UPS 2006 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2006 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

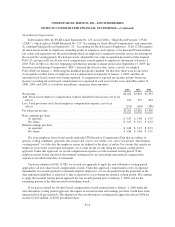

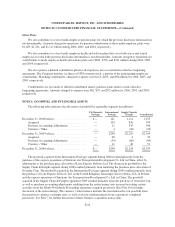

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

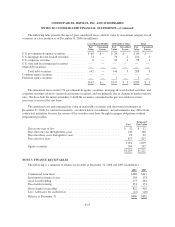

The table below provides the weighted-average actuarial assumptions used to determine the benefit

obligations of our plans.

Pension Benefits

Postretirement

Medical Benefits

International

Pension Benefits

2006 2005 2006 2005 2006 2005

Discount rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.00% 5.75% 6.00% 5.75% 4.96% 4.93%

Rate of compensation increase ................ 4.50% 4.00% N/A N/A 3.79% 3.94%

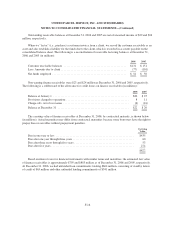

Our pension and other postretirement benefit costs are calculated using various actuarial assumptions and

methodologies as prescribed by Statement of Financial Accounting Standards No. 87, “Employers’ Accounting

for Pensions” and Statement of Financial Accounting Standards No. 106, “Employers’ Accounting for

Postretirement Benefits Other than Pensions.” These assumptions include discount rates, expected return on plan

assets, health care cost trend rates, inflation, rate of compensation increases, mortality rates, and other factors.

Actuarial assumptions are reviewed on an annual basis.

A discount rate is used to determine the present value of our future benefit obligations. For U.S. plans, the

discount rate is determined by matching the expected cash flows to a yield curve based on long-term, high

quality fixed income debt instruments available as of the measurement date. For international plans, the discount

rate is selected based on high quality fixed income indices available in the country in which the plan is

domiciled. These assumptions are updated each year.

An assumption for return on plan assets is used to determine the expected return on asset component of net

periodic benefit cost for the fiscal year. This assumption for our U.S. plans was evaluated using input from third-

party consultants and various pension plan asset managers, including their long-term projection of returns for

each asset class and our target allocation. For our U.S. plans, the 10-year U.S. Treasury yield is the foundation

for all other asset class returns, and various risk premiums are added to determine the expected return for each

allocation.

For plans outside the U.S., consideration is given to local market expectations of long-term returns.

Strategic asset allocations are determined by country, based on the nature of liabilities and considering the

demographic composition of the plan participants.

Health care cost trends are used to project future postretirement benefits payable from our plans. For

year-end 2006 obligations, future postretirement medical benefit costs were forecasted assuming an initial annual

increase of 9.0%, decreasing to 5.0% by the year 2011 and with consistent annual increases at those ultimate

levels thereafter.

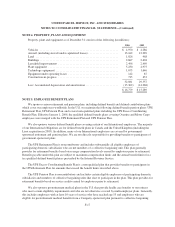

Assumed health care cost trends have a significant effect on the amounts reported for the U.S.

postretirement medical plans. A one-percent change in assumed health care cost trend rates would have the

following effects (in millions):

1% Increase 1% Decrease

Effect on total of service cost and interest cost ...................... $ 7 $ (4)

Effect on postretirement benefit obligation ......................... 70 (65)

F-19