UPS 2007 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2007 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

|

|

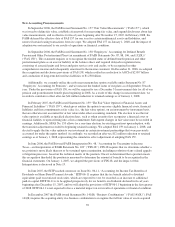

experience or changes in assumptions may affect our pension and other postretirement obligations and future

expense. A 25 basis point change in the assumed discount rate, expected return on assets, and health care cost

trend rate for the U.S. pension and postretirement benefit plans would result in the following increases

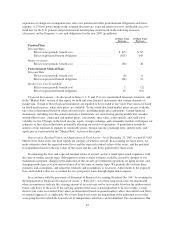

(decreases) on the Company’s costs and obligations for the year 2007 (in millions):

25 Basis Point

Increase

25 Basis Point

Decrease

Pension Plans

Discount Rate:

Effect on net periodic benefit cost .......................... $ (65) $ 67

Effect on projected benefit obligation ....................... (615) 643

Return on Assets:

Effect on net periodic benefit cost .......................... (36) 36

Postretirement Medical Plans

Discount Rate:

Effect on net periodic benefit cost .......................... (6) 6

Effect on projected benefit obligation ....................... (88) 91

Health Care Cost Trend Rate:

Effect on net periodic benefit cost .......................... 2 (2)

Effect on projected benefit obligation ....................... 19 (19)

Financial Instruments—As discussed in Notes 2, 3, 8, and 15 to our consolidated financial statements, and

in the “Market Risk” section of this report, we hold and issue financial instruments that contain elements of

market risk. Certain of these financial instruments are required to be recorded at fair value. Fair values are based

on listed market prices, when such prices are available. To the extent that listed market prices are not available,

fair value is determined based on other relevant factors, including dealer price quotations. Certain financial

instruments, including over-the-counter derivative instruments, are valued using pricing models that consider,

among other factors, contractual and market prices, correlations, time value, credit spreads, and yield curve

volatility factors. Changes in the fixed income, equity, foreign exchange, and commodity markets will impact our

estimates of fair value in the future, potentially affecting our results of operations. A quantitative sensitivity

analysis of our exposure to changes in commodity prices, foreign currency exchange rates, interest rates, and

equity prices is presented in the “Market Risk” section of this report.

Depreciation, Residual Value, and Impairment of Fixed Assets—As of December 31, 2007, we had $17.663

billion of net fixed assets, the most significant category of which is aircraft. In accounting for fixed assets, we

make estimates about the expected useful lives and the expected residual values of the assets, and the potential

for impairment based on the fair values of the assets and the cash flows generated by these assets.

In estimating the lives and expected residual values of aircraft, we have relied upon actual experience with

the same or similar aircraft types. Subsequent revisions to these estimates could be caused by changes to our

maintenance program, changes in the utilization of the aircraft, governmental regulations on aging aircraft, and

changing market prices of new and used aircraft of the same or similar types. We periodically evaluate these

estimates and assumptions, and adjust the estimates and assumptions as necessary. Adjustments to the expected

lives and residual values are accounted for on a prospective basis through depreciation expense.

In accordance with the provisions of Statement of Financial Accounting Standards No. 144 “Accounting for

the Impairment or Disposal of Long-Lived Assets” (“FAS 144”), we review long-lived assets for impairment

when circumstances indicate the carrying amount of an asset may not be recoverable based on the undiscounted

future cash flows of the asset. If the carrying amount of the asset is determined not to be recoverable, a write-

down to fair value is recorded. Fair values are determined based on quoted market values, discounted cash flows,

or external appraisals, as applicable. We review long-lived assets for impairment at the individual asset or the

asset group level for which the lowest level of independent cash flows can be identified. The circumstances that

42