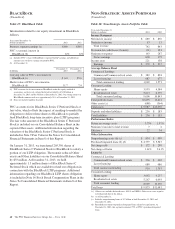

PNC Bank 2013 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2013 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

|

|

As such, the value of goodwill is supported by earnings, which

is driven by transaction volume and, for certain businesses, the

market value of assets under administration or for which

processing services are provided. Lower earnings resulting

from a lack of growth or our inability to deliver cost-effective

services over sustained periods can lead to impairment of

goodwill, which could result in a current period charge to

earnings. At least annually, in the fourth quarter, or more

frequently if events occur or circumstances have changed

significantly from the annual test date, management reviews

the current operating environment and strategic direction of

each reporting unit taking into consideration any events or

changes in circumstances that may have an effect on the unit.

For this review, inputs are generated and used in calculating

the fair value of the reporting unit, which is compared to its

carrying amount (“Step 1” of the goodwill impairment test) as

further discussed below. The fair values of the majority of our

reporting units are determined using a discounted cash flow

valuation model with assumptions based upon market

comparables. Additionally, we may also evaluate certain

financial metrics that are indicative of fair value, including

market quotes, price to earnings ratios and recent acquisitions

involving other financial institutions. A reporting unit is

defined as an operating segment or one level below an

operating segment. If the fair value of the reporting unit

exceeds its carrying amount, the reporting unit is not

considered impaired. However, if the fair value of the

reporting unit is less than its carrying amount, the reporting

unit’s goodwill would be evaluated for impairment. In this

circumstance, the implied fair value of reporting unit goodwill

would be compared to the carrying amount of that goodwill

(“Step 2” of the goodwill impairment test). If the carrying

amount of goodwill exceeds the implied fair value of

goodwill, the difference is recognized as an impairment loss.

The implied fair value of reporting unit goodwill is

determined by assigning the fair value of a reporting unit to its

assets and liabilities (including any unrecognized intangible

assets) with the residual amount equal to the implied fair value

of goodwill as if the reporting unit had been acquired in a

business combination.

A reporting unit’s carrying amount is based upon assigned

economic capital as determined by PNC’s internal

management methodologies. Additionally, in performing Step

1 of our goodwill impairment testing, we utilize three equity

metrics:

• Assigned reporting unit economic capital as

determined by our internal management

methodologies, inclusive of goodwill.

• A 6%, “well capitalized”, Tier 1 common ratio for

the reporting unit under PNC guidelines.

• The capital levels for comparable companies (as

reported in comparable company public financial

statements), adjusted for differences in risk

characteristics between the comparable companies

and the reporting unit.

In determining a reporting unit’s fair value and comparing it

to its carrying value, we generally utilize the highest of these

three amounts (the “targeted equity”) in our discounted cash

flow methodology. Under this methodology, if necessary, we

will infuse capital to achieve the targeted equity amount. As of

October 1, 2013 (annual impairment testing date), unallocated

excess capital (difference between shareholders’ equity minus

total economic capital assigned and increased by the

incremental targeted equity capital infusion) was insignificant.

The results of our annual 2013 impairment test indicated that

the estimated fair values of our reporting units exceeded their

carrying values by at least 10% and are not considered to be at

risk of not passing Step 1. By definition, assumptions utilized

in estimating the fair value of a reporting unit are judgmental

and inherently uncertain, but absent a significant change in

economic conditions of a reporting unit, we would not expect

the fair values of these reporting units to decrease below their

respective carrying values.

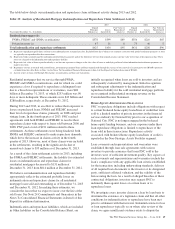

During 2012, our residential mortgage banking business,

similar to other residential mortgage banking businesses,

experienced higher operating costs and increased uncertainties

such as elevated indemnification and repurchase liabilities and

foreclosure related issues. As a result of our annual

impairment test, we determined that the carrying amount of

goodwill relating to the Residential Mortgage Banking

reporting unit was greater than the implied fair value of its

goodwill. We recorded an impairment charge of $45 million

during the fourth quarter of 2012 within Noninterest expense

which reduced the carrying value of goodwill attributed to

Residential Mortgage Banking to zero.

See Note 10 Goodwill and Other Intangible Assets in the

Notes To Consolidated Financial Statements in Item 8 of this

Report for additional information.

L

EASE

R

ESIDUALS

We provide financing for various types of equipment,

including aircraft, energy and power systems, and vehicles

through a variety of lease arrangements. Direct financing

leases are carried at the sum of lease payments and the

estimated residual value of the leased property, less unearned

income. Residual values are subject to judgments as to the

value of the underlying equipment that can be affected by

changes in economic and market conditions and the financial

viability of the residual guarantors. Residual values are

derived from historical remarketing experience, secondary

market contacts, and industry publications. To the extent not

guaranteed or assumed by a third-party, we bear the risk of

ownership of the leased assets. This includes the risk that the

actual value of the leased assets at the end of the lease term

will be less than the estimated residual value, which could

result in an impairment charge and reduce earnings in the

future. Residual values are reviewed for impairment at least

annually.

The PNC Financial Services Group, Inc. – Form 10-K 63