Chevron 2012 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2012 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

Chevron Corporation 2012 Annual Report 55

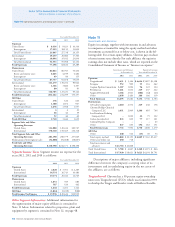

e following table indicates the changes to the company’s

suspended exploratory well costs for the three years ended

December 31, 2012:

2012 2011 2010

Beginning balance at January 1 $ 2,434 $ 2,718 $ 2,435

Additions to capitalized exploratory

well costs pending the

determination of proved reserves 595 652 482

Reclassications to wells, facilities

and equipment based on the

determination of proved reserves (244) (828) (129)

Capitalized exploratory well costs

charged to expense (49) (45) (70)

Other reductions* (55) (63) –

Ending balance at December 31 $ 2,681 $ 2,434 $ 2,718

*Represents property sales.

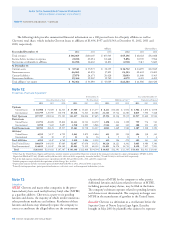

e following table provides an aging of capitalized well

costs and the number of projects for which exploratory well

costs have been capitalized for a period greater than one year

since the completion of drilling.

At December 31

2012 2011 2010

Exploratory well costs capitalized

for a period of one year or less $ 501 $ 557 $ 419

Exploratory well costs capitalized

for a period greater than one year 2,180 1,877 2,299

Balance at December 31 $ 2,681 $ 2,434 $ 2,718

Number of projects with exploratory

well costs that have been capitalized

for a period greater than one year* 46 47 53

* Certain projects have multiple wells or elds or both.

Of the $2,180 of exploratory well costs capitalized for

more than one year at December 31, 2012, $1,359 (23 proj-

ects) is related to projects that had drilling activities under

way or rmly planned for the near future. e $821 balance

is related to 23 projects in areas requiring a major capital

expenditure before production could begin and for which

additional drilling eorts were not under way or rmly

planned for the near future. Additional drilling was not

deemed necessary because the presence of hydrocarbons had

already been established, and other activities were in process

to enable a future decision on project development.

Note 17

New Accounting Standards

Balance Sheet (Topic 210) Disclosures about Osetting

Assets and Liabilities (ASU 2011-11) In December 2011,

the FASB issued ASU 2011-11, which became eective for

the company on January 1, 2013. e standard amends and

expands disclosure requirements about osetting and related

arrangements. e company does not anticipate any impacts

to its results of operations, nancial position or liquidity

when the guidance becomes eective.

Comprehensive Income (Topic 220) Reporting of

Amounts Reclassied Out of Accumulated Other Com-

prehensive Income (ASU 2013-02) e FASB issued ASU

2013-02 in February 2013. is standard became eective

for the company on January 1, 2013. ASU 2013-02 changes

the presentation requirements of signicant reclassications

out of accumulated other comprehensive income in their

entirety and their corresponding eect on net income. For

other signicant amounts that are not required to be reclas-

sied in their entirety, the standard requires the company to

cross-reference to related footnote disclosures. Adoption of

the standard is not expected to have a signicant impact on

the company’s nancial statement presentation.

Note 18

Accounting for Suspended Exploratory Wells

Accounting standards for the costs of exploratory wells (ASC

932) provide that exploratory well costs continue to be capi-

talized after the completion of drilling when (a) the well has

found a sucient quantity of reserves to justify completion

as a producing well, and (b) the entity is making sucient

progress assessing the reserves and the economic and operat-

ing viability of the project. If either condition is not met or

if an enterprise obtains information that raises substantial

doubt about the economic or operational viability of the proj-

ect, the exploratory well would be assumed to be impaired,

and its costs, net of any salvage value, would be charged to

expense. (Note that an entity is not required to complete the

exploratory well as a producing well.) e accounting stan-

dards provide a number of indicators that can assist an entity

in demonstrating that sucient progress is being made in

assessing the reserves and economic viability of the project.