Cincinnati Bell 2013 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2013 Cincinnati Bell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

|

|

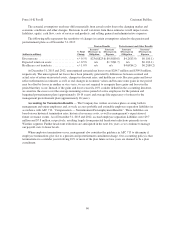

The actuarial assumptions used may differ materially from actual results due to the changing market and

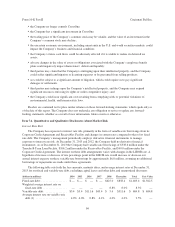

economic conditions and other changes. Revisions to and variations from these estimates would impact assets,

liabilities, equity, cash flow, costs of services and products, and selling, general and administrative expenses.

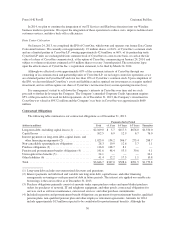

The following table represents the sensitivity of changes in certain assumptions related to the pension and

postretirement plans as of December 31, 2013:

Pension Benefits Postretirement and Other Benefits

(dollars in millions)

% Point

Change

Increase/

(Decrease) in

Obligation

Increase/

(Decrease) in

Expense

Increase/

(Decrease) in

Obligation

Increase/

(Decrease) in

Expense

Discount rate ......................... +/-0.5% $23.6/($23.6) $0.8/($0.8) $4.2/($3.9) $0.1/(0.1)

Expected return on assets ............... +/-0.5% n/a $1.7/($1.7) n/a $0.1/(0.1)

Healthcare cost trend rate ............... +/-1.0% n/a n/a $4.6/($4.2) $0.2/($0.2)

At December 31, 2013 and 2012, unrecognized actuarial net losses were $284.7 million and $399.8 million,

respectively. The unrecognized net losses have been primarily generated by differences between assumed and

actual rates of return on invested assets, changes in discount rates, and healthcare costs. Because gains and losses

reflect refinements in estimates as well as real changes in economic values and because some gains in one period

may be offset by losses in another or vice versa, we are not required to recognize these gains and losses in the

period that they occur. Instead, if the gains and losses exceed a 10% corridor defined in the accounting literature,

we amortize the excess over the average remaining service period of active employees for the pension and

bargained postretirement plans (approximately 10-14 years) and average life expectancy of retirees for the

management postretirement plan (approximately 16 years).

Accounting for Termination Benefits — The Company has written severance plans covering both its

management and union employees and, as such, accrues probable and estimable employee separation liabilities in

accordance with ASC 712, “Compensation — Nonretirement Postemployment Benefits”. These liabilities are

based on our historical termination rates, historical severance costs, as well as management’s expectation of

future severance events. As of December 31, 2013 and 2012, accrued employee separation liabilities were $9.7

million and $7.8 million, respectively, resulting largely from projected headcount reductions primarily in our

Wireline segment. Further headcount reductions are anticipated in the next few years as we continue to manage

our payroll costs to lower levels.

When employee terminations occur, management also considers the guidance in ASC 715 to determine if

employee terminations give rise to a pension and postretirement curtailment charge. Our accounting policy is that

terminations in a calendar year involving 10% or more of the plan future service years are deemed to be a plan

curtailment.

60

Form 10-K Part II Cincinnati Bell Inc.