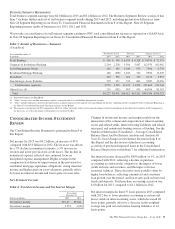

PNC Bank 2013 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2013 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

|

|

expectations that the OCC began communicating to large

banks in 2010, would establish standards governing, among

other things, the roles, responsibilities and organizational

structure of the risk management and internal audit functions

of large national banks, and the role and responsibilities of a

bank’s Board of Directors in overseeing the bank’s risk

governance framework. The standards have not been finalized

and remain subject to modification. However, if the standards

were adopted as proposed, we do not expect that the standards

would have a material effect on PNC.

On February 18, 2014, the Federal Reserve adopted final rules

to implement enhanced prudential standards relating to

liquidity and overall risk management for U.S. bank holding

companies with total consolidated assets of $50 billion or

more, as required under section 165 of Dodd-Frank. The final

rules also implement the provisions of Dodd-Frank that

require the Federal Reserve to impose a maximum debt-to-

equity ratio on a bank holding company if the Financial

Stability Oversight Council determines that, among other

things, the company poses a grave threat to the financial

stability of the United States. For additional information

regarding these final rules, as well as the other enhanced

prudential standards that the Federal Reserve is required to

establish under section 165 of Dodd-Frank, please see the

Supervision and Regulation section of Item 1 Business and

Item 1A Risk Factors of this Report.

On July 31, 2013, the United States District Court for the

District of Columbia granted summary judgment to the

plaintiffs in NACS, et al. v. Board of Governors of the Federal

Reserve System. The decision vacated the debit card

interchange and network processing rules that went into effect

in October 2011 and that were adopted by the Federal Reserve

to implement provisions of Dodd-Frank. The court found

among other things that the debit card interchange fees

permitted under the rules allowed card issuers to recover costs

that were not permitted by the statute. The court has stayed its

decision pending appeal, and the United States Court of

Appeals for the District of Columbia Circuit granted an

expedited appeal. Briefing has been completed and oral

argument was held in January 2014. In light of the appeal we

do not now know the ultimate impact of the District Court’s

ruling, nor the timing of any such impact if such ruling is

affirmed or substantially affirmed on appeal, but if the ruling

were to take effect it could have a materially adverse impact

on our debit card interchange revenues. Debit card interchange

revenue for the year ended December 31, 2013 was

approximately $338 million.

For additional information concerning recent legislative and

regulatory developments, as well as certain governmental,

legislative and regulatory inquiries and investigations that may

affect PNC, please see the Supervision and Regulation section

of Item 1 Business, Item 1A Risk Factors, and Note 23 Legal

Proceedings and Note 24 Commitments and Guarantees in the

Notes To Consolidated Financial Statements in Item 8 of this

Report.

K

EY

F

ACTORS

A

FFECTING

F

INANCIAL

P

ERFORMANCE

Our financial performance is substantially affected by a

number of external factors outside of our control, including

the following:

• General economic conditions, including the

continuity, speed and stamina of the current U.S.

economic expansion in general and on our customers

in particular,

• The monetary policy actions and statements of the

Federal Reserve and the Federal Open Market

Committee (FOMC),

• The level of, and direction, timing and magnitude of

movement in, interest rates and the shape of the

interest rate yield curve,

• The functioning and other performance of, and

availability of liquidity in, the capital and other

financial markets,

• Loan demand, utilization of credit commitments and

standby letters of credit, and asset quality,

• Customer demand for non-loan products and services,

• Changes in the competitive and regulatory landscape

and in counterparty creditworthiness and

performance as the financial services industry

restructures in the current environment,

• The impact of the extensive reforms enacted in the

Dodd-Frank legislation and other legislative,

regulatory and administrative initiatives and actions,

including those outlined elsewhere in this Report and

in our other SEC filings, and

• The impact of market credit spreads on asset

valuations.

In addition, our success will depend upon, among other things:

• Focused execution of strategic priorities for organic

customer growth opportunities,

• Further success in growing profitability through the

acquisition and retention of customers and deepening

relationships,

• Driving growth in acquired and underpenetrated

geographic markets, including our Southeast markets,

• Our ability to effectively manage PNC’s balance

sheet and generate net interest income,

• Revenue growth from fee income and our ability to

provide innovative and valued products to our

customers,

• Our ability to utilize technology to develop and

deliver products and services to our customers and

protect PNC’s systems and customer information,

• Our ability to enhance our critical infrastructure and

streamline our core processes,

• Our ability to manage and implement strategic

business objectives within the changing regulatory

environment,

• A sustained focus on expense management,

• Improving our overall asset quality,

• Managing the non-strategic assets portfolio and

impaired assets,

The PNC Financial Services Group, Inc. – Form 10-K 31