PNC Bank 2013 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2013 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

|

|

T

ROUBLED

D

EBT

R

ESTRUCTURINGS

A TDR is a loan whose terms have been restructured in a

manner that grants a concession to a borrower experiencing

financial difficulties. TDRs result from our loss mitigation

activities and include rate reductions, principal forgiveness,

postponement/reduction of scheduled amortization and

extensions, which are intended to minimize economic loss and

to avoid foreclosure or repossession of collateral.

Additionally, TDRs also result from borrowers that have been

discharged from personal liability through Chapter 7

bankruptcy and have not formally reaffirmed their loan

obligations to PNC. For the twelve months ended

December 31, 2013, $2.3 billion of loans held for sale, loans

accounted for under the fair value option and pooled

purchased impaired loans, as well as certain consumer

government insured or guaranteed loans, were excluded from

the TDR population. The comparable amount for the twelve

months ended December 31, 2012 was $3.1 billion.

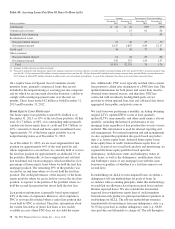

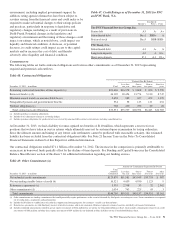

Table 44: Summary of Troubled Debt Restructurings

In millions

December 31

2013

December 31

2012

Consumer lending:

Real estate-related $1,939 $2,028

Credit card 166 233

Other consumer 56 57

Total consumer lending 2,161 2,318

Total commercial lending 578 541

Total TDRs $2,739 $2,859

Nonperforming $1,511 $1,589

Accruing (a) 1,062 1,037

Credit card 166 233

Total TDRs $2,739 $2,859

(a) Accruing loans have demonstrated a period of at least six months of performance

under the restructured terms and are excluded from nonperforming loans. Loans

where borrowers have been discharged from personal liability through Chapter 7

bankruptcy and have not formally reaffirmed their loan obligations to PNC are not

returned to accrual status.

Total TDRs decreased $120 million, or 4%, during 2013.

Nonperforming TDRs totaled $1.5 billion, which represents

approximately 49% of total nonperforming loans.

TDRs that are performing (accruing) are excluded from

nonperforming loans. Generally, these loans have been

returned to performing status as the borrowers are performing

under the restructured terms for at least six consecutive

months. These TDRs increased $25 million, or 2%, during

2013 to $1.1 billion as of December 31, 2013. This increase

reflects the further seasoning and performance of the TDRs.

Loans where borrowers have been discharged from personal

liability through Chapter 7 bankruptcy and have not formally

reaffirmed their loan obligations to PNC are not returned to

accrual status. See Note 5 Asset Quality in the Notes To

Consolidated Financial Statements in this Report for

additional information.

A

LLOWANCES FOR

L

OAN AND

L

EASE

L

OSSES AND

U

NFUNDED

L

OAN

C

OMMITMENTS AND

L

ETTERS OF

C

REDIT

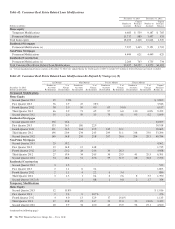

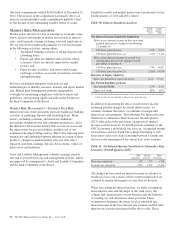

We recorded $1.1 billion in net charge-offs for 2013,

compared to $1.3 billion for 2012. Commercial lending net

charge-offs decreased from $359 million in 2012 to $249

million in 2013. Consumer lending net charge-offs decreased

from $930 million in 2012 to $828 million in 2013.

Table 45: Loan Charge-Offs And Recoveries

Year ended December 31

Dollars in millions

Gross

Charge-offs Recoveries

Net

Charge-offs /

(Recoveries)

Percent of

Average Loans

2013

Commercial $ 395 $248 $ 147 .17%

Commercial real

estate 203 93 110 .57

Equipment lease

financing 8 16 (8) (.11)

Home equity 486 73 413 1.14

Residential real estate 133 4 129 .86

Credit card 178 22 156 3.75

Other consumer 185 55 130 .60

Total $1,588 $511 $1,077 .57

2012

Commercial $ 474 $300 $ 174 .23%

Commercial real

estate 314 115 199 1.10

Equipment lease

financing 16 30 (14) (.21)

Home equity 560 61 499 1.41

Residential real estate 110 (1) 111 .72

Credit card 200 26 174 4.26

Other consumer 196 50 146 .72

Total $1,870 $581 $1,289 .73

For 2013, gross charge-offs were $1.6 billion and net charge-

offs to average loans was 0.57%, and included charge-offs of

$134 million taken pursuant to alignment with interagency

guidance on practices for loans and lines of credit related to

consumer lending in the first quarter of 2013.

In addition, total net charge-offs are lower than they would

have been otherwise due to the accounting treatment for

purchased impaired loans. This treatment also results in a

lower ratio of net charge-offs to average loans. See Note 6

Purchased Loans in the Notes To Consolidated Financial

Statements in Item 8 of this Report for additional information

on net charge-offs related to these loans.

We maintain an ALLL to absorb losses from the loan and

lease portfolio and determine this allowance based on

quarterly assessments of the estimated probable credit losses

incurred in the loan and lease portfolio. We maintain the

ALLL at a level that we believe to be appropriate to absorb

estimated probable credit losses incurred in the loan and lease

82 The PNC Financial Services Group, Inc. – Form 10-K