Chevron 2012 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2012 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

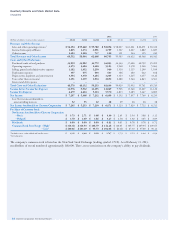

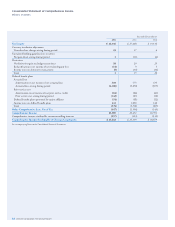

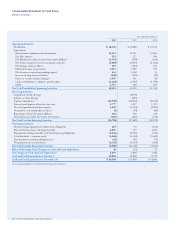

Chevron Corporation 2012 Annual Report 27

In making the determination as to whether a decline

is other than temporary, the company considers such fac-

tors as the duration and extent of the decline, the investee’s

nancial performance, and the company’s ability and

intention to retain its investment for a period that will

be sucient to allow for any anticipated recovery in the

investment’s market value. Diering assumptions could

aect whether an investment is impaired in any period or

the amount of the impairment, and are not subject to sen-

sitivity analysis.

From time to time, the company performs impair-

ment reviews and determines whether any write-down in

the carrying value of an asset or asset group is required.

For example, when signicant downward revisions to

crude oil and natural gas reserves are made for any single

eld or concession, an impairment review is performed

to determine if the carrying value of the asset remains

recoverable. Also, if the expectation of sale of a particular

asset or asset group in any period has been deemed more

likely than not, an impairment review is performed, and

if the estimated net proceeds exceed the carrying value of

the asset or asset group, no impairment charge is required.

Such calculations are reviewed each period until the asset

or asset group is disposed of. Assets that are not impaired

on a held-and-used basis could possibly become impaired

if a decision is made to sell such assets. at is, the assets

would be impaired if they are classied as held-for-sale and

the estimated proceeds from the sale, less costs to sell, are

less than the assets’ associated carrying values.

Asset Retirement Obligations In the determination

of fair value for an asset retirement obligation (ARO),

the company uses various assumptions and judgments,

including such factors as the existence of a legal obligation,

estimated amounts and timing of settlements, discount

and ination rates, and the expected impact of advances

in technology and process improvements. A sensitivity

analysis of the ARO impact on earnings for 2012 is not

practicable, given the broad range of the company’s long-

lived assets and the number of assumptions involved in the

estimates. at is, favorable changes to some assumptions

would have reduced estimated future obligations, thereby

lowering accretion expense and amortization costs, whereas

unfavorable changes would have the opposite eect. Refer

to Note 23 on page 66 for additional discussions on asset

retirement obligations.

Contingent Losses Management also makes judg-

ments and estimates in recording liabilities for claims,

litigation, tax matters and environmental remediation.

Actual costs can frequently vary from estimates for a

variety of reasons. For example, the costs for settlement

of claims and litigation can vary from estimates based on

diering interpretations of laws, opinions on culpability

and assessments on the amount of damages. Similarly,

liabilities for environmental remediation are subject to

change because of changes in laws, regulations and their

interpretation, the determination of additional informa-

tion on the extent and nature of site contamination, and

improvements in technology.

Under the accounting rules, a liability is generally

recorded for these types of contingencies if management

determines the loss to be both probable and estimable.

ecompany generally reports these losses as “Operating

expenses” or “Selling, general and administrative

expenses” on the Consolidated Statement of Income. An

exception to this handling is for income tax matters, for

which benets are recognized only if management deter-

mines the tax position is“more likely than not” (i.e.,

likelihood greater than 50percent) to be allowed by the

tax jurisdiction. For additional discussion of income tax

uncertainties, refer to Note 14 beginning on page 51.

Refer also to the business segment discussions elsewhere

in this section for the eect on earnings from losses asso-

ciated with certain litigation, environmen tal remediation

and tax matters for the three years ended December 31,

2012.

An estimate as to the sensitivity to earnings for these

periods if other assumptions had been used in recording

these liabilities is not practicable because of the number

of contingencies that must be assessed, the number of

underlying assumptions and the wide range of reasonably

possible outcomes, both in terms of the probability of loss

and the estimates of such loss.

New Accounting Standards

Refer to Note 17, on page 55 in the Notes to Consolidated

Financial Statements, for information regarding new

accounting standards.