a ry 1998, the Company contributed $32 million to

Kodak (Wuxi) Company Limited (KWCL), a newly formed com-

pany operating in China, in exchange for 70% of the outstanding

s h a res of the business. On April 2, 1998, KWCL acquired part

of the manufacturing assets of Wuxi Aermei Film and Chemical

Corporation, a Chinese domestic photographic enterprise, for

$11 million in cash and $21 million in debt payable in 1999.

The acquisitions by KCCL and KWCL were accounted for

as purchases and, accord i n g l y, the operating results of the

a c q u i red companies have been included in the accompanying

consolidated financial statements from the dates of acquisition.

Substantial portions of the purchase prices were allocated to

goodwill, which is being amortized over a ten-year period.

On November 30, 1998, Kodak acquired certain assets and

assumed certain liabilities of Imation’s medical imaging business,

including all of the outstanding shares of Imation’s Cemax-Icon

s u b s i d i a ry, for approximately $530 million. At the date of acquisi-

tion, the business acquired by Kodak generated appro x i m a t e l y

$500 million in annual revenues. The transaction was accounted

for by the purchase method and, accord i n g l y, the operating

results of the business have been included in the accompanying

consolidated financial statements from the date of acquisition. A

substantial portion of the purchase price was allocated to tangi-

ble assets and goodwill, which is being amortized over a ten-year

period. See discussion re g a rding in-process R&D charges below.

P u rchased In-process Research and Development Charg e s I n

connection with the 2000 Picture Vision Inc. acquisition and the

1998 purchase of Imation’s medical imaging busines s, the

Company allocated $10 million and $42 million of the purc h a s e

price, re s p e c t i v e l y, to in-process R&D.

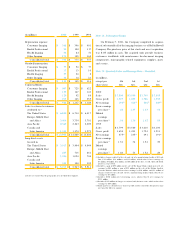

The C ompany us ed independent profess ional appraisal

consultants to assess and allocate values to the in-process R&D.

At the dates of the respective business combinations, the devel-

opment of these projects had not yet reached technological

feasibility and the R&D in pro g res s had no alternative uses.

A c c o rd i n g l y, these costs were expensed as of the re s p e c t i v e

acquisition dates.

The valuations were determined by the Company using the

income approach. This methodology involves estimating the con-

tribution of the purchased in-process technology to developing

c o m m e rcially viable products and es timating the resulting cash

flows from the expected product sales of such products. The

resulting cash flows were discounted to their present value using

a p p ropriate risk adjusted rates. Cash flows attributable to devel-

opment eff o rts, including the completion of developments under-

w a y, and future versions of the product that have not yet been

u n d e rtaken, were excluded in the valuation of in-process R&D.

A contributory asset charge was applied for the use of working

capital, fixed assets, developed technology and other intangibles.

There were no material anticipated changes from historical pricing,

m a rgins , and expense tre n d s .

The Company believes that the assumptions used in the fore-

casts were reasonable at the time of the respective business

combinations. No assurance can be given, however, that the

underlying assumptions used to estimate expected project sales,

development costs or pro f i t a b i l i t y, or the events associated with

such projects, will transpire as estimated. For thes e re a s o n s ,

actual results may vary from the projected re s u l t s .