UPS 2006 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2006 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

|

|

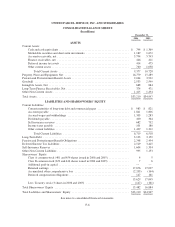

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Stock-Based Compensation

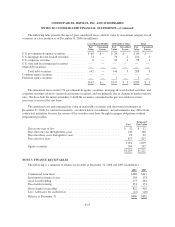

In December 2004, the FASB issued Statement No. 123 (revised 2004), “Share-Based Payment” (“FAS

123(R)”), which replaces FASB Statement No. 123 “Accounting for Stock-Based Compensation” and supercedes

Accounting Principles Board Opinion No. 25, “Accounting for Stock Issued to Employees”. FAS 123(R) requires

all share-based awards to employees, including grants of employee stock options, to be measured based on their

fair values and expensed over the period during which an employee is required to provide service in exchange for

the award (the vesting period). We had previously adopted the fair value recognition provisions of the original

FAS 123, prospectively for all new stock compensation awards granted to employees subsequent to January 1,

2003. FAS 123(R) was effective beginning with the first interim or annual period after September 15, 2005; the

Securities and Exchange Commission (“SEC”) deferred the effective date, and as a result, we adopted

FAS 123(R) on January 1, 2006 using the modified prospective method. On that date, there were no unvested

stock options or other forms of employee stock compensation issued prior to January 1, 2003, and thus all

unvested stock-based awards were being expensed. A comparison of reported net income and pro-forma net

income (assuming all stock-based compensation was expensed in each year) for the years ended December 31,

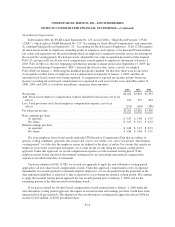

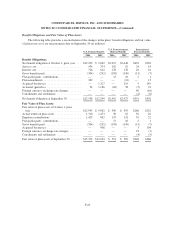

2006, 2005, and 2004, is as follows (in millions, except per share amounts):

2006 2005 2004

Net income ........................................................... $4,202 $3,870 $3,333

Add: Stock-based employee compensation expense included in net income, net of tax

effects ............................................................. 231 157 563

Less: Total pro forma stock-based employee compensation expense, net of tax

effects ............................................................. (231) (165) (588)

Pro forma net income ................................................... $4,202 $3,862 $3,308

Basic earnings per share

As reported ....................................................... $ 3.87 $ 3.48 $ 2.95

Pro forma ........................................................ $ 3.87 $ 3.47 $ 2.93

Diluted earnings per share

As reported ....................................................... $ 3.86 $ 3.47 $ 2.93

Pro forma ........................................................ $ 3.86 $ 3.46 $ 2.91

We issue employee share-based awards under the UPS Incentive Compensation Plan that are subject to

specific vesting conditions; generally, the awards cliff vest or vest ratably over a five year period, “the nominal

vesting period,” or at the date the employee retires (as defined by the plan), if earlier. For awards that specify an

employee vests in the award upon retirement, we account for the awards using the nominal vesting period

approach. Under this approach, we record compensation expense over the nominal vesting period. If the

employee retires before the end of the nominal vesting period, any remaining unrecognized compensation

expense is recorded at the date of retirement.

Upon our adoption of FAS 123(R), we revised our approach to apply the non-substantive vesting period

approach to all new share-based compensation awards. Under this approach, compensation cost is recognized

immediately for awards granted to retirement-eligible employees, or over the period from the grant date to the

date retirement eligibility is achieved, if that is expected to occur during the nominal vesting period. We continue

to apply the nominal vesting period approach for any awards granted prior to January 1, 2006, and for the

remaining portion of the then unvested outstanding awards.

If we had accounted for all share-based compensation awards granted prior to January 1, 2006 under the

non-substantive vesting period approach, the impact to our net income and earnings per share would have been

immaterial for all prior periods. The adoption of the non-substantive vesting period approach reduced 2006 net

income by $23 million, or $0.02 per diluted share.

F-12