Dollar General 2013 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2013 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

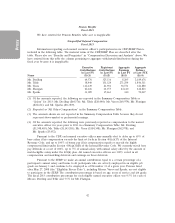

If the named executive officer is involuntarily terminated without cause or resigns for good

reason following the change in control, he will receive the same severance payments and benefits as

described above under ‘‘Voluntary Termination with Good Reason or After Failure to Renew the

Employment Agreement.’’ However, the named executive officer will have 1 year from the termination

date in which to exercise vested options that were granted after 2011 if he resigns or is involuntarily

terminated within 2 years of the change in control under any scenario other than retirement or

involuntary termination with cause (in which cases, he will have 5 years from the retirement date to

exercise vested options and will forfeit any vested but unexercised options held at the time of the

termination with cause).

Prior to March 2014, other than with respect to Mr. Sparks, if any payments or benefits in

connection with a change in control (as defined in Section 280G of the Internal Revenue Code) would

be subject to the ‘‘golden parachute’’ excise tax under federal income tax rules (the ‘‘excise tax’’), we

would pay an additional amount to the named executive officer to cover the excise tax and any other

excise and income taxes resulting from this payment. However, other than with respect to Mr. Dreiling,

if after receiving this payment the named executive officer’s after-tax benefit would not be at least

$50,000 more than it would be without this payment, then this payment would not be made and the

severance and other benefits due to the named executive officer would be reduced so that the excise

tax is not imposed. In Mr. Sparks’ case, his employment agreement provides for capped payments

(taking into consideration all payments and benefits covered by Section 280G of the Internal Revenue

Code) of $1 less than the amount that would trigger the excise tax unless he signs a release and his

after-tax benefit would be at least $50,000 more than it would be without the payments being capped.

In such case, his payments and benefits would not be capped and Mr. Sparks would be responsible for

the payment of the excise tax. We would not pay any additional amount to cover the excise tax. The

above scenarios are included in the table following this narrative since such table assumes the

occurrence of the event as of January 31, 2014.

In March 2014, Messrs. Dreiling, Tehle, Vasos and Flanigan entered into amendments to their

employment agreements that eliminated gross-up payments for the excise tax effective immediately.

Other than with respect to Mr. Dreiling, in the event of a change in control as defined in Section 280G

of the Internal Revenue Code), each named executive officer’s employment agreement now provides

for capped payments (taking into consideration all payments and benefits covered by Section 280G of

the Internal Revenue Code) of $1 less than the amount that would trigger the excise tax unless he signs

a release and his after-tax benefit would be at least $50,000 more than it would be without the

payments being capped. In such case, such officer’s payments and benefits would not be capped and

such officer would be responsible for the payment of the excise tax. We would not pay any additional

amount to cover the excise tax. In Mr. Dreiling’s case, his employment agreement now provides for

capped payments (taking into consideration all payments and benefits covered by Section 280G of the

Internal Revenue Code) of $1 less than the amount that would trigger the excise tax unless his after-tax

benefit would be at least $50,000 more than it would be without the payments being capped. In such

case, Mr. Dreiling’s payments and benefits would not be capped and he would be responsible for the

payment of the excise tax. We would not pay any additional amount to cover the excise tax.

For purposes of the CDP/SERP Plan, a change in control generally is deemed to occur (as

more fully described in the plan document):

• if any person (other than Dollar General or any of our employee benefit plans) acquires

35% or more of our voting securities (other than as a result of our issuance of securities in

the ordinary course of business);

• if a majority of our Board members at the beginning of any consecutive 2-year period are

replaced within that period without the approval of at least two-thirds of our Board

members who served as directors at the beginning of the period; or

• upon the consummation of a merger, other business combination or sale of assets of, or

cash tender or exchange offer or contested election with respect to, Dollar General if less

than a majority of our voting securities are held after the transaction in the aggregate by

holders of our securities immediately prior to the transaction.

52

Proxy