Cincinnati Bell 2013 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2013 Cincinnati Bell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

|

|

Form 10-K Part II Cincinnati Bell Inc.

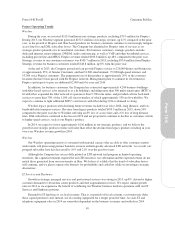

Future Operating Trends

Wireline

During the year, we invested $113.0 million in our strategic products, including $79.5 million for Fioptics.

During 2013, our Wireline segment generated $252.5 million of strategic revenue, up 22% compared to the prior

year, as the growth of Fioptics and fiber-based products for business customers continues to increasingly mitigate

access line loss and DSL subscriber losses. The Company has identified its Fioptics suite of services as its

strategic product primarily for its residential customers. For business customers, strategic products include:

dedicated internet, metro-ethernet, DWDM, audio conferencing, as well as VoIP and other broadband services,

including private line and MPLS. Fioptics revenue totaled $100.8 million, up 48% compared to the prior year.

Strategic revenue to our consumer customers was $103.7 million in 2013, including $93.6 million from Fioptics.

Strategic revenue for business customers totaled $148.8 million, up 8% from the prior year.

At the end of 2013, the Company passed and can provide Fioptics service to 276,000 homes and businesses,

or approximately 35% of Greater Cincinnati, and had 74,200 entertainment, 79,900 high-speed internet, and

53,300 voice Fioptics customers. The penetration rate of this product is approximately 29% of the customer

locations that have been passed with the Fioptics network. Management plans to continue its investment in

Fioptics and expects to pass an additional 62,000 units by year end 2014.

In addition, for business customers, the Company has connected approximately 4,200 business buildings

with fiber-based services (also referred to as a lit building), including more than 500 multi-tenant units (MTU’s)

lit with fiber, expanded the fiber network to span more than 5,700 route miles, and provided cell site back-haul

services to more than 70% of the 1,100 cell sites in-market, of which approximately 550 are lit with fiber. We

expect to continue to light additional MTU’s and towers with fiber during 2014 as demand is strong.

Wireline legacy products with declining future revenues include local voice, DSL, long distance, and low-

bandwidth data transport services. Revenue from legacy products totaled $459.5 million in 2013, down 10%

compared to the prior year due to Wireline suffering an 8% loss of access lines and a 6% loss of long distance

lines. DSL subscribers continued to decrease in 2013 and are projected to continue to decline as customers switch

to higher speed services, such as our Fioptics product.

In 2014, we expect to invest approximately $116 million in our strategic products, and we believe the

growth in our strategic product revenue will more than offset the decline from legacy products resulting in year-

over-year Wireline revenue growth in 2014.

Wireless

Our Wireless operating territory is saturated with national carriers who are able to offer customers nation-

wide family talk plans using premier handsets on more technologically advanced LTE networks. As a result, our

postpaid subscriber base has decreased by 19% and 21% over the past two years.

Although the Company has successfully piloted an LTE network trial program in limited operating

territories, the capital investment required for an LTE network is too substantial and the expected returns do not

match those generated from our investments in fiber. We believe it is likely that the trend of subscriber losses

will continue, and we plan to operate the business for profitability and cash flow while we investigate strategic

alternatives.

IT Services and Hardware

Growth in strategic managed services and professional services was strong in 2013, up 8%, driven by higher

customer demand for virtual data center products and staff augmentation services. We expect similar growth

rates in 2014 as we experience the benefit of combining our Wireline business markets operations with our IT

Services and Hardware portions.

Demand for IT hardware is cyclical in nature. That is, in periods of fiscal restraint, a customer may defer

these capital purchases and, instead, use its existing equipment for a longer period of time. As such, IT and

telephony equipment sales in 2014 are somewhat dependent on the business economy and outlook in 2014.

49

Form 10-K