PNC Bank 2013 Annual Report Download - page 245

Download and view the complete annual report

Please find page 245 of the 2013 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

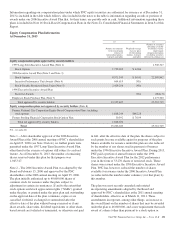

|

|

N

ONPERFORMING

A

SSETS AND

R

ELATED

I

NFORMATION

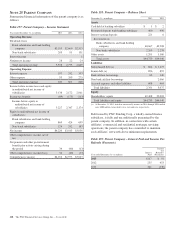

December 31 – dollars in millions 2013 2012 2011 2010 2009

Nonperforming loans

Commercial $ 457 $ 590 $ 899 $1,253 $1,806

Commercial real estate 518 807 1,345 1,835 2,140

Equipment lease financing 5 13 22 77 130

Total commercial lending 980 1,410 2,266 3,165 4,076

Consumer lending (a)

Home equity (b) (c) 1,139 951 529 448 356

Residential real estate (b) 904 845 726 818 1,203

Credit card (d) 4 5 8

Other consumer (b) 61 43 31 35 36

Total consumer lending (e) 2,108 1,844 1,294 1,301 1,595

Total nonperforming loans (f) 3,088 3,254 3,560 4,466 5,671

OREO and foreclosed assets

Other real estate owned (OREO) (g) 360 507 561 589 484

Foreclosed and other assets 9 33 35 68 49

Total OREO and foreclosed assets 369 540 596 657 533

Total nonperforming assets $3,457 $3,794 $4,156 $5,123 $6,204

Nonperforming loans to total loans 1.58% 1.75% 2.24% 2.97% 3.60%

Nonperforming assets to total loans, OREO and foreclosed assets 1.76 2.04 2.60 3.39 3.92

Nonperforming assets to total assets 1.08 1.24 1.53 1.94 2.30

Interest on nonperforming loans

Computed on original terms $ 163 $ 212 $ 278 $ 329 $ 302

Recognized prior to nonperforming status 30 30 47 53 90

Past due loans

Accruing loans past due 90 days or more (h) $1,491 $2,351 $2,973 $2,709 $2,698

As a percentage of total loans .76% 1.26% 1.87% 1.80% 1.71%

Past due loans held for sale

Accruing loans held for sale past due 90 days or more (i) $ 4 $ 38 $ 49 $ 65 $ 72

As a percentage of total loans held for sale .18% 1.03% 1.67% 1.86% 2.84%

(a) Excludes most consumer loans and lines of credit, not secured by residential real estate, which are charged off after 120 to 180 days past due and are not placed on nonperforming

status.

(b) Pursuant to alignment with interagency supervisory guidance on practices for loans and lines of credit related to consumer lending in the first quarter of 2013, nonperforming home

equity loans increased $214 million, nonperforming residential mortgage loans increased $187 million and nonperforming other consumer loans increased $25 million. Charge-offs

were taken on these loans where the fair value less costs to sell the collateral was less than the recorded investment of the loan and were $134 million.

(c) In the first quarter of 2012, we adopted a policy stating that Home equity loans past due 90 days or more would be placed on nonaccrual status. Prior policy required that these loans

be past due 180 days before being placed on nonaccrual status.

(d) Effective in the second quarter 2011, the commercial nonaccrual policy was applied to certain small business credit card balances. This change resulted in loans being placed on

nonaccrual status when they become 90 days or more past due. We continue to charge off these loans at 180 days past due.

(e) Pursuant to regulatory guidance, issued in the third quarter of 2012, nonperforming consumer loans, primarily home equity and residential mortgage, increased $288 million in 2012

related to changes in treatment of certain loans classified as TDRs, net of charge-offs, resulting from bankruptcy where no formal reaffirmation was provided by the borrower and

therefore a concession has been granted based upon discharge from personal liability. Charge-offs have been taken where the fair value less costs to sell the collateral was less than the

recorded investment of the loan and were $128.1 million.

(f) Includes TDRs of $1,511 million at December 31, 2013, $1,589 million at December 31, 2012, $1,141 million at December 31, 2011, $784 million at December 31, 2010 and $440

million at December 31, 2009, respectively. Nonperforming loans exclude certain government insured or guaranteed loans, loans held for sale, loans accounted for under the fair value

option and purchased impaired loans.

(g) OREO excludes $245 million, $380 million, $280 million, $178 million and $112 million at December 31, 2013, December 31, 2012, December 31, 2011, December 31, 2010 and

December 31, 2009, respectively, related to residential real estate that was acquired by us upon foreclosure of serviced loans because they are insured by the Federal Housing

Administration (FHA) or guaranteed by the Department of Veterans Affairs (VA).

(h) Amounts include certain government insured or guaranteed consumer loans totaling $995 million, $2,236 million, $2,474 million, $2,167 million and $1,814 million at December 31,

2013, December 31, 2012, December 31, 2011, December 31, 2010 and December 31, 2009, respectively. Past due loan amounts exclude purchased impaired loans as they are

considered current loans due to the accretion of interest income.

(i) Amounts include certain government insured or guaranteed consumer loans held for sale totaling $4 million, zero, $15 million, $22 million and $27 million at December 31,

2013, December 31, 2012, December 31, 2011, December 31, 2010 and December 31, 2009, respectively.

The PNC Financial Services Group, Inc. – Form 10-K 227