Chevron 2012 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2012 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

Chevron Corporation 2012 Annual Report 19

Liquidity and Capital Resources

Cash, cash equivalents, time deposits and marketable

securities Total balances were $21.9 billion and $20.1 bil-

lion at December 31, 2012 and 2011, respectively. Cash

provided byoperating activities in 2012 was $38.8 billion,

compared with $41.1 billion in 2011 and $31.4 billion in

2010. Cash provided by operating activities was net of contri-

butions to employee pension plans of approximately

$1.2 billion, $1.5 billion and $1.4 billion in 2012, 2011 and

2010, respectively. Cash provided by investing activities

included proceeds and deposits related to asset sales of

$2.7 billion in 2012, $3.5 billion in 2011, and $2.0billion in

2010.

Restricted cash of $1.5 billion and $1.2 billion associated

with tax payments, upstream abandonment activities, funds

held in escrow for an asset acquisition and capital investment

projects at December 31, 2012 and 2011, respectively, was

invested in short-term marketable securities and recorded as

“Deferred charges and other assets” on the Consolidated Balance

Sheet.

Dividends Dividends paid to common stockholders

were $6.8 billion in 2012, $6.1 billion in 2011 and $5.7

billion in 2010. In April 2012, the company increased its

quarterly dividend by 11.1 percent to 90 cents per common

share.

Debt and capital lease obligations Total debt and capi-

tal lease obligations were $12.2 billion at December 31, 2012,

up from $10.2 billion at year-end 2011.

e $2.0 billion increase in total debt and capital lease

obligations during 2012 included the net eect of a $4 bil-

lion bond issuance and the early redemption of a $2 billion

bond due in March 2014. e company’s debt and capital

lease obligations due within one year, consisting primarily

of commercial paper, redeemable long-term obligations and

the current portion of long-term debt, totaled $6.0 billion at

December 31, 2012, compared with $5.9 billion at year-end

2011. Of these amounts, $5.9 billion and $5.6 billion were

reclassied to long-term at the end of each period, respec-

tively. At year-end 2012, settlement of these obligations was

not expected to require the use of working capital in 2013, as

the company had the intent and the ability, as evidenced by

committed credit facilities, to renance them on a long-term

basis.

At December 31, 2012, the company had $6.0 billion in

committed credit facilities with various major banks, expiring

in December 2016, which enable the renancing of short-

term obligations on a long-term basis. ese facilities support

commercial paper borrowing and can also be used for gen-

eral corporate purposes. e company’s practice has been to

continually replace expiring commitments with new com-

mitments on substantially the same terms, maintaining levels

management believes appropriate. Any borrowings under the

facilities would be unsecured indebtedness at interest rates

based on the London Interbank Oered Rate or an average of

base lending rates published by specied banks and on terms

reecting the company’s strong credit rating. No borrowings

were outstanding under these facilities at December 31, 2012.

In addition, in November 2012, the company led with the

Securities and Exchange Commission a new registration

statement that expires in November 2015. is registration

statement is for an unspecied amount of nonconvertible

debt securities issued or guaranteed by the company.

e major debt rating agencies routinely evaluate the

company’s debt, and the company’s cost of borrowing can

increase or decrease depending on these debt ratings. e

company has outstanding public bonds issued by Chevron

Corporation, Chevron Corporation Prot Sharing/Sav-

ings Plan Trust Fund and Texaco Capital Inc. All of these

securities are the obligations of, or guaranteed by, Chevron

Corporation and are rated AA by Standard & Poor’s Corpo-

ration and Aa1 by Moody’s Investors Service. e company’s

U.S. commercial paper is rated A-1+ by Standard & Poor’s

and P-l by Moody’s. All of these ratings denote high-quality,

investment-grade securities.

e company’s future debt level is dependent primar-

ily on results of operations, the capital program and cash

that may be generated from asset dispositions. Based on its

high-quality debt ratings, the company believes that it has

substantial borrowing capacity to meet unanticipated cash

requirements. e company also can modify capital spending

plans during any extended periods of low prices for crude oil

and natural gas and narrow margins for rened products and

commodity chemicals to provide exibility to continue pay-

ing the common stock dividend and maintain the company’s

high-quality debt ratings.

Common stock repurchase program In July 2010, the

Board of Directors approved an ongoing share repurchase

program with no set term or monetary limits. e company

expects to repurchase between $500 million and $2 billion

of its common shares per quarter, at prevailing prices, as

permitted by securities laws and other legal requirements

and subject to market conditions and other factors. During

2012, the company purchased 46.6 million common shares

for $5.0 billion. From the inception of the program through

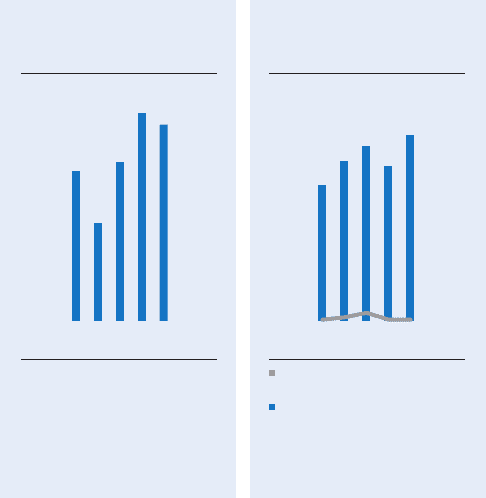

0.0

45.0

18.0

27.0

9.0

36.0

Cash Provided by

Operating Activities

Billions of dollars

Operating cash flows were $2.2

billion lower than 2011, primarily

due to lower benefits from working

capital and lower equity affiliate

distributions.

0908 10 11 12

$38.8

0.0

15.0

12.0

3.0

6.0

9.0

0.0

1.5

1.2

0.9

0.6

0.3

Total Interest Expense &

Total Debt at Year-End

Billions of dollars

Total Interest Expense

(right scale)

Total Debt (left scale)

Total debt increased $2.0 billion

during 2012 to $12.2 billion. All

interest expense was capitalized

as part of the cost of major

projects in 2012 and 2011.

$12.2

0908 10 11 12